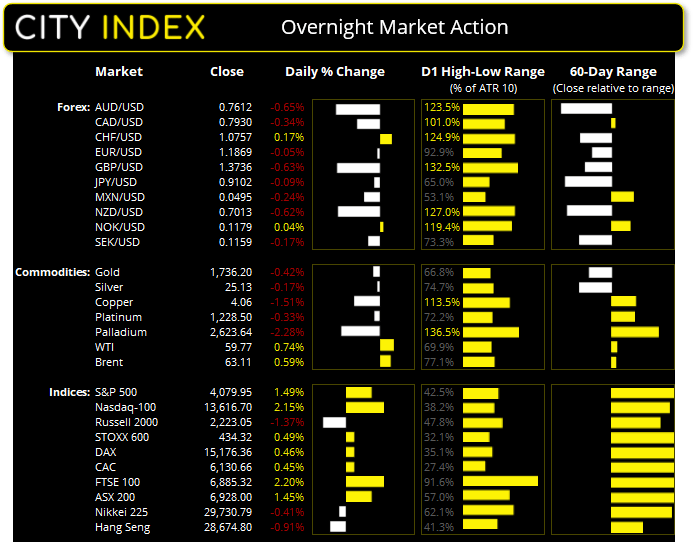

Asian Futures:

- Australia's ASX 200 futures flat, the cash market is currently estimated to open at 6,928.00

- Japan's Nikkei 225 futures are down -50 points (-0.17%), the cash market is currently estimated to open at 29,680.79

- Hong Kong's Hang Seng futures are down -207 points (-0.73%), the cash market is currently estimated to open at 28,467.80

Wednesday US Close:

- The Dow Jones Industrial rose 16.02 points (0.05%) to close at 33,430.24

- The S&P 500 index rose 6.01 points (0.15%) to close at 4,079.95

- The Nasdaq 100 index rose 38.242 points (0.28%) to close at 13,616.70

The Fed to remain ‘patient for ‘some time’

The FOMC retained their upbeat tone on the US economy in the minutes of their meeting. And this has since been backed up by a slew of strong data since their March meeting, including nonfarm payroll, job openings and surging PMI’s (with services PMI at a new record). This all points to a strong Q1 GDP print, which also ties in with the IMF’s (International Monetary Fund’s) expectation for the US to average 6.4% growth this year.

Yet despite all of this, the Fed still maintained their patient approach and that inflation will rise temporarily and the coronavirus remains a threat. It will also take “some time” to make substantial progress towards their 2%inflation and full employment targets. This remains at odds with markets which are now pricing in a first hike late 2022, although some members do see a case for raising rates sooner than others.

Indices set to open slightly lower

Wall Street posted minor gains overnight, although volatility was low overall. The Russell 2000 bucked this trend and fell -1.6% and closed below its 10 and 20-day eMA.

- The DAX is traying to close its gap just above 15,100 and closed lower for a second consecutive session, but this appears part of a natural and gentle retracement against a strong bullish trend.

- Asian markets are expected to open lower with Hang Seng and CSI300 currently down -0.73% and -0.78%. Nikkei 225 futures are a touch lower at -0.17%.

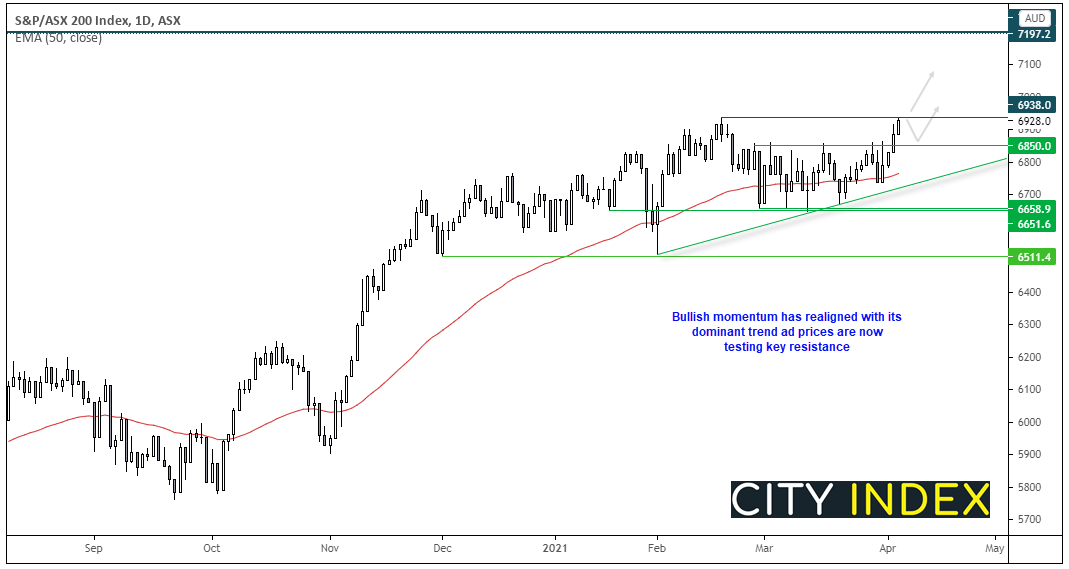

- All eyes are on the ASX 200 today to see it can break above 6938 resistance. Given volumes are rising and momentum has been bullish for four days, we could at least see an attempt to break higher today.

The daily chart on the ASX 200 is within an established uptrend, but it has effectively traded sideways since the end of February. Yet price action shows the dynamics may be about to change all of that. The index has traded higher for four consecutive sessions and its rate of change has picked up over this period. This shows a notable shift in price action behaviour which we think is favourable to a bullish breakout.

- A break above 6940 assumes bullish continuation.

- Bulls could either wait for this level to be confirmed as support or seek bullish setups on lower timeframes in line with the dominant trend.

- If resistance holds then we’d still be interest if prices were to form a base above 6850.

- Next major resistance is the record highs just below 7200.

Learn how to trade indices

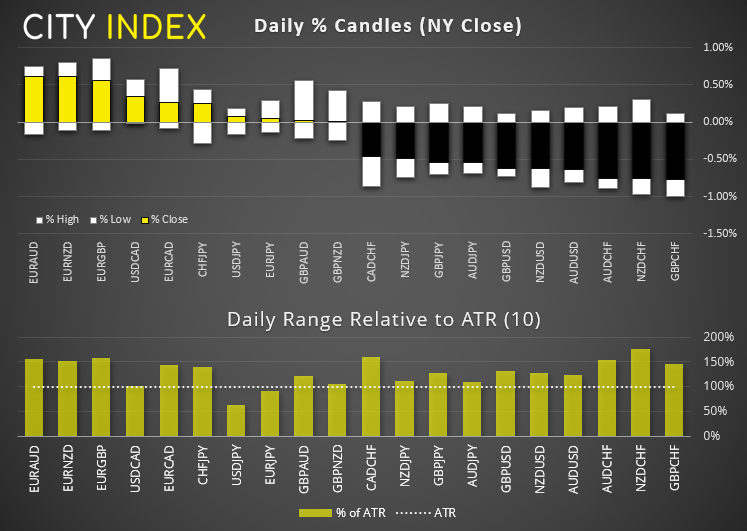

Forex: Another turbulent session for GBP

It was another turbulent session overnight, particularly among EUR, CHF and GBP pairs. The European dollar was broadly higher on the back of firmer PMI data, with the composite and service reads for Germany and the Eurozone all rising (although the service PMI for EZ remains below 50 to denote contraction).

The British pound remains sensitive to headlines surrounding the Oxford-AstraZeneca vaccine after reports continue to suggest it is indeed linked to rare blood clots on the brain for some patients. A full report is expect to be released later this week to confirm these suspicions, and GBP could move either way on the back of it.

The US dollar index (DXY) printed a small bullish candle although prior support capped as resistance at 92.50. Conversely, EUR/USD produced a bearish pinbar which suggests both markets may provide minor retracements against their recent moves.

- GBP/JPY had another volatile session (to bear’s advantage), traded beneath the 150.96 target outlined in yesterday’s European Open report and stopped just shy of the 150.55 support level. A period of consolidation today appears likely but our core view remains bearish and for bears to try and fade into rallies.

- EUR/NZD was a strong performer overnight and isn’t too far away from our initial target around 1.7000/72, outlined in yesterday’s Asian Open report. Given yesterday’s strong move and two indecision candles on the four-hour chart near its highs, we fancy its odds of consolidating or retracing towards 1.6866 support before resuming to its bullish trend.

- USD/CAD saw an intraday break above trendline resistance and Monday’s bearish engulfing / outside candle, yet closed bac under both. Whilst the bearish bias is now in ice (until momentum turns south) we can also monitor for a potential break above 1.2647 which would suggest a trend reversal.

- AUD/USD printed a bearish outside candle and found resistance at its 50-day eMA. We have revised the bearish neckline of the head and shoulders pattern which projects a target around 0.7240.

- NZD/USD also produced a bearish outside day and we think the swing high is in place at 0.7070. Next support is at 0.6945, a break beneath of which brings the 0.6800 support into focus.

Learn how to trade Forex

Commodities lack direction

The Thomson Reuters CRM commodity index remains in a strong uptrend yet within a corrective phase. Down just -6.6% from it February high, price action remains choppy yet confined to a range, which is also apparent across other commodities.

- Oil prices are essentially a more volatile version of the CRB index, with WTI and brent futures moving sideways in a volatile range – therefore range trading strategies remain preferred until trends develop once more. WTI trades just below $60, in the lower third of its 57.25 – 62.27 range and brent sits at 36.10, around the midway point of its own 60.32 – 65.50 range. Perhaps they will become of interest to mean reversion traders if they can trade near support or resistance without breaking them.

- Metals were lower overnight on the back of a stronger dollar, and palladium led the declines with a -2.4% fall. Platinum was less effected with its -0.3% fall and our bias remains bullish above the 1195 – 1200 support zone outlined yesterday.

- Gold printed a bearish inside day overnight and currently trades around 1737. Until we see a clear break above 1764 then it makes being bullish on the daily timeframe hard from a reward/risk perspective. On an intraday basis, it trades midway between 1720 support and 1755 resistance - and it really could be a flip of the coin as to which one we test first.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Latest ASX articles

April 16, 2024 10:19 PM

April 10, 2024 11:24 PM

April 9, 2024 11:02 PM