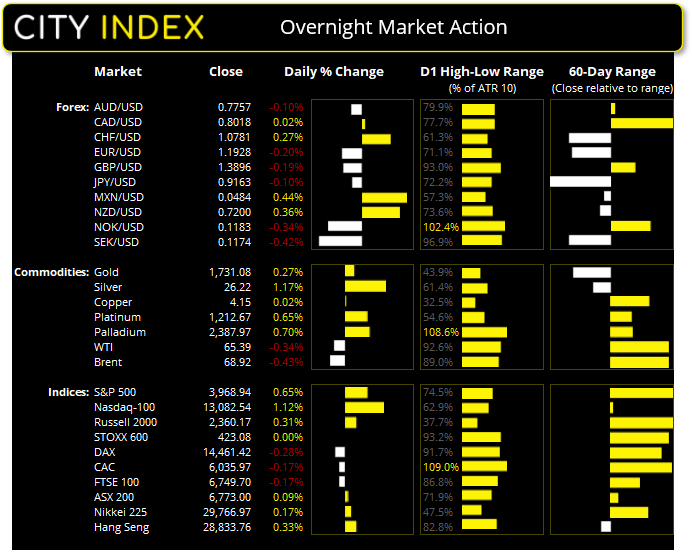

Asian Futures:

- Australia's ASX 200 futures are up 26 points (0.38%), the cash market is currently estimated to open at 6,799.00

- Japan's Nikkei 225 futures are up 120 points (0.41%), the cash market is currently estimated to open at 29,886.97

- Hong Kong's Hang Seng futures are up 159 points (0.55%), the cash market is currently estimated to open at 28,992.76

UK and Europe:

- The UK's FTSE 100 futures are up 11 points (0.16%)

- Euro STOXX 50 futures are up 5 points (0.13%)

- Germany's DAX futures are down -2 points (-0.01%)

Monday US Close:

- The Dow Jones Industrial rose 174.82 points (0.53%) to close at 32,953.46

- The S&P 500 index rose 25.6 points (0.65%) to close at 3,968.94

- The Nasdaq 100 index rose 145.246 points (1.12%) to close at 13,082.54

US equities enjoyed further gains overnight as lower yields gave them headroom to breath. Although volatility was on the low side as we approach Wednesday’s FOMC meeting. The Nasdaq 100 was Wall Street's stronger performer at +1.12% and closed to a 9-day high. Now back above its 50-day eMA, we remains bullish above 12,755 support and the bias is for a re-test of 13,300.

The S&P 500 cash index printed a fresh record high as it inched its way closed to its 4,000 milestone. Although the S&P E-mini futures are yet to follow suit and sit anchored to its current record high, so we’d like to see some follow through from the futures market to remains confident the cash index can hold on to its lofty heights.

Indices: Vaccine halts weigh on Europe

European indices came under a little pressure at their highs overnight. Investors were concerned on reports that Germany, along with several other companies had halted the use of the AstraZeneca vaccinations based on claims it causes blood clots in some patients. A bearish outside candle formed on the DAX and CAC daily charts whilst a small bearish hammer formed on the Euro STOXX 50. As the US are yet to authorise the use the vaccine, the impact of the news was limited to European bourses. AstraZeneca have said there’s no scientific evidence of the claims and the WHO (World Health Organisation) continue to support the use of the vaccine, saying that blood clot incidence is low.

It is not uncommon to see clinical trials or rollouts paused, and it is not the first time this has happened during the ‘recovery phase’ of the pandemic. And once further tests are carried out we shall see if these concerns turn to bigger concerns, in which case European bourses could face much more pressure.

Forex: Small ranges, USD mixed

NZD and CHF were the strongest majors overnight whilst EUR and JPY were the weakest. The US dollar was slightly mixed and sat in the middle of the pack, whilst the US dollar index (around 57% weighted to the Euro) etched out a small gain and sits around 0.1% higher.

- EUR/USD made a half-baked attempt to fall down to 1.1900 yet the move lacked bearish follow-through. We suspect rages may remain tight on EUR/USD without a fresh catalyst ahead of the FOMC meeting.

- USD/JPY tapped a fresh high 9-month high with a small bullish candle (of the bearish candle variety) right within a supply zone. The last time we saw USD/JPY trade in this area it marked the beginning of a -6.5% move. Whether history will repeat, only time can tell, but markets are clearly hesitant to extend its bullish move ahead of Wednesday’s FOMC meeting.

- AUD/NZD produced a bearish engulfing candle on the daily chart, after failing to hold above 1.0800. Previously we have seen bearish reversal candles form tops in this area before falling between -180 and -300 pips over a few sessions. So we remain bearish on AUD/NZD beneath last week’s high.

- We discussed AUD/CAD in yesterday’s Asian open report, although it is currently on track for a false break below 0.9570 support with a small bearish hammer, which closed back above the potential breakout level. Whilst it is not enough to invalidate the bearish structure of the daily chart, it is enough to warrant caution around current levels. Bears could continue to monitor its bearish potential and re-enter a break beneath yesterday’s low with a tighter stop above its high, assuming prices do not rally from here of course.

