Japan’s GDP (growth domestic product) surprised to the upside in Q4 on Monday, rising 12.7% versus 9.5% forecast, up from 22.9% prior. This also saw the annualised rate rise to 3% compared with 2.3% forecast, although down from 5.3% in Q3. Strong exports and a rebound in capital expenditure were the main divers behind the positive headline figures. It also means Japan are the latest Asian country to perform better than expected during their recovery, following Singapore and Thailand’s upside GDP surprises. Ultimately, this is good for global growth, so we expect sentiment to remain elevated and help support equities and yields unless a new catalyst says otherwise.

The Yen and Nikkei 225 stole the show

European bourses took a positive lead from Asia to see the DAX and STOXX 600 rally 1.5% and 1.3% respectively. The FTSE 100 was the strongest index over the European session, closing 2.5% higher during its second most bullish day this year. US equity markets and several key metals markets were closed due to Presidential day in the US, although traders are expected to return to their desks later today.

But it was the Nikkei 225 which stole the show and closed above 30,000 for the first time in 30 years. Closing 1.9% higher yesterday, it has currently notched up an impressive 8.6% this month so far and, with no immediate signs of a top in sight, bears remain side-lined.

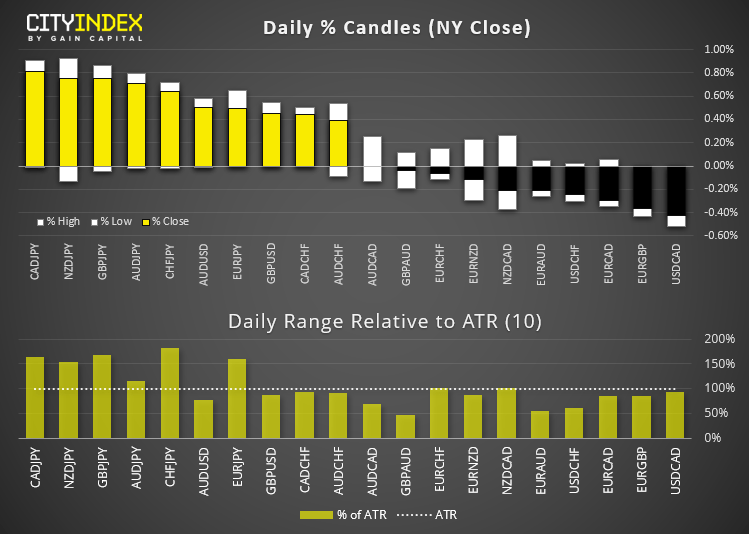

The Japanese yen was the weakest currency overnight as a risk-on vibe continued to influence sentiment. Six of the 28 FX pairs majors and crosses we track exceeded their daily ATR’s (average true ranges), all of which were yen pairs. CAD/JPY was the biggest mover as higher oil prices helped to boost the Canadian dollar. AUD/JPY rose to its highest level since December 2018 and CHF/JPY closed above 118 for the first time since February 2018. USD/CAD was the weakest pair thanks to a slightly weaker dollar, although volumes were thinner during the North America session due to their 3-day weekend.

WTI breaks above $60

Reports that Saudi Arabia had found and destroyed an explosive-laden drone on Monday sent oil prices higher, adding a geopolitical driver to the mix when oil had already been enjoying an extended trend thanks to the global vaccine rollout. It was the first time WTI futures have traded above $60 since January 2020, although the bearish pinbar which closed just above $60 warrants close attention as a clear break beneath this key level could prompt an overdue correction.

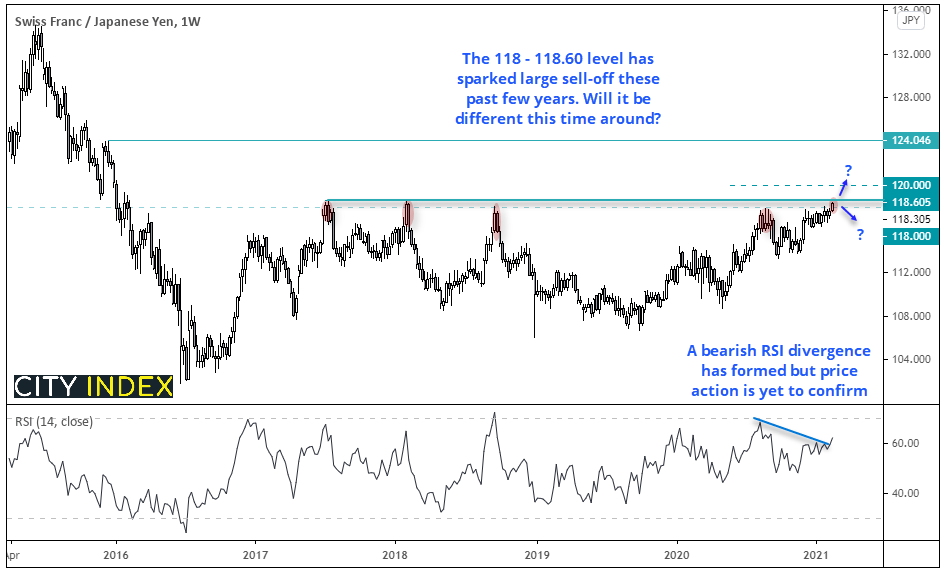

CHF/JPY: All eyes on 118.60

Since the July 2017 high, CHF/JPY has effectively rolled over each time it tried to close convincingly above 118. What makes this particularly interesting is that both the Swiss franc and Japanese yen are ‘closely watched’ by their respective central banks. Given the 118 area has provided solid resistance these past few years and that Japan’s PM reiterated just yesterday how closely they are watching the FX market, we could favour its potential to roll over from current levels. A bearish divergence with RSI also favours this potential scenario. However, price action is yet to confirm a top and we should also take note of the multi-year rounding bottom formation which denotes a potential (and large) bullish breakout over the coming month/s.

Either way, We’d suggest bulls keep a very close eye on communication from SNB (Swiss National Bank) who don’t want their currency too strong and BOJ (Bank of Japan) who don’t want theirs too volatile.

- A break or close above 118.60 could signal further gains in line with the multi-month bullish trend.

- The next major resistance is all the way up at 124 but we’d focus on 120 over the near-term.

- Bears could look for signs of reversal pattern or a momentum shift around 118.60 resistance. Around current levels, the reward to risk potential appears high for bears, although a bearish signal is yet to materialise.

Up Next (Time in Sydney GMT +11)

- Volumes in Asia are expected to remain lower than usual due to Chinese Lunar New Year through to Wednesday.

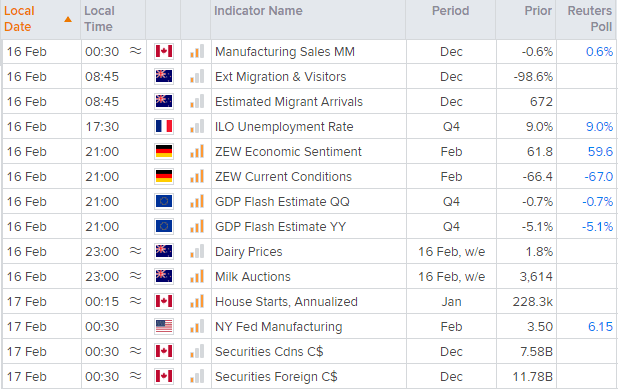

- Germany’s ZEW economic data and European flash GDP are the main economic events today, which places Euro pairs, DAX and Stoxx indices into focus for news traders.

Watchlist update:

AUD/USD: Prices have exceeded our initial target of 0.7764 as outlined in last Monday’s report and closing in on the 0.7820 high. Bulls could trail stops from here. We’d be happy to step aside until a fresh bullish opportunity arises with a better reward to risk ratio.

GBP/CHF: After a 5-day correction, bullish momentum returned above the support zone highlighted in last Tuesday’s report. Having now broken to a new cycle high the net major resistance zone (target) is around 1.2700 1.248 – 1.2530.

EUR/USD: Price action is consolidating above the 50-day eMA on the daily chart. The near-term bullish bias remains bullish engulfing low around 1.2043, and a break above 1.2190 brings the 1.2350 high into focus.

USD/CHF: A second bearish hammer has formed on the daily chart, which also respected the 38.2% Fibonacci retracement level around 0.8950 and closed below the 50-day eMA. As mentioned in yesterday’s report, a break below 0.8830 brings the 0.8838 and 0.8760 lows into focus.

AUD/CAD: Removed from watchlist. A bearish outside candle yesterday was the second consecutive session with a false break above 0.9855 resistance, warning of a potential bull-trap around a key level.

Latest market news

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM