Asian Futures:

- Australia’s ASX 200 futures rose 13 points (0.173%), the cash market is currently estimated to open at 7541.5

- Japan's Nikkei 225 futures have risen 310 points (1.04%), the cash market is currently estimated to open at 29969.89

- Hong Kong's Hang Seng futures are up 56 points (0.21%), the cash market is currently estimated to open at 26219.63

European Friday close:

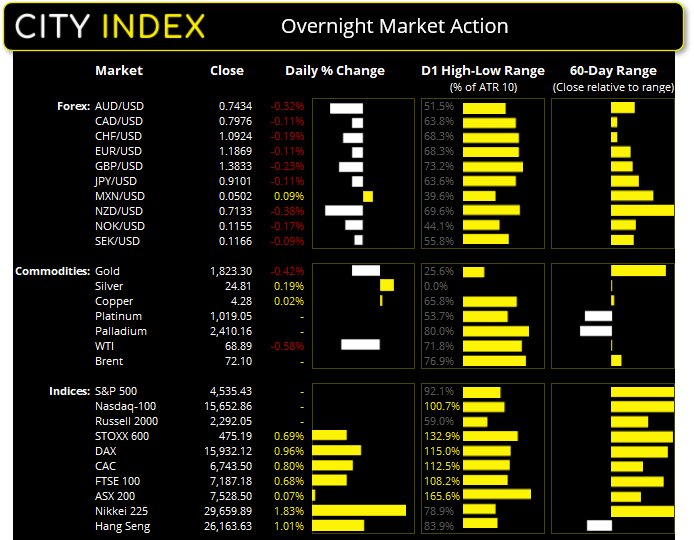

- UK's FTSE 100 index rose 48.83 points (0.68%) to close at 7187.18

- Europe's Euro STOXX 50 index rose 44.15 points (1.05%) to close at 4246.13

- Germany's DAX index rose 150.92 points (0.96%) to close at 15932.12

- France's CAC 40 index rose 53.51 points (0.8%) to close at 6743.5

US Futures:

- S&P 500 E-minis are index up 10 points (0.22%)

- Nasdaq 100 E-minis are index up 49.75 points (0.32%)

- Dow Jones E-minis are index up 78 points (0.22%)

Wall Street was closed yesterday due to US Labor Day, but that did not prevent European indices closing in on their highs. The STOXX 600 printed a bullish engulfing day after finding support at its 20-day eMA and the DAX rose to a 4-day high after Friday’s Doji found support at its 50-day eMA. Even the FTSE rose to a 2-week high and printed a bullish engulfing candle although 7200 remains to be an untested level during its choppy round of minor gains.

The ASX 200 once again found support around the daily bullish trendline, August lows and closed above the 50-day eMA. Rallying into the close a ‘buyer tail’ has formed (long lower wick) so if prices can break above 7556 (sooner than later) then its bullish trend is assumed to be re-established.

Learn how to trade indices

ASX 200 Market Internals:

ASX 200: 7528.5 (0.07%), 06 September 2021

- Information Technology (1.15%) was the strongest sector and Materials (-1.09%) was the weakest

- 8 out of the 11 sectors closed higher

- 4 out of the 11 sectors closed lower

- 7 out of the 11 sectors outperformed the index

- 108 (54.00%) stocks advanced, 80 (40.00%) stocks declined

- 69.5% of stocks closed above their 200-day average

- 64.5% of stocks closed above their 50-day average

- 62% of stocks closed above their 20-day average

Outperformers:

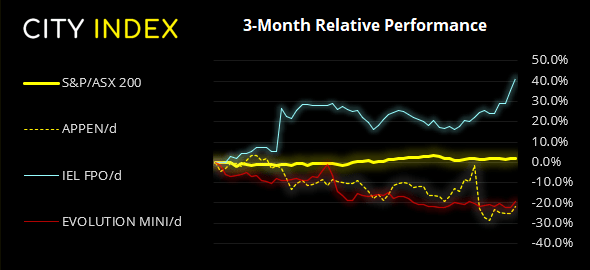

- + 4.56% - Appen Ltd (APX.AX)

- + 4.29% - IDP Education Ltd (IEL.AX)

- + 3.85% - Evolution Mining Ltd (EVN.AX)

Underperformers:

- -10.9% - Fortescue Metals Group Ltd (FMG.AX)

- -5.84% - Pro Medicus Ltd (PME.AX)

- -5.31% - Pilbara Minerals Ltd (PLS.AX)

Forex:

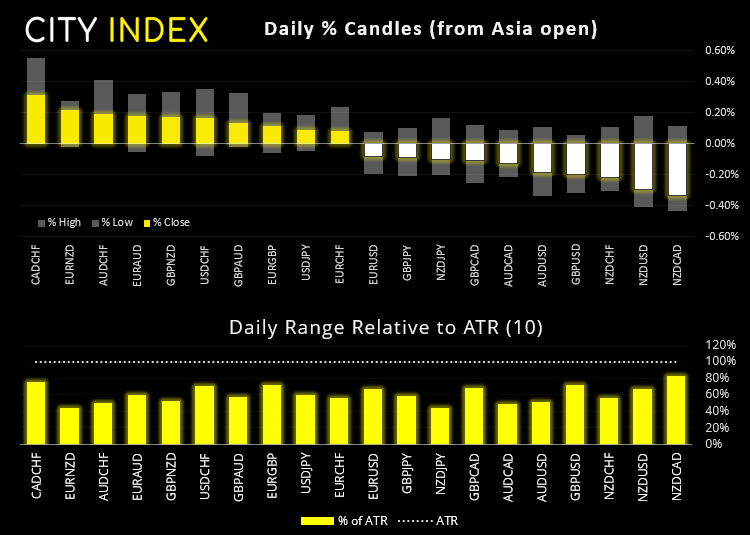

With key US markets closed due to Labor day in the US there was no major economic news released after the European session. The US dollar retracted overnight and was the strongest major currency, during a session light on news. We suspect it’s a case of technical repositioning over anything else at this stage. This helped the US dollar index (DXY) rise back above its 200-day eMA although went on to close back beneath it.

This also allowed EUR/USD to break beneath Friday’s bearish hammer and its 200-day eMA capped as yesterday’s high, so we may find a little more noise around current levels being around such an important technical level.

GBP was weaker after PMI data revealed the construction sector expanded at its slowest pace since February and further supports concerns that the post-reponing economic surge has peaked.

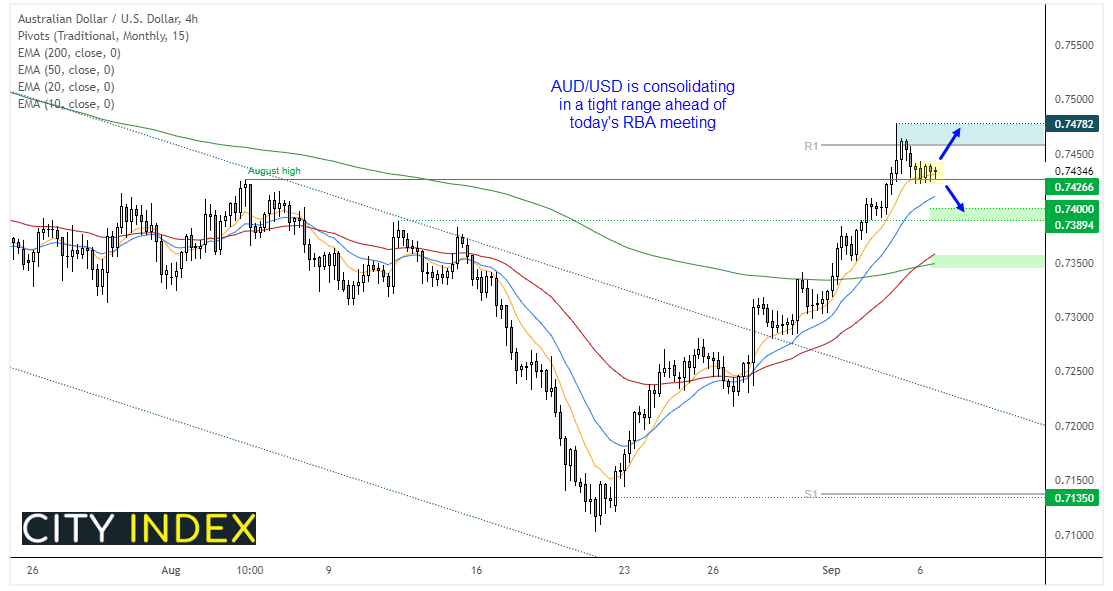

AUD/USD traded in a tight range and caught between the August high and monthly R1 pivot point, after failed to close above its 200-day eMA last week. RBA hold their monetary policy meeting at 14:00 AEST and, whilst there’s no expectation for a rate change, it’s possible we may see the RBA walk back their decision to begin tapering. And that could weigh on the Australian dollar despite its recent surge fuelled by short covering.

We can see on the four-hour chart that prices are consolidating above the August high. Should RBA make no changes then bulls may be tempted to return above the August high, yet if tapering is reinstated then the support zone around 0.7400 comes into focus. EUR/AUD is also one to watch as it is trying to build a base above 1.5900 support.

Learn how to trade forex

Commodities:

Gold retraced slightly from Friday’s highs and, whilst the pennant pattern is no more, the structure on gold’s four-hour chart remains structurally bullish. We suspect a breakout stands a better chance of materialising once the US dollar index moves lower, although US data does not heat up until Thursday’s JOLTS job openings.

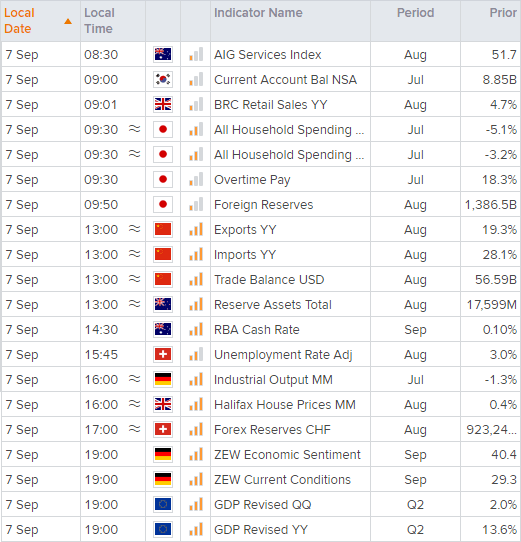

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM