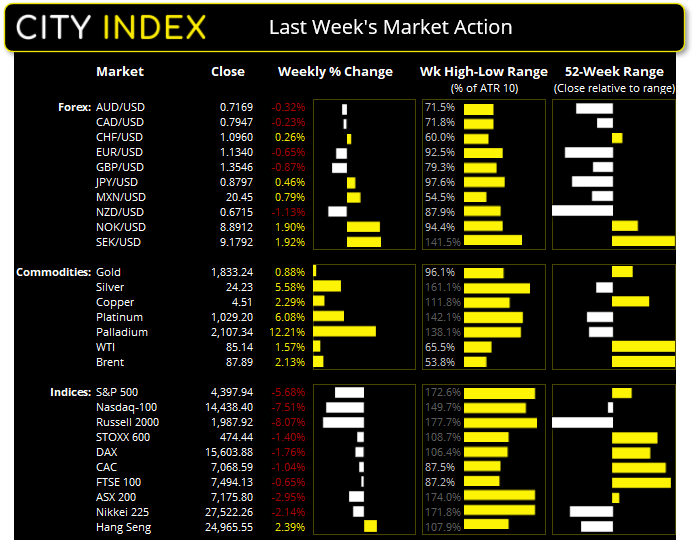

US equities suffered one of their worst weeks since the pandemic

Wall Street continued its downwards trajectory on Friday with the S&P 500 closing marginally beneath its 200-day eMA and at the low of the day and week. Falling over -5%, it was its worst week for the index since March 2020. Ultimately, it was a sea of red for equity traders last week with the Nasdaq 100 falling -7.5% with around 40% of its constituents down early 50% from their 52week highs and the Russell 200 falling -8.1%. The reality of a hawkish Fed seems to finally be sinking in.

Japanese yen was the strongest currency amidst risk-off trade last week

The risk-off tone (to put it lightly) helped the Japanese yen take the top spot among FX majors last week with the Swiss franc come in a close second. The Kiwi dollar and British pound were the worst performers. GBP/USD formed a bearish engulfing week and closed beneath its 200-day eMA. AUD/JPY closed beneath its 200-day eMA during its worst session this year.

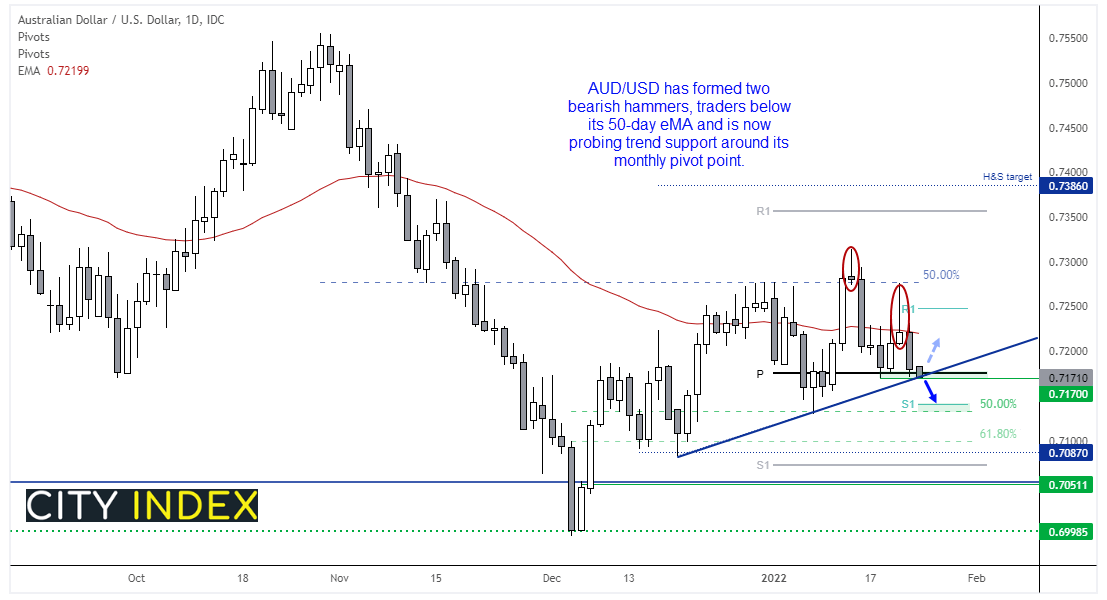

The Aussie probes trend support

AUD/USD is probing trend support near a cluster of levels including the monthly pivot point and 0.7170 low. The pair has been trying to grind out a to for a few week with a bearish hammer marking a top around 0.7300, and a second bearish hammer forming a lower high and respecting the 50% retracement level as resistance last week. The 50-day eMA also capped as resistance for most of last week so we now await bearish momentum to return. A break beneath trend support brings the support zone around 0.7133 into focus. Until then be on guard for a bounce from support, although the bias is for an eventual break lower (sooner or later).

Read our guide on the Australian Dollar

Gold pulls back (slightly)

Despite the risk-off tone gold traded lower on Thursday and Friday, although its lack of bearish follow-through suggests it’s a minor pullback ahead of its next leg higher. The spot price now trades slightly below the 1834 support level but we’ll continue to see if momentum can turn higher and challenge a resistance zone around 185555 this week.

Oil bulls set to return?

We saw a bit of a shakeout around $85 on WTI last week and, despite a weak start on Friday, bulls regained control and formed a bullish hammer on the daily chart by Friday’s close. However, take note of the bearish trendline which was breached on Friday on the intraday chart and price action is crawling up the inside of it. SO whilst prices remain below the October highs we are also on guard for another leg lower.

Hang Seng to break above 25k?

The HSI was one of the few indices to trade higher last week, after further easing from PBOC helped bolster and arguably oversold index. It broke out of a flag pattern (which itself invalidated a long-term bearish trendline) which projects a target around the October high. Closing just below 25k on Friday we now wait to see if it can break above that key level to continue higher towards its initial target.

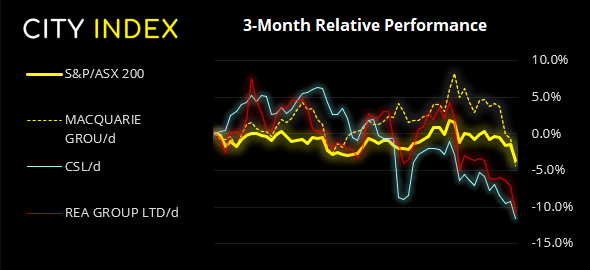

ASX 200

Friday was its second worst session since January 2021 and prices closed to their lowest level since June 2021 and well below the 200-day eMA. 7145 is a key level of support for bulls to defend today. Technology stocks have been the worst performers this month so far, falling nearly -15% with healthcare down around -10%. Only utilities and materials sectors have posted gains in January so far, up around 3% and 4.9% respectively.

ASX 200: 7175.8 (-2.27%), 23 January 2022

- Materials (-3.52%) was the strongest sector and Telecomm Services (-2.17%) was the weakest

- 11 out of the 11 sectors closed lower

- 5 out of the 11 sectors outperformed the index

- 184 (92.00%) stocks advanced, 10 (5.00%) stocks declined

Outperformers:

- +4.74% - Summerset Group Holdings Ltd (SNZ.AX)

- +2.09% - Boral Ltd (BLD.AX)

- +1.03% - Northern Star Resources Ltd (NST.AX)

Underperformers:

- -3.76% - Macquarie Group Ltd (MQG.AX)

- -2.48% - CSL Ltd (CSL.AX)

- -3.62% - REA Group Ltd (REA.AX)

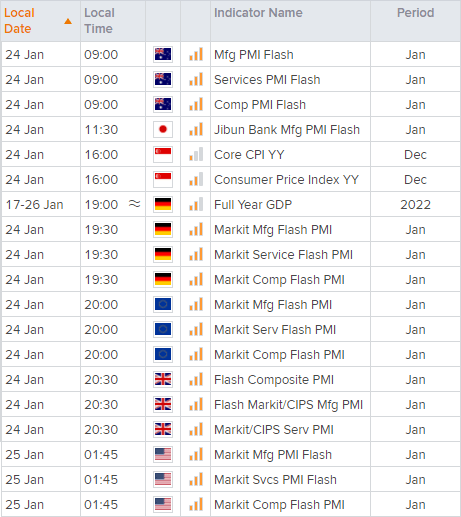

Up Next (Times in AEDT)

Flash PMI’s are the main theme for traders today. Markit Economics will release PMI data for manufacturing, services and the composite read for Australia at 09:00 AEDT, with Japan releasing their manufacturing report at 11:30.

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Trade Ideas articles

Today 04:00 PM

Today 11:30 AM

Today 08:18 AM