Asian Futures:

- Australia's ASX 200 futures are up 35 points (0.47%), the cash market is currently estimated to open at 7,495.90

- Japan's Nikkei 225 futures are up 230 points (0.85%), the cash market is currently estimated to open at 27,243.25

- Hong Kong's Hang Seng futures are up 206 points (0.83%), the cash market is currently estimated to open at 25,055.72

UK and Europe:

- UK's FTSE 100 index rose 29.04 points (0.41%) to close at 7,087.90

- Europe's Euro STOXX 50 index rose 22.79 points (0.55%) to close at 4,147.50

- Germany's DAX index rose 42.23 points (0.27%) to close at 15,808.04

- France's CAC 40 index rose 20.22 points (0.31%) to close at 6,626.11

Friday US Close:

- The Dow Jones Industrial rose 225.98 points (0.65%) to close at 35,120.08

- The S&P 500 index rose 35.87 points (0.82%) to close at 4,441.67

- The Nasdaq 100 index rose 158.633 points (1.06%) to close at 15,092.57

Learn how to trade indices

Indices:

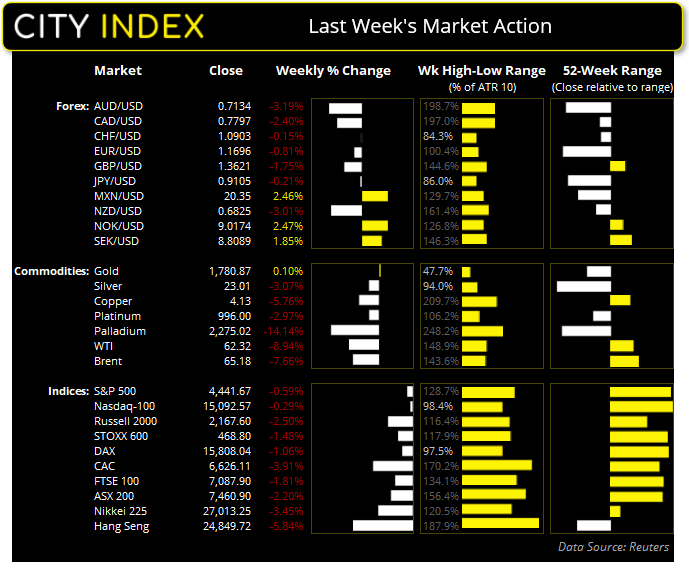

It was a weak close for indices overall last week, yet prices recovered on Friday with small caps leading the minor rebound. The Russell 2000 rose 1.65% on Friday (with growth stocks outperforming) whilst the Nasdaq 100 managed a 1.06% gain compared to the S&P 500’s 0.81% rise. For the week the Russel 2000 was down -2.6%, the Dow Jones fell -1.1%, the S&P 500 fell -0.6% (both printed bearish outside weeks) although the Nasdaq was up 0.9%.

The ASX 200 printed a bearish engulfing candle during its worst week of trade since January, falling -2.2%. It held above Thursday’s low but wasn’t exactly the bullish bounce we were hoping for on Friday. That said, a potential inverted pinbar has formed which shows bearish momentum is waning and is confirmed with a break above Friday’s high.

ASX 200 Market Internals:

ASX 200: 7460.9 (-0.05%), 22 August 2021

- Utilities (1.49%) was the strongest sector and Materials (-1%) was the weakest

- 7 out of the 11 sectors closed higher

- 8 out of the 11 sectors outperformed the index

- 83 (41.50%) stocks advanced, 110 (55.00%) stocks declined

- 66.5% of stocks closed above their 200-day average

- 56% of stocks closed above their 50-day average

- 57.5% of stocks closed above their 20-day average

Outperformers:

- + 15.66% - Redbubble Ltd (RBL.AX)

- + 5.6% - Treasury Wine Estates Ltd (TWE.AX)

- + 4.6% - Inghams Group Ltd (ING.AX)

Underperformers:

- -7.43% - Cochlear Ltd (COH.AX)

- -6.91% - Lynas Rare Earths Ltd (LYC.AX)

- -5.66% - Orocobre Ltd (ORE.AX)

Forex: Is risk-off getting too risky?

It was another crushing week for commodity currencies, with AUD and NZD leading the declines at -3.1% and -2.95% respectively. RBA remain as dovish as they could possibly be, whilst the Delta variant breakout in New Zealand has weighed on the Kiwi dollar despite RBNZ being the most hawkish central bank in town.

The Japanese yen was the second strongest currency last week, and only slightly behind the US dollar. It was higher against all major peers (except the USD), yet moves now appear stretched. That is not to suggest place bets against the yen, but bears should trade with caution.

Taking AUD/JPY as an example, there are technical reasons to suspect it is oversold. It has fallen for 7 consecutive days for the firt time since October, the RSI (2) sits at an extremely oversold level of 0.6 and Friday formed a Doji. Oh, an indices closed higher on Friday so if we see Asian share markets track Wall Street higher then it could help support the battered AUD/JPY.

The US dollar index (DXY) closed above the March high for two consecutive days, yet closed on Friday with a bearish hammer just above this key level. If the dollar turns lower we’d expect many of last week’s moves to also unwind, so we’ll keep a close eye for a break below 93.43 as it could signal a change in sentiment for market.

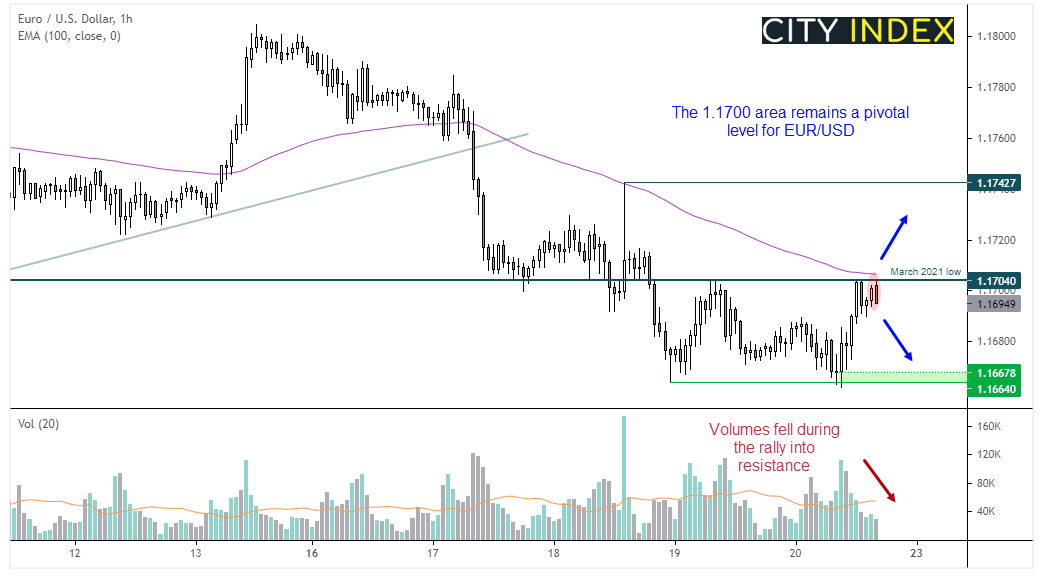

The March 2021 low at 1.1704 is the clear line in the sand on EUR/USD. Prices rebounded to this level on Friday yet stalled at this key resistance level (just below its 100-bar eMA) and a bearish engulfing candle has formed on the hourly chart to show traders are clearly paying attention to it. As long as the 1.17 area continues to cap as resistance then it may tempt bears to try and drive price lower and should a weak dollar story develop it could be the early stages of trend continuation. Yet a break above the 1.17 area signals a deeper retracement and should coincide with a break back below the march high on DXY.

Learn how to trade forex

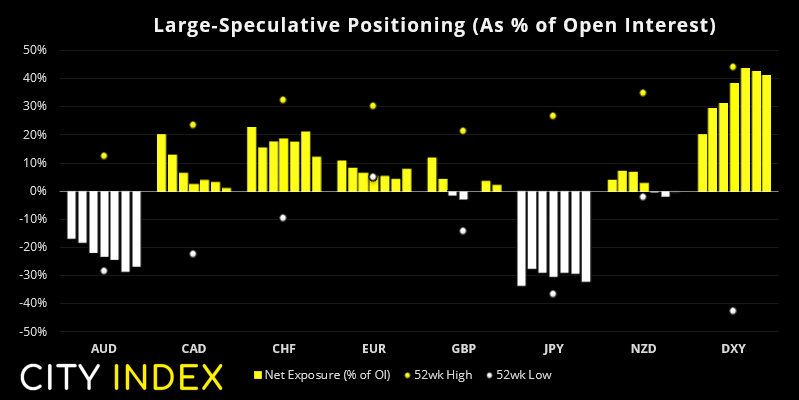

From the Weekly COT Report (Commitment of Traders)

From Tuesday 17th August 2021:

- Net-long exposure to the US dollar fell by US -$2.2 billion last week to $0.8 billion according to calculations from IMM. They are net-short the dollar against emerging market by -$0.79 billion and net-long against G10 by $1.08 billion.

- Traders were their most bearish on AUD futures since March 2020. Yet it sits at -2.9 standard deviations over the past year, so we could be reaching a sentient extreme. Still, the move has mostly been fuelled by a rapid increase in short positions as opposed to longs closing out, so now is probably not the time to stand in front of a bearish freight train.

- Traders were their least bullish on silver futures since June 2023.

- Net-long exposure for copper fell for a 3rd week to 20.08k contracts, due to short bets rising for 3 weeks and longs being trimmed for the past two.

Worst week for commodities in 16-months

The rise of Delta and the US dollar saw commodities trade were broadly lower last week, with the CRB commodity basket falling -4.6% during its most bearish week since April 2020. It’s holding above its 20-week eMA (for now), although all eyes will be on Jackson Hole this week to see how the dollar responds after Jerome Powell’s speech.

WTI fell -9.2% to a 3-month low and is trading lower during early Asian trade. Brent was slightly spared with a -7% loss and now trades around 65.0.

Given the potential reversal signal on the DXY, and gold’s ability to withstand dollar weakness over the past week, we suspect gold could pop higher should the dollar finally retrace. It continues to trade in a potential bull flag formation, and 1800 – 1805 remain interim targets. A break above here would be a clear victory for bulls.

Palladium fell -14.1% last week during its worst week since March 2020. Whilst this points to oversold by some metrics there are no obvious signs of a price low in just yet.

Up Next (Times in AEST)>

Flash PMI date (purchase managers index) is released across major regions today and provides an early peak at growth potential. For stronger market reactions for currency markets we’d like to see divergences form among the regions.

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM