Asian Futures:

- Australia's ASX 200 futures are up 6 points (0.09%), the cash market is currently estimated to open at 7,051.60

- Japan's Nikkei 225 futures are up 20 points (0.07%), the cash market is currently estimated to open at 29,146.23

- Hong Kong's Hang Seng futures are down -45 points (-0.16%), the cash market is currently estimated to open at 28,907.83

UK and Europe:

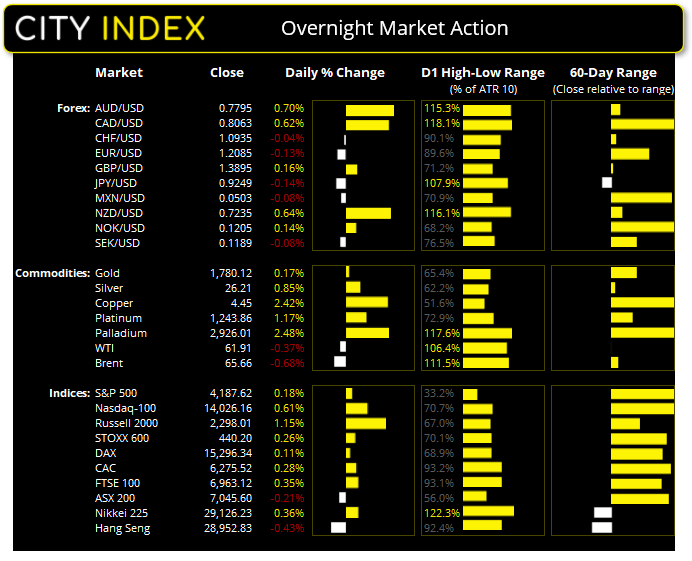

- UK's FTSE 100 index rose 24.56 points (0.35%) to close at 6,963.12

- Europe's Euro STOXX 50 index rose 7.49 points (0.19%) to close at 4,020.83

- Germany's DAX index rose 16.72 points (0.11%) to close at 15,296.34

- France's CAC 40 index rose 17.58 points (0.28%) to close at 6,275.52

Monday US Close:

- The Dow Jones Industrial fell -61.93 points (-0.18%) to close at 33,981.57

- The S&P 500 index rose 7.45 points (0.18%) to close at 4,187.62

- The Nasdaq 100 index rose 84.718 points (0.61%) to close at 14,026.16

Indices approach new highs ahead of a busy earnings week:

The US has pledged to share up to 60 million doses of the AstraZeneca vaccine with other countries, even though it has not been authorised for use in the US. The Nasdaq and S&P 500 approached their record highs ahead of a busy earnings week for US stocks. Around 40% of the stocks on the S&P 500 are due to release earnings reports between today and Thursday, so volatility can be expected on the index but its direction may be a flip of a coin. Seven out of the eleven sectors rise, with the energy sector taking the top spot whilst utilities and consumer staples were the weakest sectors.

ASX 200 Market Internals:

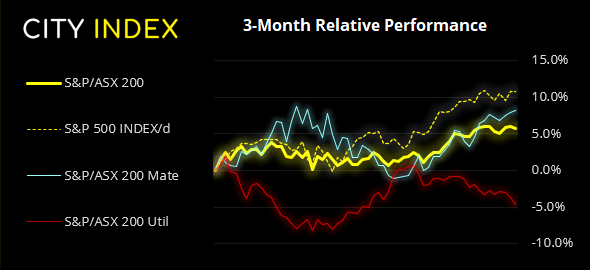

The ASX 200 fell -0.2% yesterday during a session of light trade. Although it printed a (small) bearish outside day, we remain confident that it remains in an uptrend which has been reinforced by the large bullish hammer last Wednesday. The trend remains bullish above 6900 although, if it is truly in an uptrend, should not have to retrace that far to bring into question the trends strength. Our bias remains bullish above 7,000, but the 6956 high can also be used to aid with risk management.

ASX 200: 7045.6 (-0.21%), 23 April 2021

- Materials (0.36%) was the strongest sector and Utilities (-0.99%) was the weakest

- 3 out of the 11 sectors outperformed the index

- 10 out of the 11 sectors closed lower

- 9 stocks hit a new 52-week high, 1 hit a new 52-week low

- 71% of stocks closed above their 200-day average

- 69.5% of stocks closed above their 50-day average

- 61.5% of stocks closed above their 20-day average

Outperformers

- + 10.2% - NIB Holdings Ltd (NHF.AX)

- + 4.80% - Fortescue Metals Group Ltd (FMG.AX)

- + 4.36% - Perpetual Ltd (PPT.AX)

Underperformers:

- -6.82% - Whitehaven Coal Ltd (WHC.AX)

- -4.64% - Blackmores Ltd (BKL.AX)

- -4.12% - Kogan.com Ltd (KGN.AX)

Learn how to trade indices

Forex: The Dollar is under pressure ahead of the Fed’s meeting

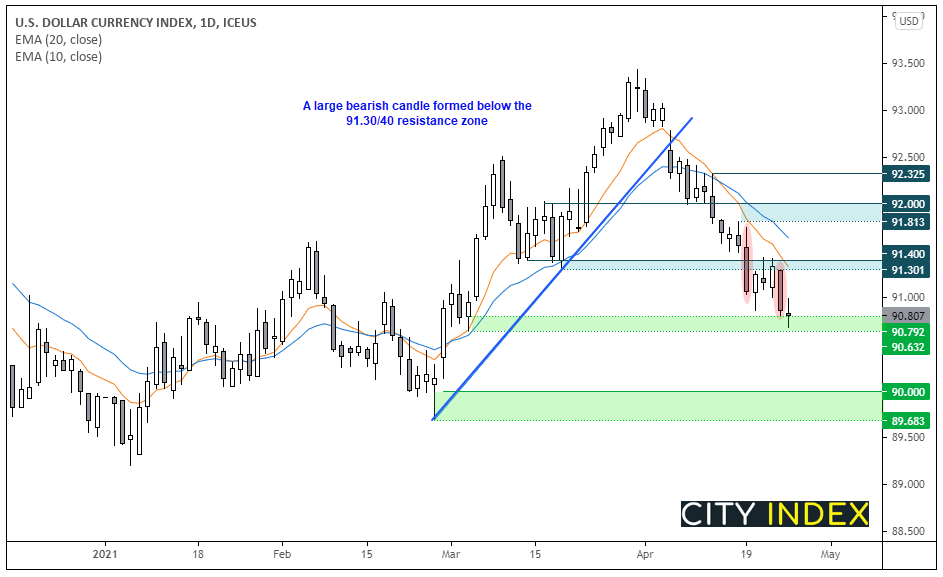

The US dollar index (DXY) printed a bearish engulfing candle on Friday, perfectly respecting the 91.30 resistance level. Our bias remains bearish below 91.40 and the target is the base of the (broken) trendline at 89.90. However, yesterday produced an indecision candle (Rikshaw Man Doji) above 90.63 support, so perhaps we’re approaching a period of consolidation.

AUD/USD printed a bullish engulfing candle yesterday, strongly suggesting 0.7690 to be a structural swing low. A break above 0.7850 assumes trend continuation.

CAD/JPY has broken out of consolidation. Now trading above its 20-day eMA, we suspect the correction from the March high is now complete. The swing low sits at 85.98 so the bias remains bullish above this level.

USD/CAD fell to a six-week low ahead of this week’s Fed meeting. There were several failed attempts to break above 1.2647 resistance, and last week printed a weekly bearish hammer and bearish outside day and a bearish outside/engulfing day on Wednesday. Given the established downtrend on the daily charts, our bias is for a break beneath the 1.2365 low.

Learn how to trade forex

Commodities:

Oil prices are refusing to break higher, yet both WTI and brent futures have reaffirmed their support levels. Rising coronavirus cases in India are weighing on prices, but not by enough to send prices lower. Perhaps the US supplying vaccine doses could help prices break higher in due course.

Gold produced a small bullish hammer yesterday and prices remains above the untested 1760/65 support zone. Our bias remains bullish above this level and the next target remains at 1835, projected from the double bottom pattern from 1676.

Silver remains in a corrective phase in a bullish channel and printed a small bullish engulfing candle yesterday. Our bias remains bullish above the 25.50/62 support zone.

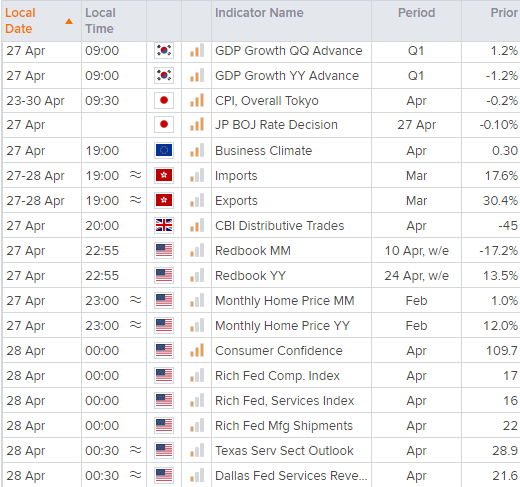

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM