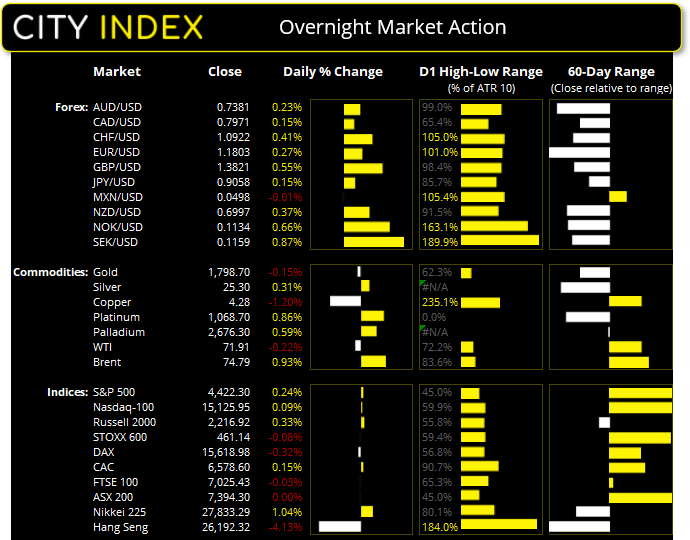

Asian Futures:

- Australia's ASX 200 futures are down -7 points (-0.1%), the cash market is currently estimated to open at 7,387.30

- Japan's Nikkei 225 futures are up 120 points (0.43%), the cash market is currently estimated to open at 27,953.29

- Hong Kong's Hang Seng futures are down 1 points (0%), the cash market is currently estimated to open at 26,193.32

UK and Europe:

- UK's FTSE 100 index fell -2.15 points (-0.03%) to close at 7,025.43

- Europe's Euro STOXX 50 index fell -6.51 points (-0.16%) to close at 4,102.59

- Germany's DAX index fell -50.31 points (-0.32%) to close at 15,618.98

- France's CAC 40 index rose 9.78 points (0.15%) to close at 6,578.60

Monday US Close:

- The Dow Jones Industrial rose 82.76 points (0.24%) to close at 35,144.31

- The S&P 500 index rose 10.51 points (0.24%) to close at 4,422.30

- The Nasdaq 100 index rose 14.16 points (0.09%) to close at 15,125.95

Learn how to trade indices

Indices:

Doubts are rising that Biden’s $1.2 trillion infrastructure bill will get over the line quickly. Whilst there were hopes that the Senate Majority Leader Chuck Schumer could start the floor debate as soon as Monday, Democrats and Senates argued over the weekend making a bipartisan vote this week much less likely. But with a long history of competing parties not agreeing on much in general then this is of little surprise. And that was apparent on US indices which etched out minor gains.

The Dow Jones and S&P 500 led gains by rising 0.24% and the Nasdaq rose 0.09%, all closing at record highs. 7 of the 11 S&P 500 sectors rose, led by energy and materials. Small caps were the stronger performers with the S&P SC600 rising 1.3% and Russell 2000 up 0.89%.

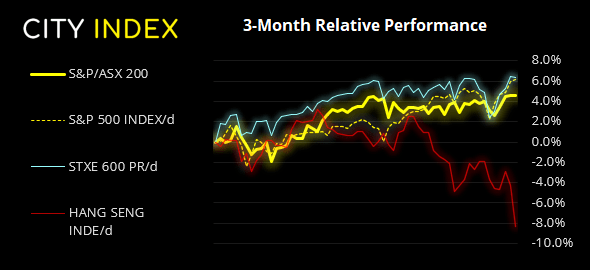

The ASX 200 saw an intraday record high yet closed flat, back below the breakout level to close the day with a small bearish pinbar. Given the strong momentum leading up to yesterday’s candle then we still favour a break higher although yesterday’s reversal candle does leave the potential for a pause in trend or dip back within its 1-month range.

The Hang Seng index closed below its 200-week eMA yesterday after finding resistance at its 200-day eMA last week. Next major support sits around 25,850 – 26,000.

ASX 200 Market Internals:

ASX 200: 7394.30 -0.1 (0.00%), 26 July 2021

- 67.5% of stocks closed above their 200-day average

- 56.5% of stocks closed above their 50-day average

- 55% of stocks closed above their 20-day average

Forex:

The US dollar index (DXY) fell -0.2% ahead of tomorrow’s FOMC meeting to a two-day low. Whilst there’s no expectation of any policy change (or indication of there being one any time soon) we suspect volatility across dollar pairs may remain on the low side leading into the event. That said, DXY did probe the lower trendline of its bullish channel so a break beneath 92.50 (yesterday’s low) would warn of a countertrend move on the daily chart.

The British pound was the strongest major currency overnight, rising 0.6% against the greenback and 0.4% against the Japanese yen. Covid cases had fallen for five-consecutive days in the UK for the first time since February which saw selling pressure for GBP crosses abate.

AUD/USD dipped below 0.7350 overnight yet later recovered on the bac of the weaker dollar to form either a bullish hammer, or hanging man candle. A break either side of yesterday’s range will confirm which reversal candle it may be but, if it breaks higher, take note of resistance around 0.7400 (round number and September 2020 high).

Learn how to trade forex

Commodities: CRB index break to four-year high

The Thomson Reuters CRB commodities index rose to its highest level since July 2015 and above its 200-week eMA yesterday, taking its rise from the April 2020 low to +116%. We’d noted last week how it have recovered back above its 50-day eMA and the last time that had occurred was in March, which marked the beginning of its next leg higher. And whilst history is kind of repeating, bullish momentum is stronger on this occasion.

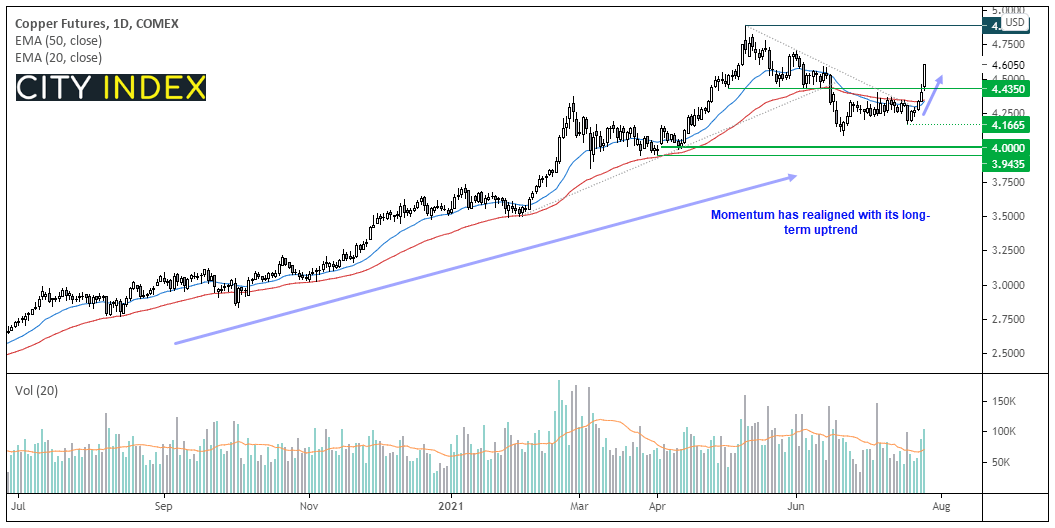

We also discussed the potential for copper to outperform precious metals in yesterday’s video and, so far, it has not disappointed. The combination of a weaker US dollar, better-than-expected earnings and floods in China saw copper futures rally over 4% to a six-week high with rising (and above average) volumes. The 4.888 May high is now in focus for bulls although the bias is for an eventual break above it due to the strong trend, even if prices pause for breath or retrace around those highs first. Ideally it can now hold above yesterday’s low or turn 4.435 resistance into support, if it can’t break directly higher form here.

Silver continues to find resistance at its 200-day eMA, with the highs of the past three days all respecting it almost to the point. Whilst this shows the potential for the swing high to have formed already our bias remains bearish below 25.75 / broken trendline.

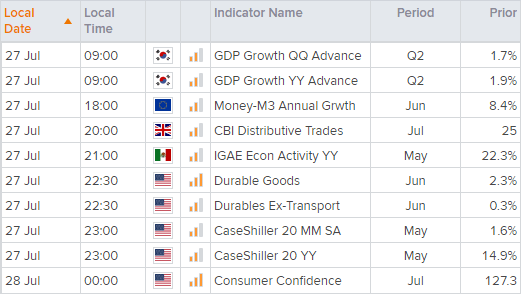

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 01:15 PM

Today 07:49 AM

Today 04:24 AM

Latest Indices articles

Yesterday 06:08 AM

April 14, 2024 04:00 AM

April 12, 2024 05:46 PM

April 11, 2024 05:15 PM