Asian Futures:

- Australia's ASX 200 futures are down -3 points (-0.04%), the cash market is currently estimated to open at 7,267.20

- Japan's Nikkei 225 futures are down -10 points (-0.03%), the cash market is currently estimated to open at 28,850.80

- Hong Kong's Hang Seng futures are down -32 points (-0.11%), the cash market is currently estimated to open at 28,710.63

UK and Europe:

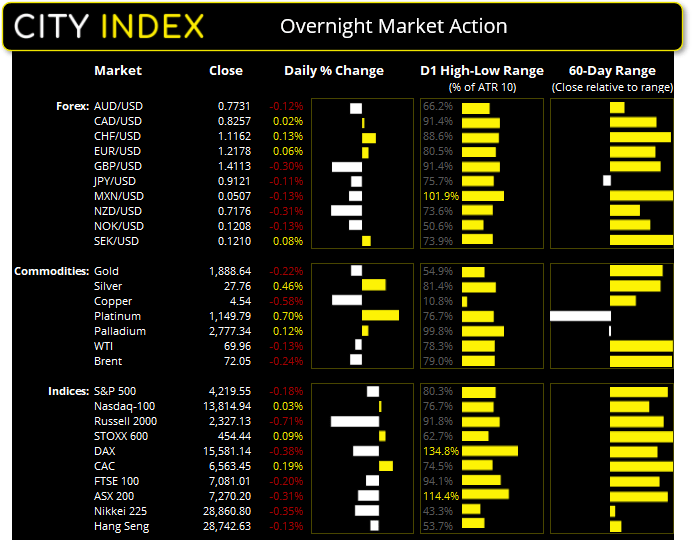

- UK's FTSE 100 index fell -14.08 points (-0.2%) to close at 7,081.01

- Europe's Euro STOXX 50 index rose 0.84 points (0.02%) to close at 4,096.85

- Germany's DAX index fell -59.46 points (-0.38%) to close at 15,581.14

- France's CAC 40 index rose 12.44 points (0.19%) to close at 6,563.45

Wednesday US Close:

- The Dow Jones Industrial fell -152.68 points (-0.44%) to close at 34,447.14

- The S&P 500 index fell -7.71 points (-0.19%) to close at 4,219.55

- The Nasdaq 100 index rose 4.079 points (0.03%) to close at 13,814.94

Learn how to trade indices

Another range-bound session on Wall Street:

The Biden Administration is to donate 500 million doses of Pfizer covid vaccine globally. Two hundred million are earmarked for this year with the remaining 300 million to be allocate for the first half of next year. The deal is expected to be announced at the G7 mean later today in the UK. The MSCI’s all-country index closed just 3 points from its record high and bond yields softened as traders covered some of their heavily-short exposure to underlying bond prices.

Wall Street teased its record high yet, once again, failed to hold into earlier gains during a wait-and-see session ahead of today’s CPI report. The Dow Jones was -0.44% lower and the S&P was down -0.18%, with healthcare and utility stocks supporting the index, whilst financial and industrial stocks ultimately led it lower. The Russell 2000 closed -0.7% lower yet remains the strongest performer over recent weeks, having risen 10.79% over the past 18 sessions and now trades just off its record high.

A large bearish hammer formed on the ASX 200 by its close yesterday which strongly hints at a interim top. Whilst futures markets currently point to a relatively flat open our bias is bearish given yesterday’s key reversal day, but we’d prefer to see a break beneath 7267.60 to confirm.

- R3: 7311 (Yesterday’s value area high)

- R2: 7300 (Round number)

- R1: 7285 (POC)

- S1: 7267/71 (prior two day’s lows)

- S2: 7244 – 7251 (June 4th low and lower value area)

ASX 200 Market Internals:

ASX 200: 7270.2 (-0.31%), 09 June 2021

- Utilities (0.37%) was the strongest sector and Consumer Staples (-1.44%) was the weakest

- 5 out of the 11 sectors closed higher

- 8 out of the 11 sectors outperformed the index

- 68 (34.00%) stocks advanced, 118 (59.00%) stocks declined

- 14 hit a new 52-week high, 0 hit a new 52-week low

- 74.5% of stocks closed above their 200-day average

- 69% of stocks closed above their 50-day average

- 77.5% of stocks closed above their 20-day average

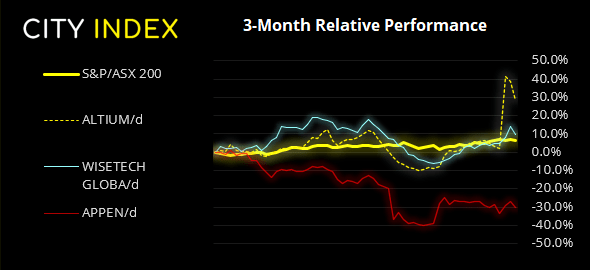

Outperformers:

- + 11.3% - Brickworks Ltd (BKW.AX)

- + 7.77% - Unibail-Rodamco-Westfield SE (URW.AX)

- + 5.18% - Whitehaven Coal Ltd (WHC.AX)

Underperformers:

- -7.50% - Altium Ltd (ALU.AX)

- -4.04% - WiseTech Global Ltd (WTC.AX)

- -3.90% - Appen Ltd (APX.AX)

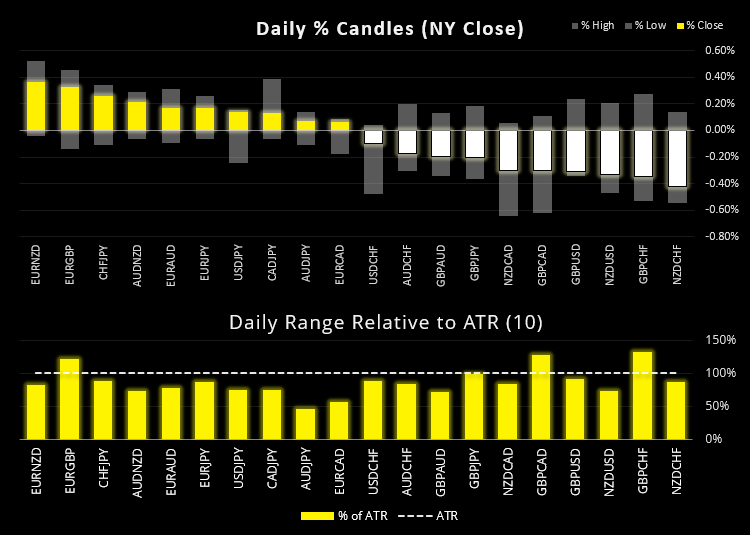

Forex: GBP gets lightly ‘battered’ over sausages

The British pound was lower as the EU’s VP threatened quotas and tariffs on the UK imports on a wide range of goods including (heavens forbid) sausages. GBP/JPY gave back earlier gains and -0.2% invalidating an earlier bullish breakout. GBP/CAD once again turned lower at 1.7170 resistance to close -0.3% and GBP/USD fell -0.25%.

The Bank of Canada (BOC) kept policy unchanged although expectations are for them to taper in July. This should remain a supportive feature for the Canadian dollar as we head into H2, especially if lockdown restrictions are eased further as their vaccination program is rolled out. CAD/CHF is teasing the May low as part of a weekly reversal pattern we have mentioned previously, although CAD is managing to remain firm against its other peers.

Elsewhere, CHF/JPY rose to a seven-day high and is fast approaching our initial target at the May high. EUR/JPY rose to a three-day high ahead of today’s ECB meeting where no change is expected and they’re likely to avoid ‘talking taper’ or mentioning the exchange rate. There’s potential for a swing low at 132.90 to keep an eye on.

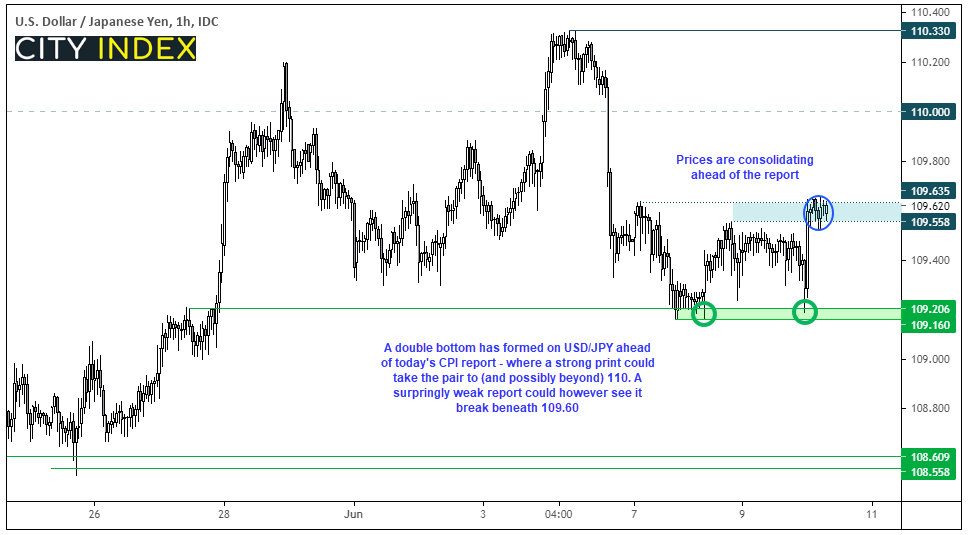

USD/JPY has printed a double bottom pattern on the hourly chart ahead of today’s CPI report from the US. With two swing lows around 109.16-20, traders now have a clear support zone to keep in focus should we see a large move on the dollar. A strong report could strengthen the greenback and send USD/JPY closed to 110, or simply take the buck to new cycle lows (with a break beneath 109.16 being a key levels for bears to monitor).

Learn how to trade forex

Commodities:

Platinum futures are trying to turn lower after falling to a three-day low, suggesting a lower high has formed at 1179.0, so a break beneath 1140 assumes bearish trend continuation.

Gold and silver are hanging around recent prices as they await the outcome of today’s CPI report. Silver tested 28.0 resistance and gold closed back below 1900 for a fifth session.

A Rikshaw Man Doji formed on WTI futures daily chart and fractionally below 70.0 to suggest a pause in trend is underway. Although it could also be caught I the crosswinds of inflation data and the strength of the US dollar upon its release, so directionally could go either way by the end of the week.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 10:40 PM

Yesterday 04:00 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM