Asian futures:

- Australia’s ASX 200 futures are currently up 29 points (0.48%), the cash market is currently estimated to open at 6,702.3

- Japan’s Nikkei 225 futures are currently up 100 points (0.34%), the cash market is currently estimated to open at 29,066.01

- Hong Kong’s Heng Seng futures are currently up 13 points (0.04%), the cash market is currently estimated to open at 28,993.21

FTSE 100 Friday close:

Europe’s Friday close:

- The Euro STOXX 50 index fell -48.84 points (-1.33%)

- France’s CAC 40 index fell -93.04 points (-0.67%)

- Germany’s DAX index fell -80.67 points (-1.4%)

Friday US close:

- The Dow Jones index fell -469.64 points (-0.15%) to close at 30,932.37

- S&P 500 index fell -18.19 points (-0.48%) to close at 3,811.15

- Nasdaq 100 index fell -473.88 points (-3.56%) to close at 12,909.443

The US dollar was the strongest major during a risk-off week, allowing the US dollar index close to a 6-day high. Commodity currencies such as AUD and NZD were hit hard over Thursday and Friday, EUR/USD appears to be headed for 1.2000 again and USD/JPY closed above 106 to print a bullish outside candle on Friday.

The stronger dollar saw commodities trade broadly lower, and the Thomson Reuters CRB commodity index fell -2.2% from its 3-year high amid its most bearish session in 5-months. Copper led metals lower with a -4% decline, palladium and platinum fell -3.5% and -2.3% respectively, silver was down -2.85% and gold broke below key support (in line with Friday’s bias) to close at 1,733. WTI (-3.2%) and Brent (-1.2%) remain structurally bullish on their daily charts yet suffered their most bearish sessions since early November. Gold broke below key support in line with our bearish bias in Friday’s European open report and currently trades around 1,733.

The US 10-year is back below 1.5% to close at 1.45% and the 3-year yield fell to 2.18% after printing a 1-year high on Thursday of 2.42%. Given the TNX/S&P 500 ratio fell 3% then the move could be attributed to pension funds buying bonds alongside month-end rebalancing.

Asian indices were the worst hit on Friday with the Nikkei 5 falling nearly 4%, the Hang Seng was -3.6% lower and the ASX 200 fell to a 1-month low. Yet US indices seemed to get off lightly. The Nasdaq 100 held above 12,755 support and posted a minor gain of 0.6%, the S&P 500 held above its 50-day eMA with a minor loss of -0.5% and the Russell 2000 remains flat at 2200. The Dow Jones industrial average got off less lightly closing -1.5% lower and breaking convincingly below 31,272 support.

Democratic House passes Biden’s COVID-19 relief plan

Biden’s relief package has passed another milestone, even if it was highly unlikely to be blocked by the Democrat-majority House. Voting down party lines, the bill won majority support of 219- 212. Individuals can now expect $1400 to arrive as a one-off payment with a $400 employment benefit due to run until the 29th of August. The bill is expected to be signed into law before current unemployment benefits package is due to expire in mid-March.

Yet Republicans retain their view that much of this support is not necessary, and there are also concerns from within the investment community that this $1.9 trillion package could result in unwanted inflation. Now to be passed over to the Senate and Vice President Kamilla Harris may have to perform another tie-breaking vote (obviously, in favour of the bill).

FDA Approve Johnson and Johnson’s one-shot vaccine

Further positive news in the fight against the pandemic has arrived, as the FDA formally approved Johnson and Johnson’s vaccine. Now the third available in the US, 20 million doses already produced and 100 million expected by May, this one-shot vaccine alone could treat nearly one third of the US population. And as it does not require two shots like other currently available vaccines, it could help speed up the process and the economic recovery.

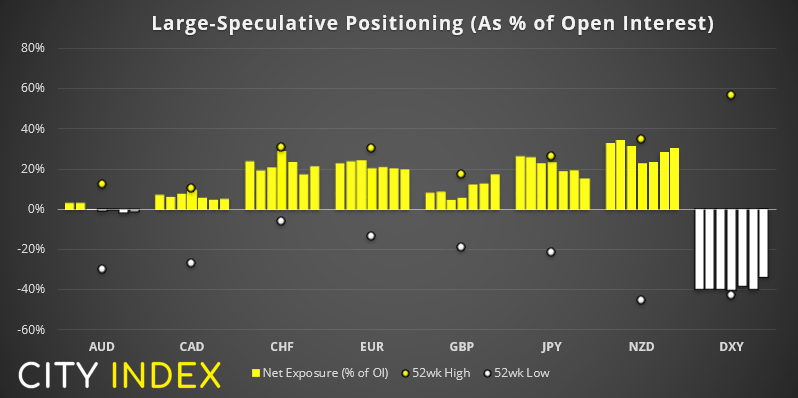

Weekly Commitment of Traders Report

Read our guide on how to interpret the weekly COT report

As of Tuesday 23rd February 2021:

- Repositioning last week was fairly-light with all FX majors seeing a weekly change below 10,000 contracts.

- Large speculators reduced their net-long JPY futures exposure by -5.5%.

- Traders increased their net-long exposure to the Swiss franc futures by 10%, and British pound futures by 8.4%.

- Gold futures traders reduced their net-long exposure by -19.2k contracts, fuelled predominantly with a closure of log positions.

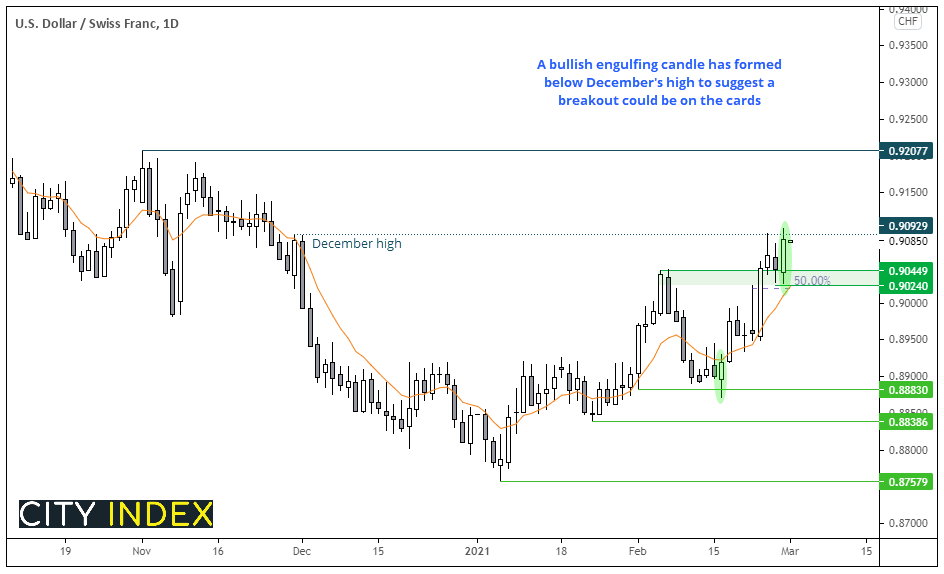

USD/CHF: Eyeing a break of the December high

USD/CHF has produced a 3-month bullish reversal pattern called a morning star reversal. Prices closed to a 3-month high and produced a bullish engulfing candle on Friday. Given the series of higher lows on the daily chart and Friday’s bullish close we are now waiting for a break above Friday’s high to assume bullish continuation.

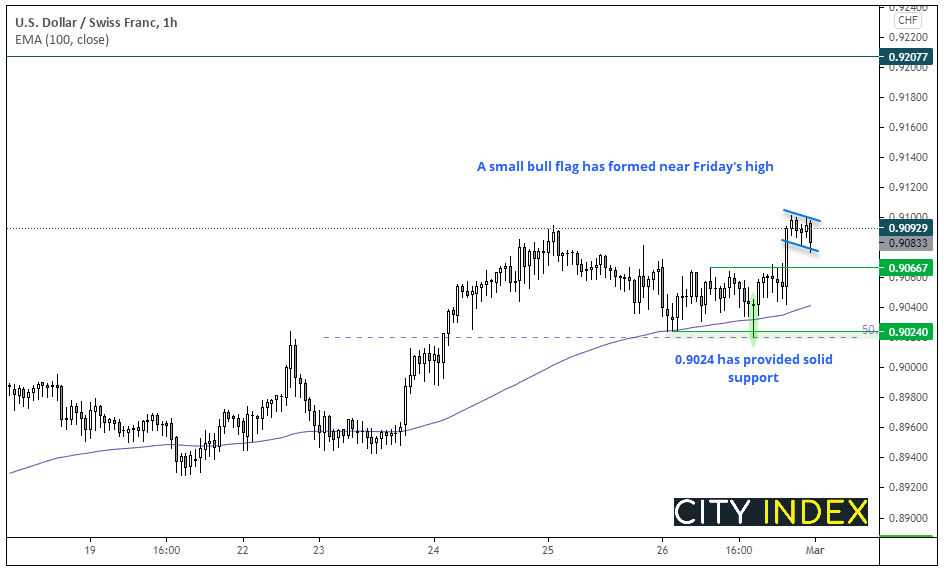

Switching to the hourly chart shows a small bull flag has formed around Friday’s high. Assuming prices do not trade much lower at the weekly open then we’d be on high alert for a breakout above 0.9100. Also note that a bullish pinbar marks support around 0.9024 which also coincide with a 50% retracement level.

- A break above Friday’s high confirms the bullish breakout. If prices drift lower we’d be looking for 0.9067 to hold as support

- Next major resistance is around 0.9100

- The 0.9067 and 0.9024 support levels can be used to aid risk management

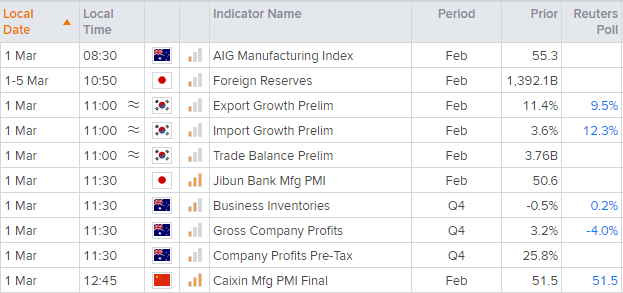

Up Next (Times in AEDT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Today’s trade balance data for South Korea can be used as a proxy for global demand. Exports are expected to have risen by +9.5% in February whilst imports are forecast to have risen by +12.3%. A positive report could help provide some support under Asian indices.

Flash PMI data is released across Asia, Europe and US today (US also includes ISM manufacturing). As for Asia, manufacturing PMI for Australia, Japan and China are main calendar events. If we are to see all rise in tandem (along with positive exports for South Korea) then we run the chance of a mild risk-on session ahead of the Europe open. Asian indices (Nikkei, Hang Seng, ASX 200) along with AUD and JPY should be of interest to news traders.

Latest market news

Latest Forex articles

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM