Asian Futures:

- Australia's ASX 200 futures are up 37 points (0.53%), the cash market is currently estimated to open at 7,034.50

- Japan's Nikkei 225 futures are up 330 points (1.16%), the cash market is currently estimated to open at 28,838.55

- Hong Kong's Hang Seng futures are up 163 points (0.57%), the cash market is currently estimated to open at 28,784.92

UK and Europe:

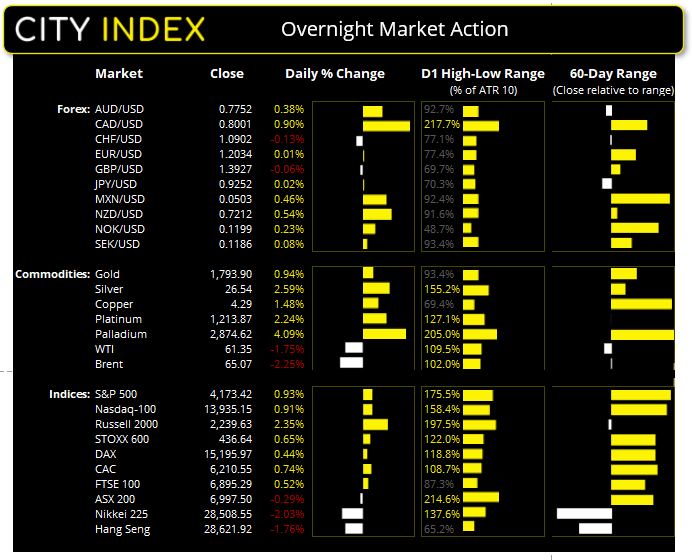

- UK's FTSE 100 index rose 35.42 points (0.52%) to close at 6,895.29

- Europe's Euro STOXX 50 index rose 35.95 points (0.91%) to close at 3,976.41

- Germany's DAX index rose 66.46 points (0.44%) to close at 15,195.97

- France's CAC 40 index rose 45.44 points (0.74%) to close at 6,210.55

Wednesday US Close:

- The Dow Jones Industrial rose 316.01 points (0.93%) to close at 34,137.31

- The S&P 500 index rose 38.48 points (0.94%) to close at 4,173.42

- The Nasdaq 100 index rose 125.848 points (0.91%) to close at 13,935.15

Learn how to trade indices

US Indices reverse Tuesday’s losses with bullish engulfing days

European indices tried to recoup Tuesday’s losses but settled for a minor bounce, yet Wall Street managed to eradicate their prior day’s losses with a convincing reversal. All major US indices rallied from the open and printed bullish engulfing candles by the close.

The VIX (volatility index) fell to 17.5 from a high of 19.7 on Tuesday to show anxiety was not sustained. 83.2% of S&P 500 stocks advanced, 16.7% declined, and nine out of eleven S&P 500 sectors were higher, led by basic materials and energy.

The Russel 2,000 saw the strongest rebound of +2.35%, of which value stocks rose +1.2% and growth stocks rallied +1.2%. The broader, technology focused Nasdaq composite recouped +1.2%, whilst the Nasdaq 100 and S&P 500 gained +0.91% and +0.93% respectively.

ASX 200 Market Internals

ASX 200: 6997.5 (-0.29%), 21 April 2021

- Healthcare (1.06%) was the strongest sector and Materials (-1.93%) was the weakest

- 8 out of the 11 sectors closed lower

- 58 (29.00%) stocks advanced and 126 (63.00%) declined

- 72% of stocks closed above their 200-day average

- 70.5% of stocks closed above their 50-day average

- 61.5% of stocks closed above their 20-day average

Outperformers:

- + 5.12% - IDP Education Ltd (IEL.AX)

- + 3.52% - Corporate Travel Management Ltd (CTD.AX)

- + 3.28% - Nufarm Ltd (NUF.AX)

Underperformers:

- -15.3% - Nuix Ltd (NXL.AX)

- -5.86% - Whitehaven Coal Ltd (WHC.AX)

- -5.58% - Challenger Ltd (CGF.AX)

