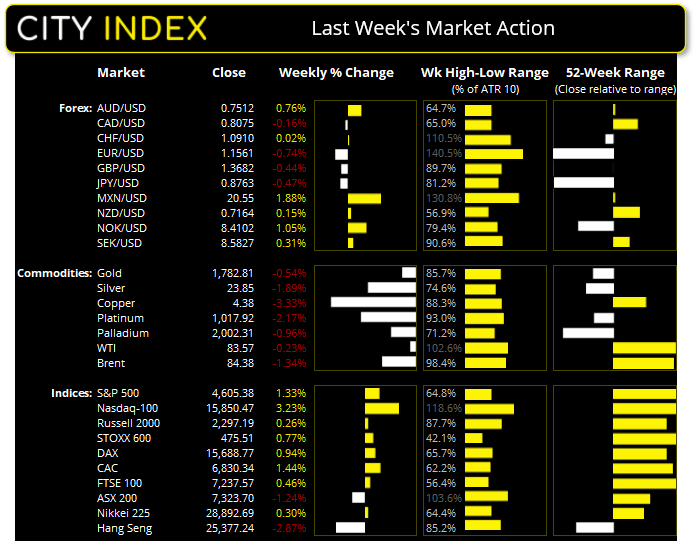

Australia’s ASX 200 index closed at 7,323.70 on Friday

- Japan's Nikkei 225 index closed at 28,892.69 on Friday

- Hong Kong's Hang Seng index closed at 25,377.24 on Friday

- China'sA50 Index closed at 15,882.05 on Friday

European Friday close:

- UK's FTSE 100 index fell -11.9 points (-0.16%) to close at 7237.57

- Europe's Euro STOXX 50 index rose 16.69 points (0.39%) to close at 4250.56

- Germany's DAX index fell -7.56 points (-0.05%) to close at 15688.77

- France's CAC 40 index rose 26.12 points (0.38%) to close at 6830.34

US Friday close:

- The Dow Jones rose 89.06 points (0.25%) to close at 35,819.56

- The S&P 500 rose 8.96 points (0.2%) to close at 4,605.38

- The Nasdaq 100 rose 72.31 points (0.46%) to close at 15,850.47

Indices:

The Nasdaq 100 closed to a record high on Friday, despite concerns over rising inflation. US consumer spending rose 0.6% and personal consumption expenditures rose 0.2% in September, further fanning concerns of persistent inflation. Combined with weak GDP print of 2% y/y it shows stagflation remains in play.

Concerns that inflation in Australia is to rip higher like it is elsewhere across the globe toppled the ASX 200 on Friday, falling -1.4% during its worst session since October 1st. Handing back earlier gains the index closed effectively flat in October, although it printed a bearish engulfing week and closed on its 200-week eMA. The final hour of trade printed a bullish hammer on high volume so there’s potential for a bounce, although we’d look for any signs of weakness below the 7368 – 7380 zone.

The China A50 produced a bearish inside week after finding resistance at last week’s high. 15,600 is the next level for bulls to defend. The Hang Seng fell for a fourth consecutive session. The daily trend remains bullish above 24,870 and we’re waiting for evidence of a corrective low to form. Weak manufacturing data over the weekend could weigh further on these indices, especially if Caixin PMI read at 12:45 tracks lower.

Japan’s conservative party remained in power at Sunday’s election, although Prime Minister Fumio Kishida has lost some authority as the opposition took some seats away from him. The LDC (Liberal Democratic Party) and its smaller coalition partner (Komeito) have so far won 274 seats of the 261 required for a majority, although it is down from 305 seats previously. Futures markets are yet to open, but the Nikkei 225 closed at 28,892 and rose 0.3% last week.

ASX 200 Market Internals:

ASX 200: 7323.7 (-1.44%), 31 October 2021

- Healthcare (-0.1%) was the strongest sector and Real Estate (-2.52%) was the weakest

- 11 out of the 11 sectors closed lower

- 5 out of the 11 sectors outperformed the index

- 33 (16.50%) stocks advanced, 160 (80.00%) stocks declined

- 64% of stocks closed above their 200-day average

- 51.5% of stocks closed above their 50-day average

- 43.5% of stocks closed above their 20-day average

Outperformers:

- + 6.92%-GUD Holdings Ltd(GUD.AX)

- + 5.63%-Reece Ltd(REH.AX)

- + 4.25%-JB Hi-Fi Ltd(JBH.AX)

Underperformers:

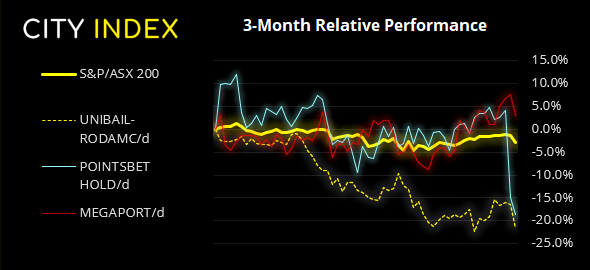

- -6.23%-Unibail-Rodamco-Westfield SE(URW.AX)

- -4.4%-Pointsbet Holdings Ltd(PBH.AX)

- -4.22%-Megaport Ltd(MP1.AX)

Forex:

The US dollar was the strongest major on Friday which saw the US dollar index (DXY) print a bullish engulfing candle during its most bullish session in over 4-months. Conversely, EUR/USD fell to a 2-week low and appears a 3-wave correction is now complete. The weekly chart posted a bearish outside week and closed below the 200-week eMA.

The Australian dollar rose for a fourth week and briefly touched a 16-week high, although dollar strength saw it hand back some gains on Friday. Whilst the trend remains bullish on the daily chart momentum is waning, so we see the potential for a pullback.

USD/JPY continues to consolidate just off its 3-year highs and above its 20-day eMA. We’re looking for an eventual bullish breakout and for prices to hold above 113.00.

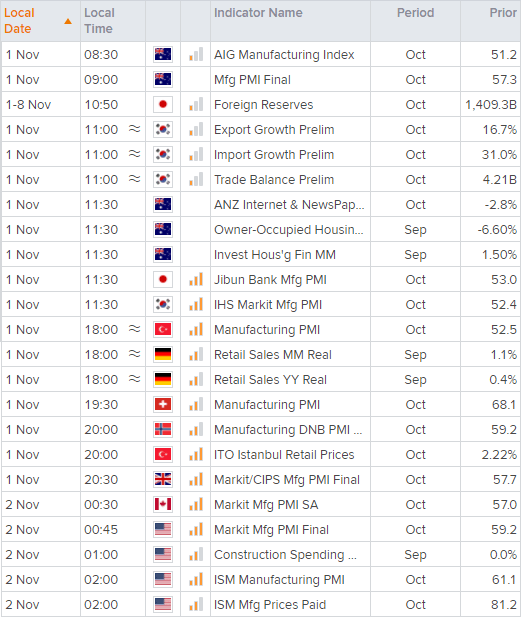

Final PMI for Australian manufacturing and services PMI are released at 08:30 and 09:00 respectively, then at 11:30 ANZ job adverts and home loans data is released. South Korean trade data is scheduled for 11:00 and is seen as a proxy for global demand, then we have final PMI’s for South Korea and Japan at 11:30. We’ll also be keeping an eye on China’s manufacturing PMI at 12:45 given the NBS read fell to 49.2 over the weekend, down from 49.6.

Learn how to trade forex

Commodities:

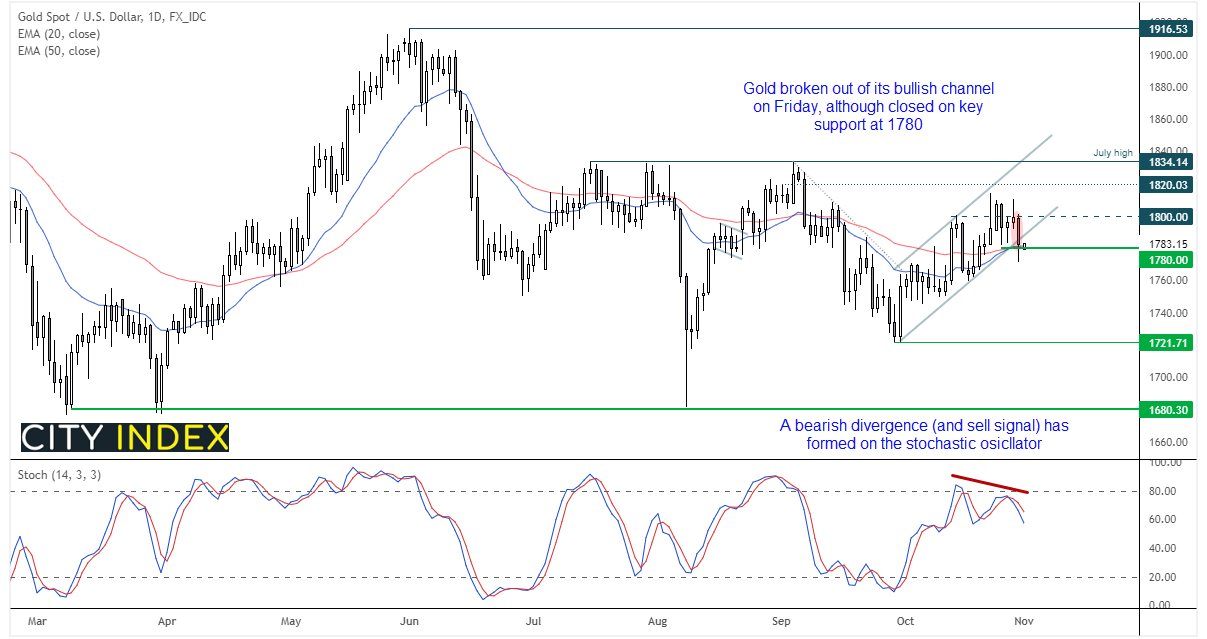

The strong dollar weighed on metals and helped bears to break gold’s bullish channel. Despite its best attempts, it only managed to close above 1800 one day last week before printing a bearish hammer on Thursday and bearish engulfing candle on Friday.

Furthermore, a bearish divergence and sell signal has formed on the stochastic oscillator. Whilst the trend channel has been penetrated, support has been found around 1780 where the 20 and 50-day eMA’s reside, so there is potential for a minor bounce from current levels. Ultimately we remain bearish below 1800 and now seeking a break of Friday’s low as part of its next bearish move.

Oil prices held above $80 last week with WTI printing a bullish hammer at the 20-day eMA followed by a second hammer (and up day) on Friday. The daily trend remains bullish and $85 is the next key level for bulls top conquer to extend this trend.

Up Next (Times in AEST)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Trade Ideas articles

Yesterday 03:00 PM

Yesterday 11:14 AM

April 24, 2024 11:00 AM