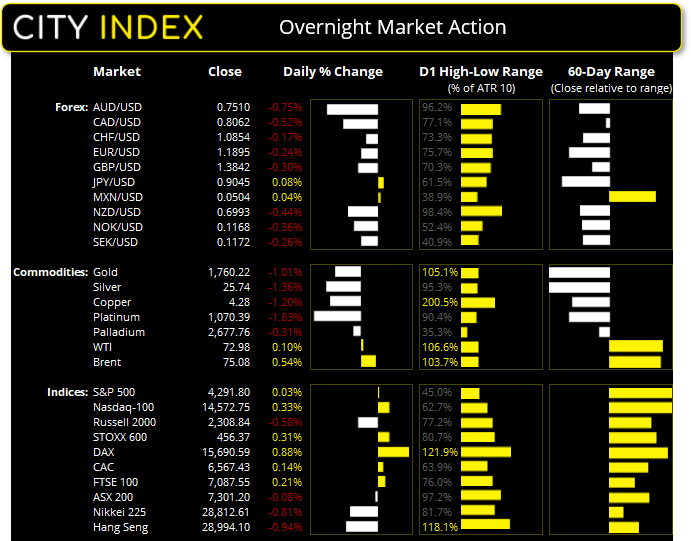

Asian Futures:

- Australia's ASX 200 futures are up 16 points (0.22%), the cash market is currently estimated to open at 7,317.20

- Japan's Nikkei 225 futures are up 100 points (0.35%), the cash market is currently estimated to open at 28,912.61

- Hong Kong's Hang Seng futures are up 59 points (0.2%), the cash market is currently estimated to open at 29,053.10

UK and Europe:

- UK's FTSE 100 index rose 14.58 points (0.21%) to close at 7,087.55

- Europe's Euro STOXX 50 index rose 17.6 points (0.43%) to close at 4,107.51

- Germany's DAX index rose 136.41 points (0.88%) to close at 15,690.59

- France's CAC 40 index rose 9.41 points (0.14%) to close at 6,567.43

Tuesday US Close:

- The Dow Jones Industrial rose 9.02 points (0.03%) to close at 34,292.29

- The S&P 500 index rose 1.19 points (0.03%) to close at 4,291.80

- The Nasdaq 100 index rose 47.769 points (0.33%) to close at 14,572.75

Learn how to trade indices

Indices: New highs for Wall Street

US consumer confidence rose to a 16-month high in June according to the Conference Board, as survey respondents showed an appetite for motor vehicles and household appliances, underlining strength in the economic recovery. Furthermore, consumer’s outlook on whether jobs are ‘plentiful’ over ‘hard to get’ rose to its highest differential since 2000, which could bode well for Friday’s NFP report if that indeed turns out to be the current situation.

The Nasdaq 100 and S&P 500 extended their record highs, with the S&P 500 extending its record for a fourth consecutive session. Yet volatility was low overall with the S&P and Dow Jones rising just 0.3% and the Nasdaq rose 0.33%.

In Europe equities had a positive start yet failed to hold onto early gains to close effectively flat. The FTSE 100 and CAC printed bearish hammers inside Monday’s bearish ranges, so we are still on guard for a bearish break on the FTSE of Monday’s low.

The ASX 200 threw a spanner in the works of the symmetrical triangle discussed yesterday, by teasing bears with a downside break yet recovering later in the session to close flat with a bullish pinbar. Considering this is as 10 million Australian’s went into lockdown then it’s not a bad close at all. As it stands, we would still consider longs with a break above Friday’s high to suggest momentum had realigned with its bullish trend.

ASX 200 Market Internals:

ASX 200: 7301.2 (-0.08%), 28 June 2021

- Information Technology (0.65%) was the strongest sector and Materials (-0.68%) was the weakest

- 8 out of the 11 sectors closed higher

- 78 (39.20%) stocks advanced, 111 (55.78%) stocks declined

- 8 hit a new 52-week high, 2 hit a new 52-week low

- 71.36% of stocks closed above their 200-day average

- 64.32% of stocks closed above their 50-day average

- 47.24% of stocks closed above their 20-day average

Outperformers:

- + 5.69% - Metcash Ltd (MTS.AX)

- + 4.96% - Nuix Ltd (NXL.AX)

- + 3.47% - Lynas Rare Earths Ltd (LYC.AX)

Underperformers:

- -5.67% - Collins Foods Ltd (CKF.AX)

- -5.18% - Unibail-Rodamco-Westfield SE (URW.AX)

- -4.6% - Nufarm Ltd (NUF.AX)

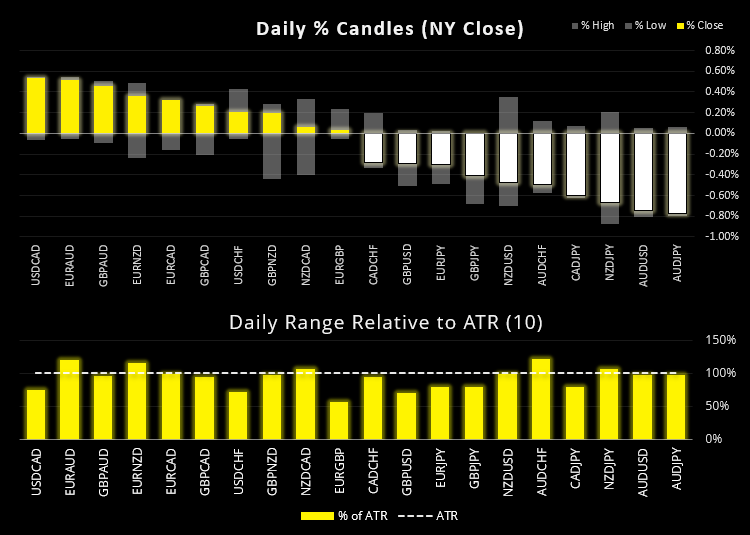

Forex: Delta outbreaks weighs on commodity FX

The latest coronavirus outbreak saw the USD and JPY rise on safe-haven flows and weigh on commodity currencies (AUD, CAD and NZD). Commodity currencies were the weakest majors overnight and the weakest month-to-date.

The Japanese yen was the strongest major as the risk-off sentiment apparent in yesterday’s Asian session spilled over to the European and US ones. The yen was up against all its major peers but made the most ground against the Australian dollar as several states have headed back into lockdown and the Delta variant rose across parts of Asia. AUD/JPY was the biggest mover, shedding -0.8% in line with our bearish bias and its ranges topping near its 10-day ATR and hitting the initial target of 0.8300. Its next support level is 82.76. Strong economic sentiment for Europe lifted EUR/AUD to our near-term bullish target at its 200-day eMA.

The US dollar index (DXY) moved higher in line with its double bottom breakout, rose to a six-day high and made it around ¾ of its way to the double bottom target at 92.30. USD/CHF stopped just shy of our June high target and GBP/USD came just 14 pips from our initial 1.3800 target. AUD/USD and NZD/USD both closed firmly beneath their 200-day eMA’s after printing prominent highs.

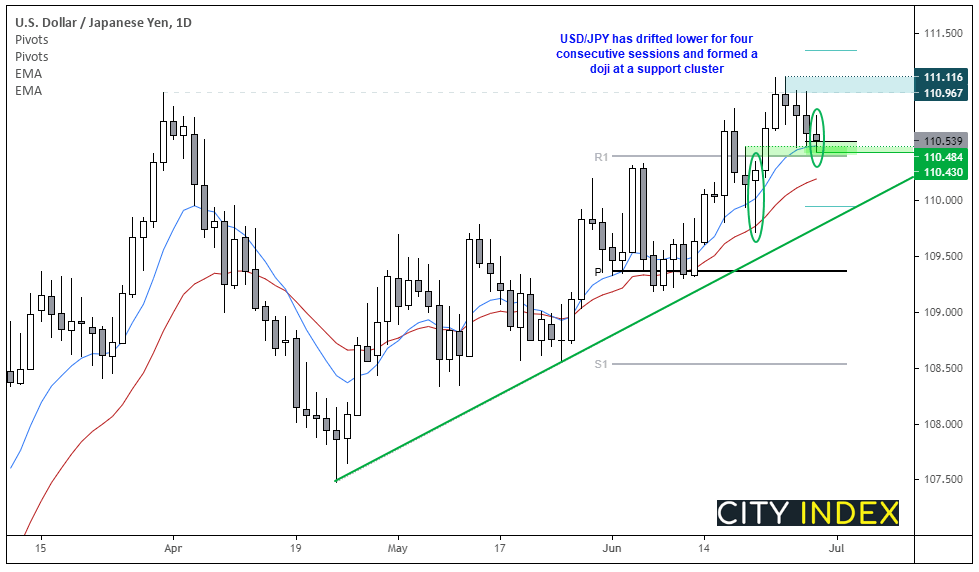

USD/JPY was just -0.1% lower by the close but intraday price action suggests the move to be corrective. Its trend remains bullish overall, and prices are accelerating away from trendline support to show a pickup of momentum. Prices have also retraced for four consecutive days since last week’s high. Moreover, prices have formed a Doji and respected a cluster of support including the monthly R1 and pivot and weekly pivot point and 20-day eMA. Therefore, if prices can break above yesterday’s high without breaking the support zone then bulls could assume momentum is trying to realign with its bullish trend.

Learn how to trade forex

Commodities: Metals feel the weight of a stronger dollar

Gold and silver finally woke up from their small but choppy sideways ranges with downside breaks. Gold fell -1% and broke to a 10-week low before rising back above 1756 support to close around 1760. Silver fell -1.26% and probed the 25.56 low before closing at 25.73.

Platinum futures fell -3% and accelerated further away from its 200-day eMA after printing a two-bar bearish reversal at the technical milestone on Monday.

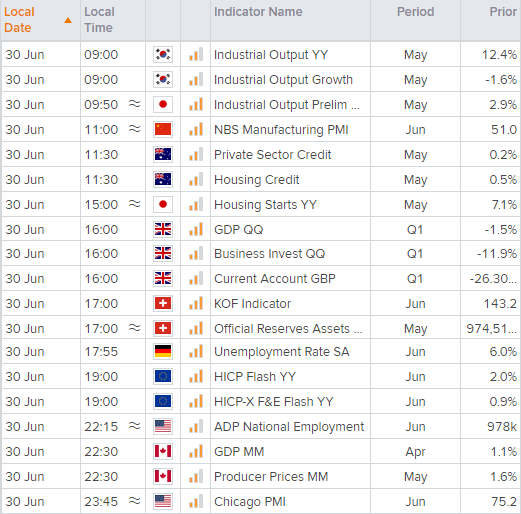

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Latest Forex articles

Yesterday 11:09 PM

Yesterday 04:00 PM

Yesterday 04:19 AM

April 22, 2024 04:33 PM