Asian Futures:

- Australia's ASX 200 futures are down -28 points (-0.4%), the cash market is currently estimated to open at 7,016.90

- Japan's Nikkei 225 futures are down -450 points (-1.6%), the cash market is currently estimated to open at 27,697.51

- Hong Kong's Hang Seng futures are down -267 points (-0.95%), the cash market is currently estimated to open at 27,964.04

UK and Europe:

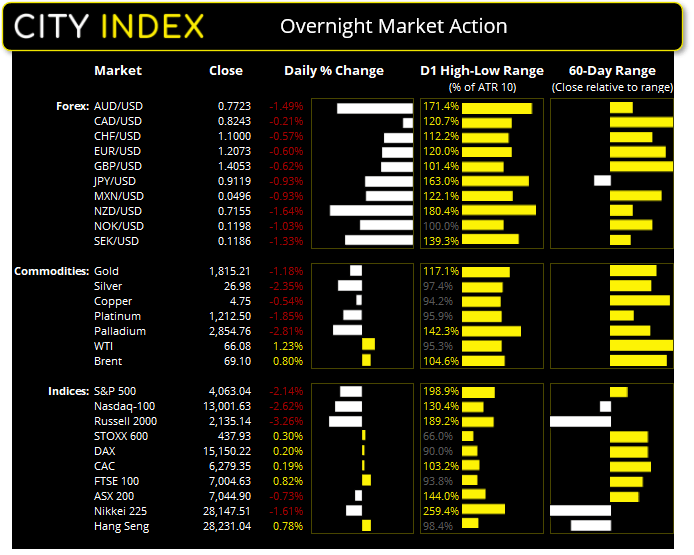

- UK's FTSE 100 index rose 56.64 points (0.82%) to close at 7,004.63

- Europe's Euro STOXX 50 index rose 1.37 points (0.03%) to close at 3,947.43

- Germany's DAX index rose 30.47 points (0.2%) to close at 15,150.22

- France's CAC 40 index rose 11.96 points (0.19%) to close at 6,279.35

Wednesday US Close:

- The Dow Jones Industrial fell -681.5 points (-1.99%) to close at 33,587.66

- The S&P 500 index fell -89.06 points (-2.15%) to close at 4,063.04

- The Nasdaq 100 index fell -349.633 points (-2.62%) to close at 13,001.63

Watch out, inflation’s about

On a year over year basis, inflation overshot forecasts by quite some margin. Broad CPI rose 4.2% YoY versus 3.2% expected and core CPI increased by 3.2% compared with 2% forecast. Yet as Joe Perry points out, with April’s core CPI rising 0.9% MoM is suggests upwards pressure will indeed spill over to May’s inflation report released next month. And if monthly inflation continues to rally it puts the Fed under pressure to concede that inflation may not be as transitory as made out, and be strong armed into raising rates or talking taper much sooner than currently they’re currently conveying.

Wall Street was broadly lower, seeing the Nasdaq 100 shed a further -2.6% to a six-week low and momentarily dip beneath 13k before settling at 13,00.64. The S&P 500 had its most bearish session since February with 10 of its 11 sectors in the red, led by consumer discretionary stocks.

As things stand, the ASX 200 is on track for a bearish pinbar on the monthly and weekly chart. There’s time for that to change of course, but something to consider as we approach the end of the week and month. The index has found support at its 50-bar eMA on the four-hour chart and around its 7,000 handle so there’ potential for a minor bounce, although further downside could be o the cards should prices remains beneath the 7100 handle.

ASX 200 Market Internals:

ASX 200: 7044.9 (-0.73%), 12 May 2021

- Information Technology (0.76%) was the strongest sector and Utilities (-2.19%) was the weakest

- 5 out of the 11 sectors outperformed the index

- 8 out of the 11 sectors closed lower

- 5 hit a new 52-week high, 6 hit a new 52-week low

- 72.7% of trades on the ASX 200 yesterday were on declining volume

- 60.5% of stocks closed above their 200-day average

- 53% of stocks closed above their 50-day average

- 36% of stocks closed above their 20-day average

Outperformers:

- + 6.42% - Resolute Mining Ltd (RSG.AX)

- + 4.45% - Nearmap Ltd (NEA.AX)

- + 4.23% - CSR Ltd (CSR.AX)

Underperformers:

- -7.71% - AusNet Services Ltd (AST.AX)

- -6.26% - Pointsbet Holdings Ltd (PBH.AX)

- -5.53% - Pilbara Minerals Ltd (PLS.AX)

Learn how to trade indices

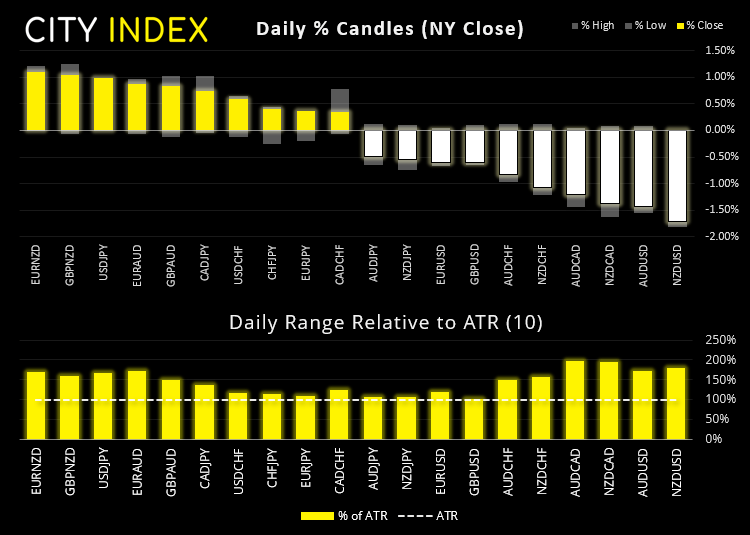

Forex: Most bullish session in eight for the dollar

The higher-than-expected CPI print lifted the US dollar to the top spot, rising against all of its major peers, with antipodeans (AUD, NZD) and the yen taking the biggest hit. The Canadian dollar was the second strongest major on the back of rising oil prices (and the general advantage of a hawkish central bank behind it)

- The US dollar index (DXY) enjoyed its most bullish session in eight and could remain supported if Fed members fail to dispel inflationary fears in public forums (Fed members Waller, Bullard and Kaplan all speak tomorrow).

- USD/CAD printed a bullish outside candle at key support (September 2017).

- USD/CHF is on the cusp of invalidating our bearish bias with a test of the 0.9094 high but, in the current environment, we feel inclined to remove it from the bearish watchlist anyway given the solid rise and lack of topping signal.

- AUD/CAD broken convincingly below 0.9450 support outlined in yesterday’s Asian open report and is about 2/3rd the way to 0the 0.9300/25 support zone.

- AUD/USD suffered its worst session in 10-week and closed beneath its 20-day eMA to a five-day low.

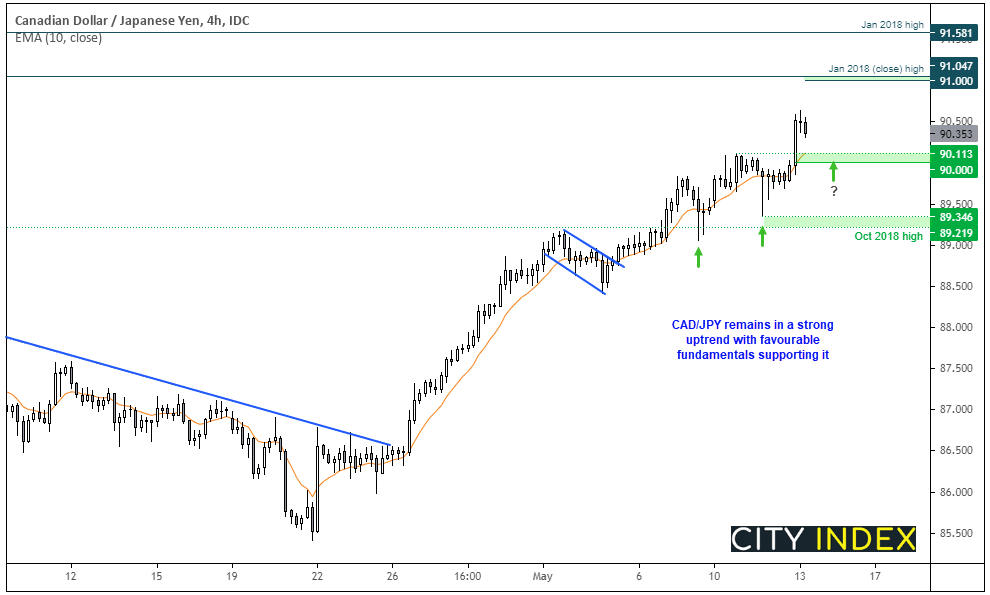

CAD/JPY’s bullish trend has remained firmed since breaking above its retracement line back in April. A series of prominent higher lows preceded breaks to new highs and yesterday’s close saw it at its highest level since January 2018. Prices are showing minor signs of exhaustion with the potential to consolidate or perform a gentle retracement, and we would welcome any dips towards the 90.00/11 support zone for fresh bullish opportunities. The next major target for bulls is just below the 91.00 handle / Jan 2018 closing high.

Learn how to trade forex

Commodities: Yields weigh on gold

Higher treasury yields weighed on gold, which is on track to close lower for the first week in five. Whilst near-term momentum points lower, bears can target 1800 support and bulls could reconsider their appetite for the yellow metal, should a base of support form around this key level. Silver prices are on track for a bearish outside week and are in a corrective phase within its bullish channel on the four-hour chart. Next support levels are 27.00, 26.63 and the lower trendline of the channel.

US oil exports fell and inventories declined, whilst the monthly IEA (International Energy Agency) report noted that demand is outstripping supply. Oil prices rose despite the stronger US dollar. The front month brent futures contract stopped just shy of retesting $70 and closed at 69.10, although prices could well break above it should prices continue to hold above its April bullish trendline on the daily chart.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM