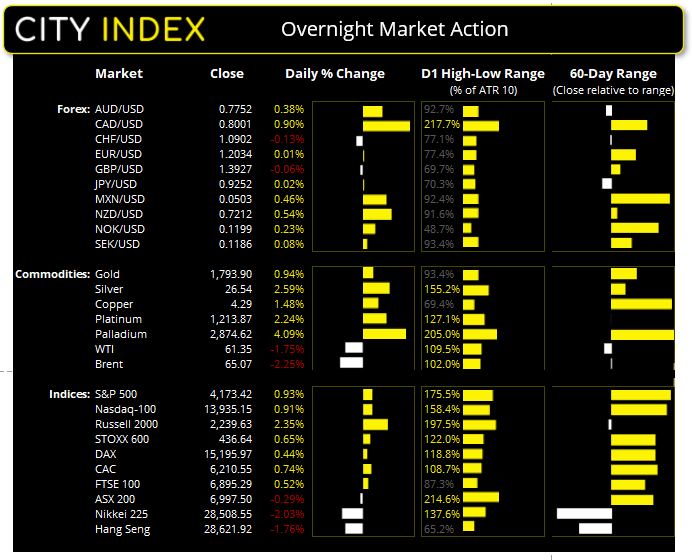

Asian Futures:

- Australia's ASX 200 futures are down -15 points (-0.21%), the cash market is currently estimated to open at 7,040.40

- Japan's Nikkei 225 futures are down -220 points (-0.76%), the cash market is currently estimated to open at 28,968.17

- Hong Kong's Hang Seng futures are down -38 points (-0.13%), the cash market is currently estimated to open at 28,717.34

UK and Europe:

- UK's FTSE 100 index rose 42.95 points (0.62%) to close at 6,938.24

- Europe's Euro STOXX 50 index rose 38.39 points (0.97%) to close at 4,014.80

- Germany's DAX index rose 124.55 points (0.82%) to close at 15,320.52

- France's CAC 40 index rose 56.73 points (0.91%) to close at 6,267.28

Thursday US Close:

- The Dow Jones Industrial fell -321.41 points (-0.94%) to close at 33,815.90

- The S&P 500 index fell -38.44 points (-0.93%) to close at 4,134.98

- The Nasdaq 100 index fell -172.794 points (-1.24%) to close at 13,762.36

US indices wobble on Biden’s eye-watering tax proposal:

That the Biden administration wanted to raise taxes does not come as a surprise. But what was unexpected (at least judging by the market’s reaction) is plans to almost double capital gains tax to 39.6% for earners over $1 million. Of course, Biden still needs to get this over the line. But he is clearly playing hardball. And, given high earners are more likely to be active on Wall Street to some degree or other, the news weighed on prices.

The Nasdaq-100 was biggest decliner on Wall Street, falling -1.24% and giving back all of Wednesday’s ‘recovery’ gains to re-test the low of the week. Now back beneath its 10-day eMA, it appears vulnerable to further losses as its stumbles into the weekend. The S&P 500 fell -0.92%, dragged down by materials, energy and technology stocks. All but the health care sector closed in the red. The Russell 2,00 held up quite well in comparison, falling just -0.3% by the close.

It was a better close for Europe which saw the DAX, CAC and STOXX 50 trade to a two-day high and close firmly above their 10-day eMA’s. Still, in each case these markets are on track for weekly bearish hammers to form at their highs, which is a slight concern if we use the rule of thumb that the higher the timeframe, the more reliable the pattern.

As for the ASX, we doubt US tax news will weigh on it much today. Yesterday, the ASX 200 broke above Wednesday’s hammer high from the get-go, which further suggests the ‘buying tail’ above 6900 has conviction. Barring a sudden shift in sentiment (locally or globally), the bias remains for a run for, and beyond, 7100. However, also take note that like its European counterparts, the ASX 200 is also forming a large bearish hammer, so it would need to close convincingly above this week’s highs to help eradicate that technical warning next week. Ultimately, today’s bias remains bullish above yesterday’s low.

ASX 200 Market Internals:

ASX 200: 7055.4 (0.83%), 21 April 2021

- Heath Care (1.74%) was the strongest sector and Energy (-0.57%) was the weakest

- 5 out of the 11 sectors outperformed the index

- 9 out of the 11 sectors closed higher

- 6 hit a new 52-week high, 3 hit a new 52-week low

- 76.5% of stocks closed above their 200-day average

- 66.5% of stocks closed above their 20-day average

Outperformers

+ 9.74% - Megaport Ltd (MP1.AX)

+ 5.76% - Monadelphous Group Ltd (MND.AX)

+ 5.73% - Westgold Resources Ltd (WGX.AX)

Underperformers:

-23.05% - Redbubble Ltd (RBL.AX)

-10.8% - Pilbara Minerals Ltd (PLS.AX)

-4.32% - Blackmores Ltd (BKL.AX)

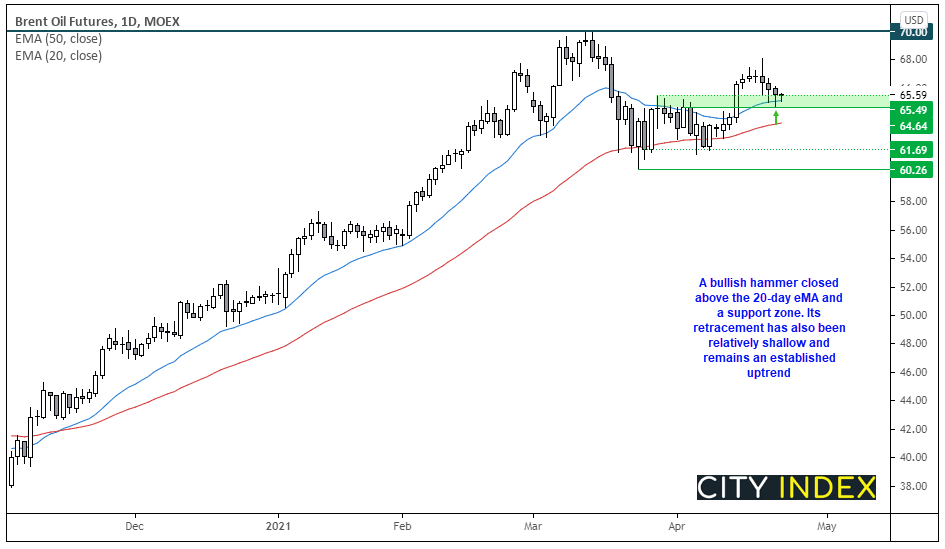

Commodities: Oil forming a base?

Metals were lower overnight as fears of capital gains tax (and a stronger USD) squeezed Wall Street traders. Gold is back below its 200-day eMA, which is usually the case upon its firt attempt to break it and silver stumbled from the March 18th resistance level. Palladium was also lower after reaching our inverted H&S (head and shoulders) target at 2895.

We suspect a base is forming on oil prices. WTI found support above 60.38 (last Wednesday’s low), adding significance to this support level for the bull-camp and making it a pivotal level to watch. Brent produced a bullish hammer and closed above the 20-day eMA and on 65.50 support, after an intraday break beneath it. Given its long-term uptrend our bias is bullish, and brent is favoured over WTI as its recent retracement has been the shallower of the two.

- The near-term bias remains bullish above yesterday’s low.

- A break above yesterday’s high confirms the bullish hammer.

- Target is open, and also time dependant (depending on time horizon and appetite for risk) as heading into the weekend.

Learn how to trade indices

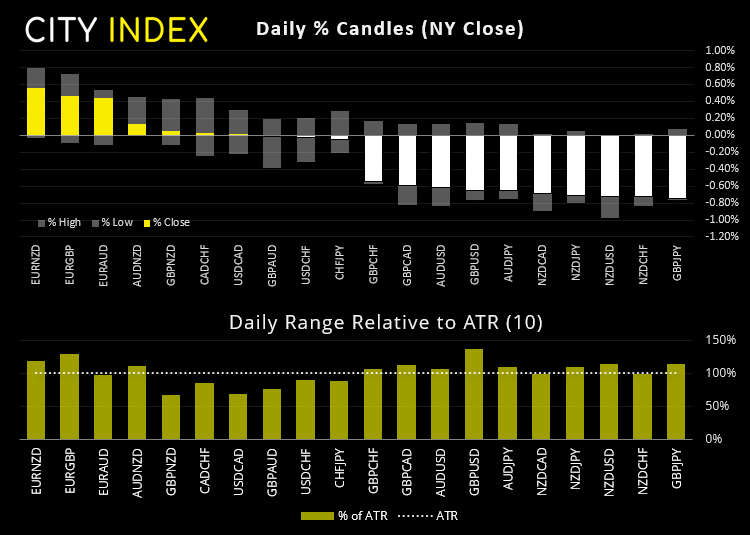

Forex: Jobless claims fall, dollar catches a safe-haven bid

The US dollar was the strongest major, thanks to a combination of weaker equity prices and better than employment data. US jobless claims fell to a 13-month low of 574k, down from 765k previously, which more than beat the estimated rise to 617k claims.

- The Japanese yen was the second strongest major thanks to safe-haven flows amid falling stock prices. NZD, GBP and AUD the weakest majors as risker assets were sold.

- This placed GBP/JPY as the worst performer, whist EUR/NZD as the strongest following yesterday’s ECB meeting. As expected, the ECB left policy unchanged, although as the dollar caught a bid it weighed on EUR/USD.

- A bearish outside candle formed on the daily chart and prices saw an intraday break of the bullish channel highlighted yesterday, yet prices remain above the key level of 1.2000.

- GBP/USD failed to hold onto its base above 1.3900, making this level an area for bears to consider fading into and brings the 1.3716 low into focus.

- AUD/USD fell to a six-day low and probed 0.7700 support. NZD/USD fared slightly better with a fall to a four-day low and appears to be the marginally stronger of the two (as seen with a falling AUD/NZD).

- AUD/JPY continues to suggest it is topping out on the daily charts. A bearish engulfing candle closed just above the 50-day eMA, but a break beneath 83.00 takes it to fresh lows an bring the 82.50 target into focus (just above the 82.00/30 lows.

- The Canadian dollar was favoured over its commodity FX peers, AUD and NZD, after the BOC’s hawkish meeting on Wednesday, but mostly flat elsewhere.

Learn how to trade forex

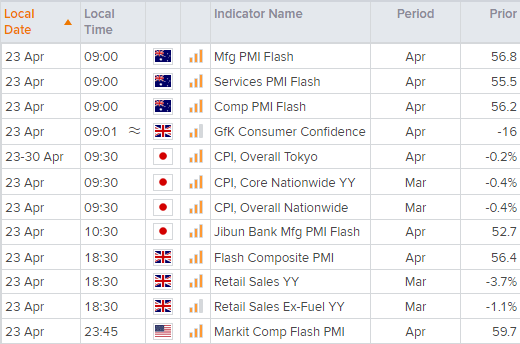

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM