Asian Futures:

- Australia's ASX 200 futures are down -17 points (-0.25%), the cash market is currently estimated to open at 6,743.70

- Australia's ASX 200 futures are down -50 points (-0.17%), the cash market is currently estimated to open at 28,880.11

- Australia's ASX 200 futures are down -340 points (-1.17%), the cash market is currently estimated to open at 28,896.79

UK and Europe:

- The UK's FTSE 100 futures are down -47 points (-0.71%)

- Euro STOXX 50 futures are down -35 points (-0.94%)

- Germany's DAX futures are down -96 points (-0.68%)

Thursday US Close:

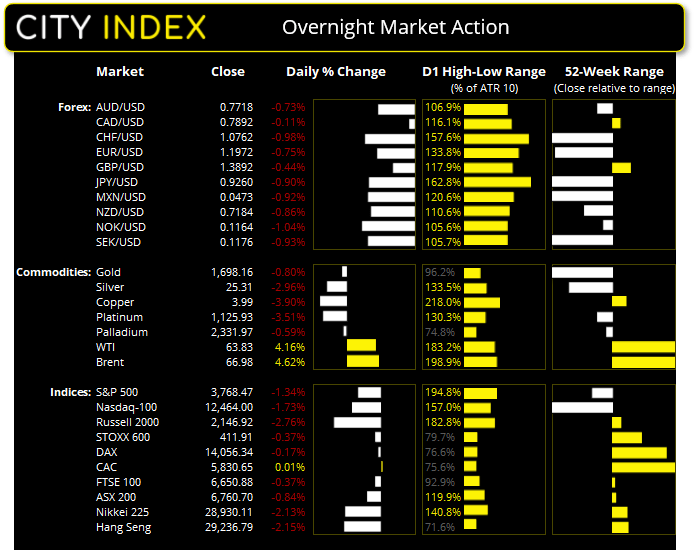

- The Dow Jones Industrial fell 345.95 points (-0.0111%) to close at 30,924.14

- The S&P 500 index fell -51.25 points (-1.35%) to close at 3,768.47

- The Nasdaq 100 index fell -219.325 points (-1.73%) to close at 12,464.00

The inverted correlation between stock market indices and yields continued. Bond traders offloaded their bets to push yields higher, sending the US 10-year rose to 1.54% and the 30-year to 2.31%. Both are sat just below last week’s 1-year highs and the trend suggests they’ll break above them in due course. We therefore expect Australian yields to follow suit today and retest RBA’s patience and their 1% target of the 3-year yield (which currently trades around 1.5%).

Equity markets were broadly lower, although it was small caps which led declines in Wall Street with the Russell 2000 falling -2.8%, whilst the tech savvy Nasdaq 100 falling a further -2.7% and the S&P 500 shed -1.3%. Moreover, the S&P 500 e-mini futures closed beneath its bullish trendline from the November low (watch this space).

S&P 500: 04 March 2021

- The index closed -4.61% below its 52-week high

- 77.03% of stocks closed above their 200-day average

- 69.5% of stocks closed above their 200-day average

- 40.99% of stocks closed above their 200-day average

Powell: Fed to remain patient

Despite bond traders challenging the Fed’s patient approach of easy policies with an inflationary overshoot, Jerome Powell stuck to his guns and vowed to keep rates low until the economy rebounds, warning it could still be “substantial time” before they act. Even if rates were to rise this spring, expect patience from the Fed, as they want to see wages broadly higher across all ethnic groups along with low unemployment and job gains. So, we can expect easy policies from the Fed until the economy is “very far along the road to recovery”.

Dollar dominates as bears get squeezed

The US dollar index (DXY) rallied to a 3-month high overnight amid its second most bullish session. With speculators short the dollar at levels not seen since 2011, a squeeze was bound to happen at some point. Clues of a dollar turnaround have been left in recent weeks but evidence of it is now seeping through more obviously into price action.

The Swiss franc was the weakest major which saw USD/CHF blow through 0.9200 and (momentarily) rise to its highest level since July 2018. USD/JPY moved from 107 to 108 with apparent ease during its most bullish session in four months.

The Canadian dollar was also firm due to higher oil prices following the OPEC+ meeting. USD/MXN saw a daily close above 21.00 in line with our bias from yesterday’s Asian Open report. Higher levels of volatility saw several USD, CHF and JPY pairs exceed their daily ATR’s (average true ranges) so a key question for Asian traders is whether we’ll see an extension of those move, and how much room there is left for them to continue (for example, we probably won’t see trend continuation of a similar magnitude to overnight trade).