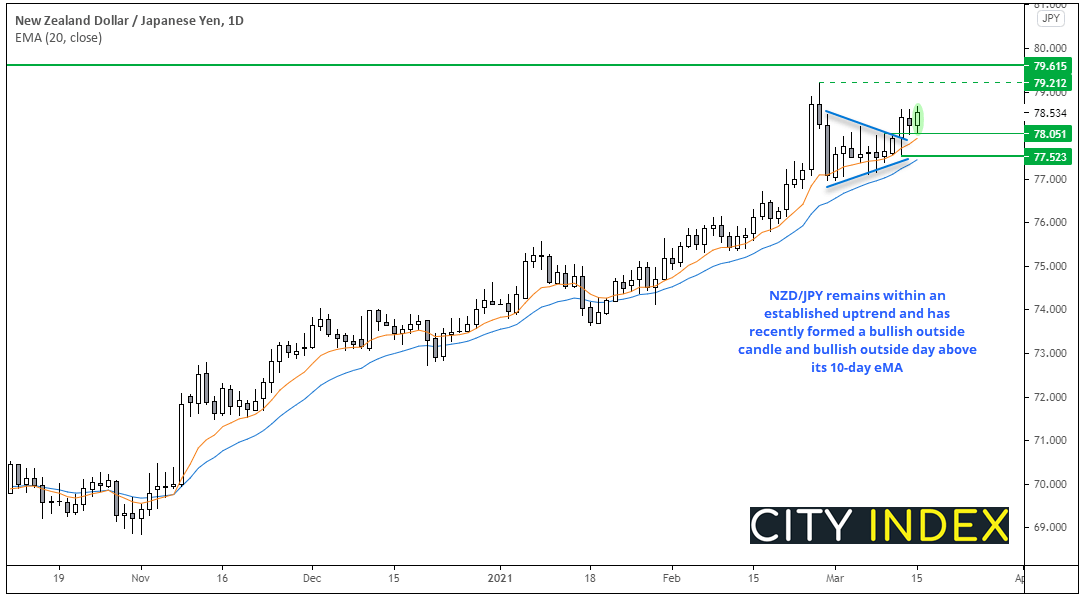

NZD/JPY or AUD/NZD?

The daily structure on NZD/JPY remains firmly bullish and is trying to move further beyond its 10-day eMA. Yesterday’s candle closed with a smallish bullish engulfing candle and its low reaffirmed nearby support to be at 78.05.

Thursday’s candle saw a strong bullish candle break out of a small pennant-like pattern, so we’re now looking for prices to trade higher. Take note that NZD tends to benefit when RBA send dovish signals, and RBA’s minutes are released this morning.

- Bulls could enter a break above yesterday’s high to assume bullish continuation

- Our bias remains bullish above the 77.52 low (bullish outside candle) but 78.05 can also be used to fine-tune risk management

- The initial target is the 79.21 high but the April 2018 high also makes a viable target

Commodities: Metals outshine oil

Oil prices moved lower for a second session, with bearish outside days forming on brent and WTI. It was just yesterday we noted that the longer prices remain stuck below recent highs on low volatility, the greater the odds of a bearish ‘spike of sorts’. So, for now we’ll step aside from oil until we are convinced a corrective low has arrived or it breaks to fresh highs.

Metals were on the rise overnight, with silver taking the lead with a 1.8% gain and now trading at 26.22. Gold posted a minor gain of 0.27% and is back above 1730 but we’d need to see prices break the 1740 swing high for a clearer run to our 1760 target.

Platinum nudged its way to an 11-day high with the session low respected its 10 and 20-day eMA as support. Bullish momentum was hardly ground-breaking though. Palladium is trying to break above 2,400 at the time of writing although prices have been broadly ranging between 2,200 and 2,500 since Q4, so price action remains choppy overall.

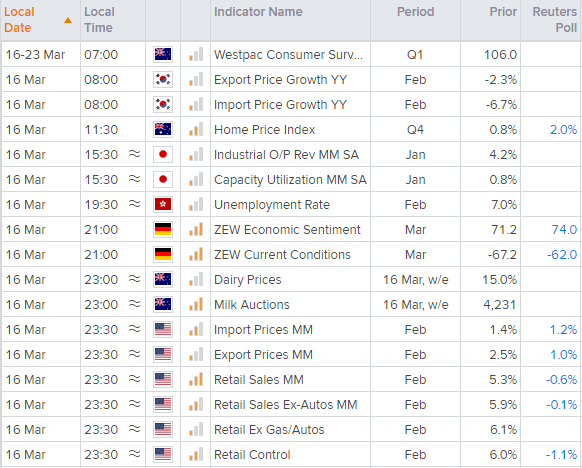

Up Next (Times in AEDT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- The Reserve Bank of Australia (RBA) release their minutes of their March cash rate meeting at 11:30 AEDT. Otherwise, we’re in for a mostly quiet session in Asia.

- Germany’s ZEW economic index warrants a look for euro news traders. Especially now Germany has halted the use of AstraZeneca’s vaccine, as the DAX and euro may become more sensitive to a weaker ZEW report.

Latest market news

Today 08:33 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM