Asian Futures:

- Australia’s ASX 200 futures are flat, the cash market is currently estimated to open at 7308

- Japan's Nikkei 225 futures are down -50 points (-0.17%), the cash market is currently estimated to open at 29016.18

- Hong Kong's Hang Seng futures are up 41 points (0.14%), the cash market is currently estimated to open at 29329.22

European Friday close:

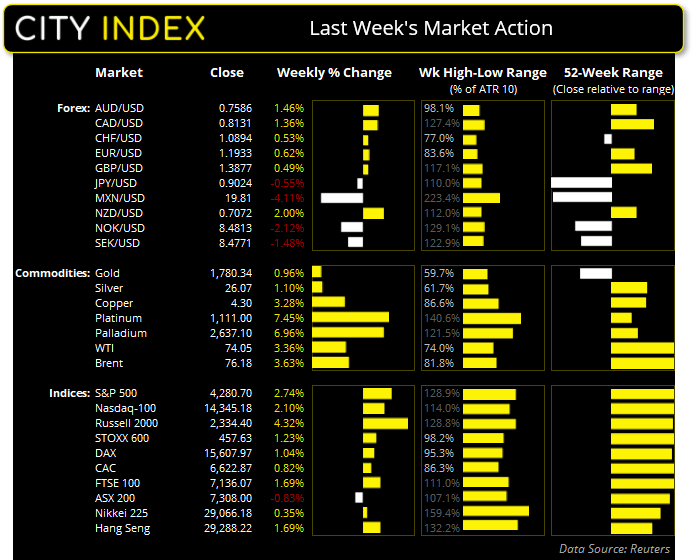

- UK's FTSE 100 index rose 26.1 points (0.37%) to close at 7136.07

- Europe's Euro STOXX 50 index fell -1.77 points (-0.04%) to close at 4120.66

- Germany's DAX index rose 18.74 points (0.12%) to close at 15607.97

- France's CAC 40 index fell -8.28 points (-0.13%) to close at 6622.87

US Friday close:

- The Dow Jones rose 237.04 points (0.36%) to close at 34,433.84

- The S&P 500 rose 14.21 points (0.34%) to close at 4,280.70

- The Nasdaq 100 fell -20.777 points (-0.14%) to close at 14,345.18

Learn how to trade indices

Global stocks close to a record high

US consumer sentiment rose in June according to the Michigan survey’s final read, although it was revised down slightly from the preliminary report. Inflation expectations also rose with the 1-year forward look now at 4.2% (up from 4% previously), whilst the 5-year remained flat at 2.8%.

Core PCE inflation rose to 3.4% YoY from 3.1% previously, although slightly below 3.5% expected. This is unlikely to deter the Fed from sticking to their transitory guns regarding inflation, but the fact the dollar did not sell-off also suggests the jury is still out on that one.

Global equities closed to a record high on Friday according to MSCI’s World Price index. The Nasdaq Biotech and Bank index were again top performers, rising around 0.78% on the day and up 2.8% and 5.8% respectively last week. The Nasdaq closed a touch lower by -0.14% after hitting a record high on Thursday which warned of over-extension with a bearish pinbar which failed to hold above its upper Keltner band. A bearish divergence has also formed on its RSI (2), so perhaps the Nasdaq may take another dip lower. The S&P 500 closed to a record high and rose 2.75% last week, with all but the technology sector rising on Friday with the financial and utilities sector leading the way higher.

The ASX 200 remained above its 20-day eMA on Friday and moved higher form the open but only created a marginal new high above 7300. If it can break above Friday’s high today, we would be keen to explore any bullish patterns upon a retracement to 7322 or 7311.50.

ASX 200 Market Internals:

ASX 200: 7308 (0.45%), 25 June 2021

- Materials (1%) was the strongest sector and Consumer Staples (-0.93%) was the weakest

- 8 out of the 11 sectors closed higher

- 5 out of the 11 sectors outperformed the index

- 148 (74.37%) stocks advanced, 44 (22.11%) stocks declined

- 74.87% of stocks closed above their 200-day average

- 74.87% of stocks closed above their 50-day average

- 64.32% of stocks closed above their 20-day average

Outperformers:

- + 6.38% - Boral Ltd (BLD.AX)

- + 6.09% - Kogan.com Ltd (KGN.AX)

- + 4.88% - Adbri Ltd (ABC.AX)

Underperformers:

- -3.91% - Nuix Ltd (NXL.AX)

- -3.88% - Pilbara Minerals Ltd (PLS.AX)

- -3.06% - Zip Co Ltd (Z1P.AX)

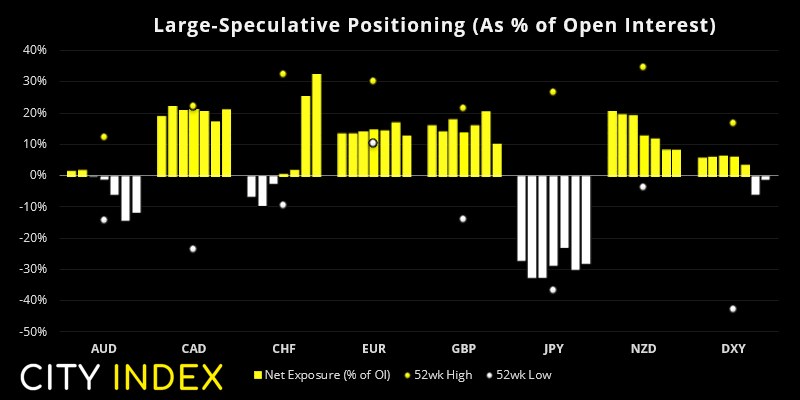

From the Weekly COT Report (Commitment of Traders)

From Tuesday 22nd July 2021:

- Short exposure to the US dollar was reduced by -$4.5 billion, according to data compiled by IMM

- Large speculators flipped to net-short exposure on US 10-year treasuries

- Net-long exposure to euro futures fell by 29.1k contracts

- Net-long exposure to the Swiss franc is at its highest level in three months

- Traders were their least bullish on gold futures two years

- Net-short exposure to yen futures fell to a -week low

- Long exposure to copper futures continued to fall, and is now at its lowest level since reverting to net-long exposure in in June 2020

Gross long exposure (75% and above):

- S&P 500 futures: 84.4%

- WTI futures: 82.3%

Commodities: Soybean bulls make a meal of it

The US oil rig count rose for a 10th consecutive month, as rising prices are supported by firm fundamentals. Oil prices rose to their highest level since October 2018, seeing WTI futures hit $74 and brent futures hit $76.16. Brent formed a bullish engulfing candle on the four-hour chart to show support is confirmed at 74.95. OPEC meet on Thursday and expectations are production increase in production.

Gold remains in a corrective phase and produced another bearish hammer which failed to retest 1800. With Core PCE roughly in line with expectations it has calmed fears that the Fed may taper sooner. So, one may have expected a firmer close for gold, yet here we are. We remain bearish below 1800 and favour selling into minor rallies, for an eventual break below 1756.

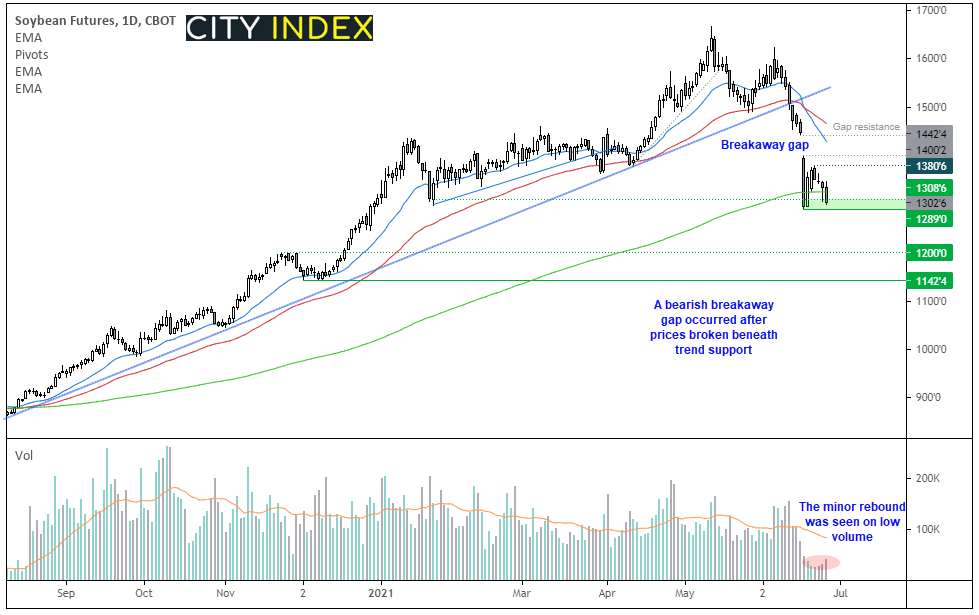

Lumber futures fell to a 5-month low and all but erased this year’s 173% rally. A break below 775 brings the lows around 600 into focus. Bearish lumber prices certainly plays into the hands of ‘transitory’ inflation, as would soybean futures breaking below 1289 support.

We can see on the daily chart that prices broke beneath trendline support in the middle of June then produced a bearish breakaway gap. Whilst prices have tried to form a base above 1289, the minor rebound was seen on low volumes and momentum has turned lower once more so we are now looking for a break to new lows, given the strength of bearish momentum leading into recent lows. A break beneath 1289 brings the highs around 1200 into focus and then the 1124.4 low.

Forex: DXY rests below its 200-day eMA

The US dollar index (DXY) remained under its 50-week eMA for a second week and prices are now resting beneath its 200-day eMA. And, after all the hype, the dollar failed to make a decisive move on Friday after Core PCE came in slightly under expectations at 3.4%. Closing the day with a bullish pinbar, DXY’s closing has been effectively flat since Wednesday despite its intraday ups and downs. That said we favour an upside break as its recent move lower appears corrective.

Incidentally, we didn’t get the breakout from compression on USD/CHF but it continues to favour an upside break, given the shallow retracement on the daily chart against a bullish impulsive move, and now a bullish pinbar on Friday. We are now looking for a break (or hourly close) above trend resistance to suggest its uptrend is ready to resume.

AUD/USD and NZD/USD appear to be other majors that are near to completing their retracements. Both pairs rose each day last week as part of a countertrend move but printed bearish pinbars on Friday. We suspect upside from here may be limited. Our bias for AUD remains bearish below 0.7650 (which allows plenty of wriggle room for the upside) but this will be lowered if bearish momentum returns.

Learn how to trade forex

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM