Asian Futures:

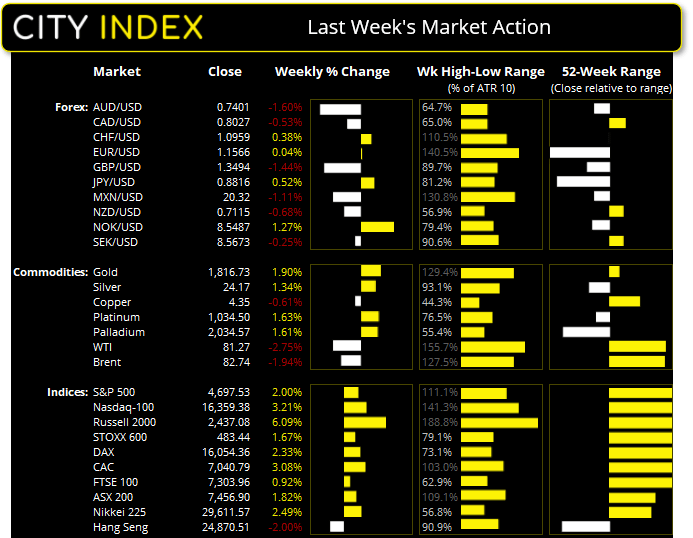

- Australia’s ASX 200 index closed at 7,456.90 on Friday

- Japan's Nikkei 225 index closed at 29,611.57 on Friday

- Hong Kong's Hang Seng index closed at 24,870.51 on Friday

- China'sA50 Index closed at 15,591.46 on Friday

European Friday close:

- UK's FTSE 100 index rose 24.05 points (0.33%) to close at 7303.96

- Europe'sEuro STOXX 50 index rose 29.7 points (0.69%) to close at 4363.04

- Germany's DAX index rose 24.71 points (0.15%) to close at 16054.36

- France's CAC 40 index rose 53 points (0.76%) to close at 7040.79

US Friday close:

- The Dow Jones rose 203.75 points (0.56%) to close at 36,327.95

- The S&P 500 rose 17.47 points (0.38%) to close at 4,697.53

- The Nasdaq 100 rose 13.133 points (0.08%) to close at 16,359.38

Indices:

The S&P 500 rose for a fifth consecutive week, although Friday’s Spinning Top Doji at the monthly R1 pivot suggests it may need to pause for breath. The Russell 2000 hasn’t really looked back since it broke its 8-month sideways range. We remain bullish above 2357 and would welcome any pullback towards it.

We’ll have our eyes on the Nikkei today to see if it can extend its post-election rally. Reports over the weekend suggest that PM Kishida may move ahead with his election promise with a ¥35 trillion economic package. The package is to include around ¥100k cash handouts for children 18 and below, regardless of household income. The travel ban will also be eased to allow internal travel. Kishida has vowed to unveil several large-scale packages this month and aims to get them past parliament by the end of the year. We’ll dig through the details when they arrive but, on the face of it, it suggests BOJ may have reason to up their forecasts for growth and CPI for a change.

The ASX 200 formed a bullish outside week although resistance was met at the monthly R1 pivot on Friday. If prices can hold above Friday’s low today then perhaps it can break out and have another crack at trading above 7500.

ASX 200 Market Internals:

ASX 200: 7456.9 (0.39%), 06 November 2021

- Telecomm Services (1.65%) was the strongest sector and Information Technology (-1.64%) was the weakest

- 8 out of the 11 sectors closed higher

- 2 out of the 11 sectors closed lower

- 7 out of the 11 sectors outperformed the index

- 117 (58.50%) stocks advanced, 73 (36.50%) stocks declined

- 66% of stocks closed above their 200-day average

- 60% of stocks closed above their 50-day average

- 64% of stocks closed above their 20-day average

Outperformers:

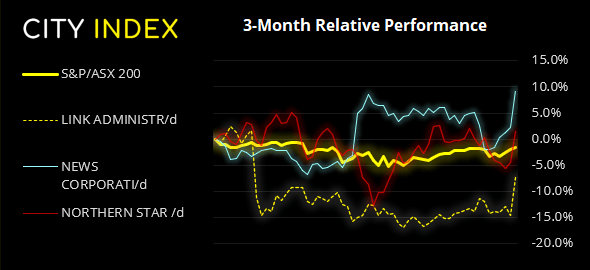

- + 8.55%-Link Administration Holdings Ltd(LNK.AX)

- + 6.94%-News Corp(NWS.AX)

- + 6.31%-Northern Star Resources Ltd(NST.AX)

Underperformers:

- ·-12.48%-Clinuvel Pharmaceuticals Ltd(CUV.AX)

- ·-11.27%-Virgin Money UK PLC(VUK.AX)

- ·-5.53%-Afterpay Ltd(APT.AX)

Forex:

Safe-haven currencies JPY and CHF were the strongest among the majors last week, with the yen rising around 0.5% and the Swiss franc up around 0.35% against the greenback.

AUD was the worst performer last week, falling -1.6% against the dollar. However, it found support at its 200-week eMA and formed a bullish hammer on the four-hour chart, so perhaps there’s chance for some follow-through on Monday although take note of the 200-day eMA at 7440.

The Canadian dollar was broadly lower on Friday after a disappointing employment and PMI report. Only 31.2k jobs were filled, compared with the 42k expected and 157.1k previously, although unemployment fell to 6.7% to beat the 6.8% forecast, and down from 6.9%. The Ivey PMI rose 59.3, which is quite below the 71.2 forecast and 70.4 previously.

The US dollar index printed a bearish hammer on the daily chart following Friday’s NFP report (which beat expectations). As it occurred just below the monthly R1 pivot and marks a false break above the October high, we suspect a countertrend move is underway for the dollar.

Commodities:

Oil prices rallied on Friday which saw WTI break back above $80. However, it’s interest to note that the initial break below $80 seems to have found support around 79.15 – a level we’d flagged ahead of the OPEC+ meeting as it had previously seen some strong buying activity around that level.

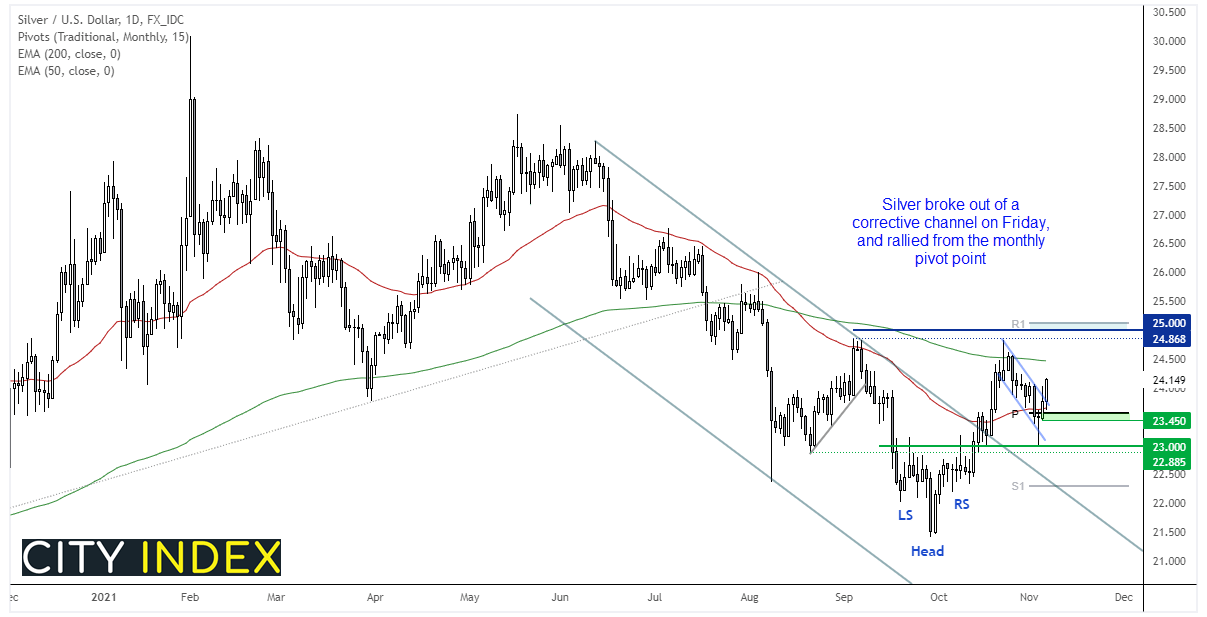

Silver prices appear to have troughed at $23 with a bullish pinbar. Its rally from the head and shoulders bottom initially found resistance around the 200-day eMA and just below $25 before pulling back. And we now suspect that pullback is now complete. Friday’s rally saw it bounce from the monthly pivot point. From here we suspect prices may try to have another crack at $25, and our bias remains bullish above Thursday’s low, which is just beneath the monthly pivot.

Up Next (Times in AEDT)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Trade Ideas articles

Yesterday 03:00 PM

Yesterday 11:14 AM

April 24, 2024 11:00 AM