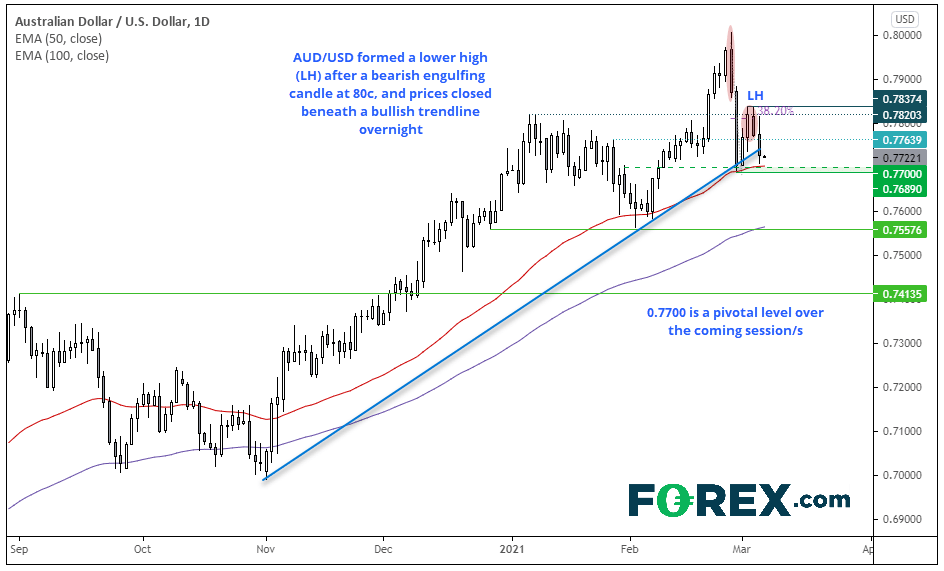

AUD/USD: Have we seen the turning point?

The Australian dollar is slowly leaving a trail of clues that it may have topped. A bearish engulfing candle on the daily charts at 80c was the first, and we have now seen a lower high and a close beneath its November bullish trendline.

It has found support at its 50-day eMA, although a break beneath 0.7700 would also see it break the average.

- A break below 0.7700 brings the 0.7557 low into focus

- If USD retraces in Asia it should leave room for a minor bounce from current levels (and be of interest to bullish day traders), and raise the potential for a ‘false break’ of the trendline

- A break back above the 0.7820 high will see us revert to a bullish bias on the daily chart

Crude oil rallies on OPEC+ surprise

Oil prices rose sharply overnight as OPEC+ wrongfooted investors by leaving oil output unchanged. As Joe Perry points out, this came as quite the surprise as the broad consensus was for OPEC+ to raise output between 1.2 – 1.5 million barrels a day to control the combination of higher prices, higher demand and lower supply.

WTI rallied over 7% at one stage and broke a long-term bearish trendline from the July 2008, record high. Currently trading around 64, the daily structure remains bullish above the 59.24 swing low. Brent rallied to 67.70 and stopped just shy of breaking a new cycle high. Both oil markets have risen around 85% from their October lows and both appear primed to continue their trends from here.

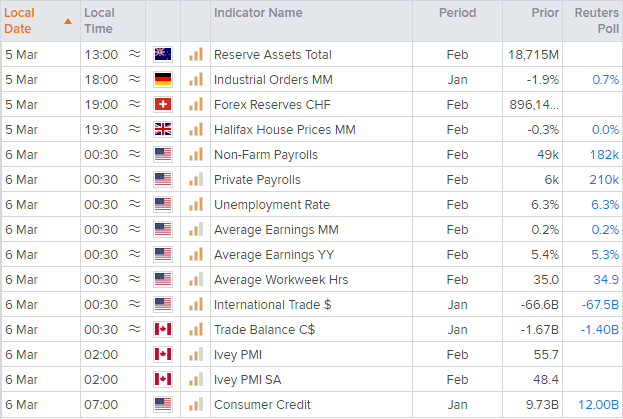

Up Next (Times in AEDT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- We expect yields (and their reaction to them rising to remain a dominant theme today. And it would be interesting to see if RBA step in again either today or next week to take the sting out of the 3-year yield trading above 1%.

- Nonfarm payroll is today’s main calendar event. View Matt Weller’s preview for a complete rundown: NFP preview: When will jobs growth get back into gear?

Latest market news

Today 07:55 AM

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Yesterday 08:00 PM

Latest Indices articles

Yesterday 08:00 PM

Yesterday 04:54 PM

April 15, 2024 06:08 AM

April 14, 2024 04:00 AM