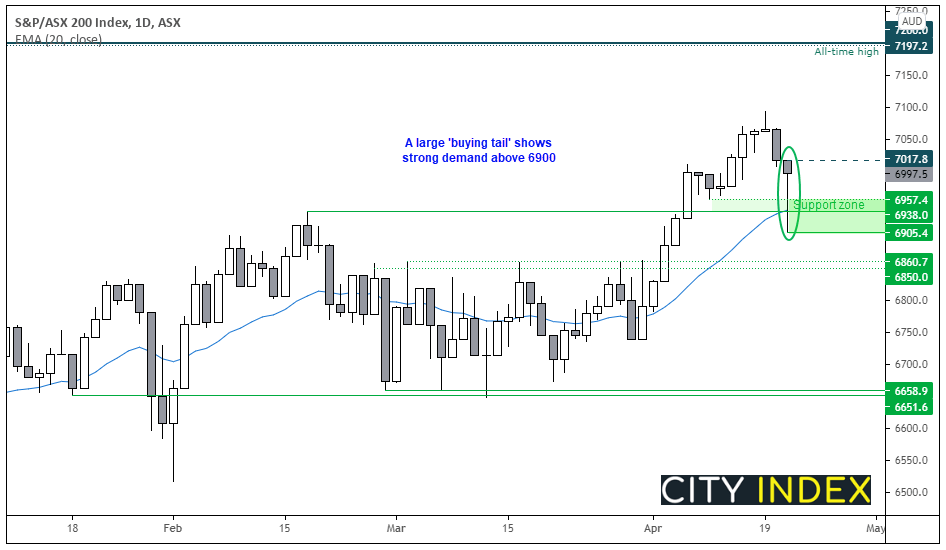

ASX 200 was on track for its worst close in two month’s yesterday, dragged down by technology and energy stocks. Yet it managed to recoup losses in the second half of the session to close just -0.3% down for the day, leaving a bullish hammer in its wake. Given the positive lead from Wall Street overnight and recovery on the ASX 200, we could be in for less severe start to today’s session.

Whilst the bullish hammer is larger than we’d like, there are key levels nearby which may help splice it up into a more manageable size. Note the lower wick (buying tail) pushed prices back above the 20-day eMA, prior record high and 6957 swing low, which provides a potential support zone between 6938 – 6957. It also suggests strong buying demand above 6900.

- A break above 7018 confirms yesterday’s bullish hammer.

- Our bias remains bullish above the 6938 – 6957 support zone.

- The initial target is 7100, followed by the previous record high (just below 7200).

Forex: BOC to move first?

The Bank of Canada (BOC) were more hawkish than expected at yesterday’s policy meeting. Whilst BOC kept rates unchanged at 0.25%, they tapered their weekly asset purchases to CA $3 billion from $4 bn and said it could hike rates in the second half of 2022 (brought forward from 2023). However, they also warned that rates won’t raise until economic slack is absorbed. Still, OIS pricing was showing markets expectation for BOC to hike ahead of other major central banks yesterday, and the meeting suggests that market pricing to be correct.

- Commodity currencies were at the top of the leader board, thanks to the revival of risk sentiment. The Canadian dollar was the strongest thanks to the dual combination of improved risk appetite and a hawkish BOC meeting. CAD crosses accounted for the baulk of volatility among FX pairs, with CAD/CHF and CAD/JPY at the top of the leader board and EUR/CAD and GBP/CAD at the bottom.

- The US dollar index (DX) probed, yet failed to break above, the 91.30/40 resistance zone and closed with a bearish hammer on the daily chart.

- EUR/USD tested yet held above 1.2000 support and remains in its bullish channel highlighted in yesterday’s European open report.

- EUR/NZD is probing key support at 1.6665, a break of which brings the 1.6490 / 1.6530 support zone into focus.

Learn how to trade forex

AU retail sales and NZ CPI beat expectations yesterday

Q1 CPI for New Zealand beat expectations yesterday, rising 1.5% YoY and 0.8% MoM. Whilst it’s not enough to expect any hawkish rection from RBNZ in isolation (although BOC’s hawkish stance may help), it’s a step in the right direction. Separately, Moody’s ratings agency kept their outlook on New Zealand as a ‘stable’ AAA rating, with little chance of a downgrade happening soon.

Australia can add retail sales to the growing list of strong data. Preliminary retail sales rose by 1.4%, beating 1% expected and rising from -0.8% previously. This comes after consumer confidence hit an 11-year high and their employment report smashed it out of the park. NAB’s business survey is up at 11:30 AEDT.

Whilst AUD/USD and NZD/USD are in holding patterns, NZD has the upper hand as AUD/NZD has slipped to six-week low. Yet with the 200-day eMA and bullish trendline between 20 – 50 pips away, we suspect downside could be limited for bears.

Commodities: Metals higher on a weaker dollar

Metals were mostly higher on the back of a weaker dollar, with silver rising +2.6% to a five-week high, and silver closing just above its 200-day eMA yet closing below 1800 after a +0.94% gain. Copper closed to its highest level since late February and palladium closed to a new record high.

Oil prices were lower again as a rise in covid cases continues to weigh on expected demand, with brent futures down -2.3% and WTI falling -1.75%.

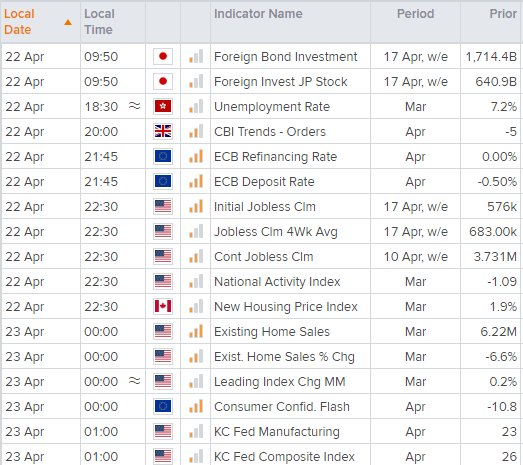

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Trade Ideas articles

Today 11:14 AM

Yesterday 11:00 AM

Yesterday 08:15 AM