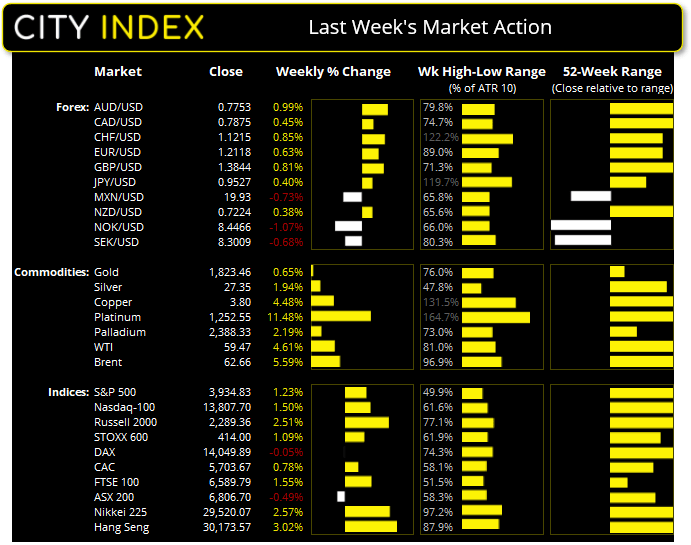

Bears returned to keep USD under pressure last week ahead of the 3-day weekend in the US. The US dollar index (DXY) fell further away from its 20-week eMA and closed beneath its 10-week eMA to create a two-week bearish reversal pattern. USD/CNH closed to its lowest level since June 2018 and all majors took advantage of the dollar’s doldrums.

Whilst we expect the dollar to remain under pressure this week, Monday could be off to a slow start as both the US and China have public holidays which means key markets across Asia and North America will be closed. Yet in the Asian session we have an important GDP print from Japan which could impact BOJ's (Bank of Japan's) monetary policy decision in March, as reports surfaced they may use the meeting to signal tweaks in their policy. A weak GDP print will all but confirm this expectation.

The Australian dollar was the strongest performer last week and closed to a 2-week high. Bullish momentum saw prices accelerate away from its 10-week eMA and now looks set to re-test the 0.7820 high. However, keep in mind the 200-month eMA resides at 0.7877 and the psychological level of 0.8000 sits just 150 pips above Friday’s close.

The British pound was also a strong performer and closed near its 33-month high. A bullish engulfing candle formed on Friday and used its 10-day eMA as a springboard, therefore a break above last week’s high assumes bullish continuation.

Commodities also took advantage of the weaker dollar with most most major commodities closing higher. Although it was platinum which stole the show with an impressive 11.5% rally during its most bullish week since March. Closing at its highest level in 6-years, the next major resistance is around 1300, a level we now expect to break after an initial period of consolidation or a minor retracement.

Indices were broadly higher with the exception of the ASX 200 and DAX. 6894 resistance continues to cap gains on the ASX, and a break beneath 6800 assumes a deeper correction. The DAX is trying to build support above 13,800 and a break above 14,170 assumes bullish continuation. The Russell 2000 led US indices higher to show small-caps continue to appreciate the Biden Administration’s stimulus measures.

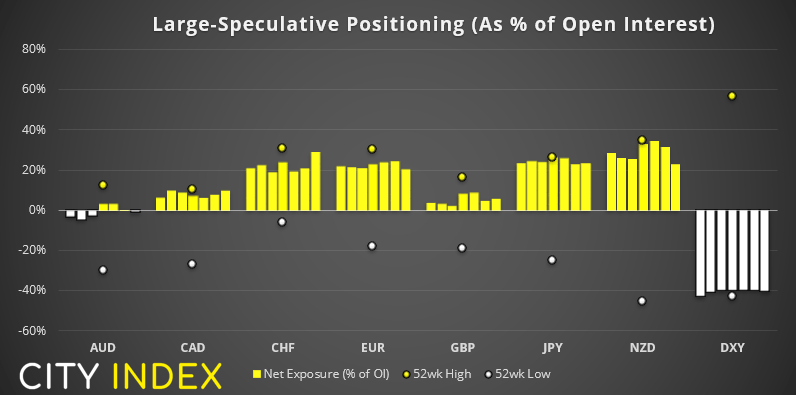

Large Speculative Positioning

- Traders flipped to net-short exposure on Russell 2,000 futures. At a net-short exposure of -8.4k contracts, it’s the most bearish positioning since May. Whilst it is plausible traders are hedging their long equities exposure through Russell 2000 futures, their net-short exposure could suggest traders are erring on the side of caution with the index at record highs.

- Bullish bets increased to an 11-month high on the British pound after the BOE (Bank of England) effectively ruled out negative interest rates. Net-long exposure increased by 11.5k contracts (+£720 million, or 11.5%).

- Net-long exposure to CAD futures was reduced by -6.6k contracts (-$656 million, or -3.3%), its largest weekly decline in 7-months.

- Traders reduced long exposure to JPY futures by -10k contracts.

- Gross long exposure on copper futures rose to their highest level since January 2018.

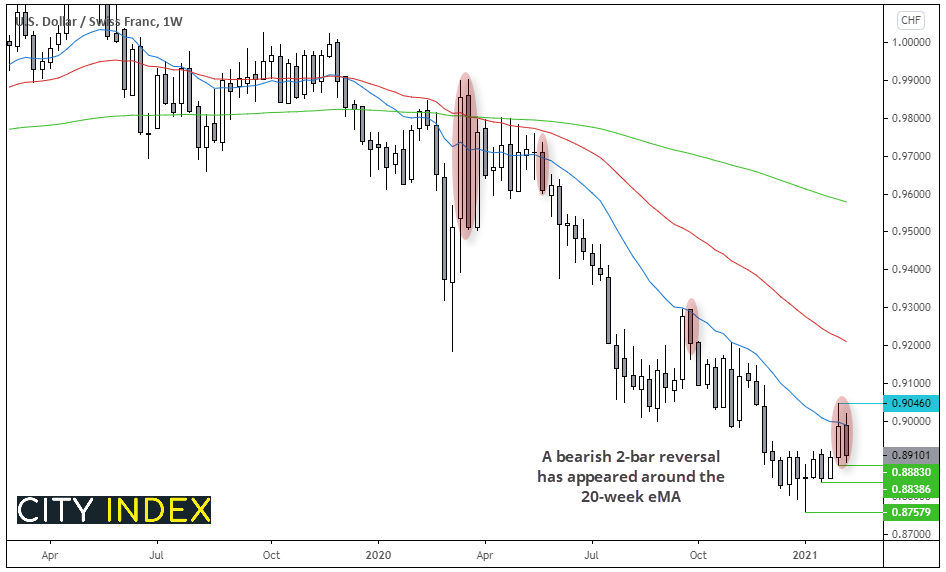

USD/CHF: Potential Swing Trade Short

The weekly chart has respected resistance at the 20-week eMA and produced a 2-bar bearish reversal (dark cloud cover). Should prices break beneath 0.8890 (the prior week’s low) then we can assume momentum has realigned with the dominant bearish trend.

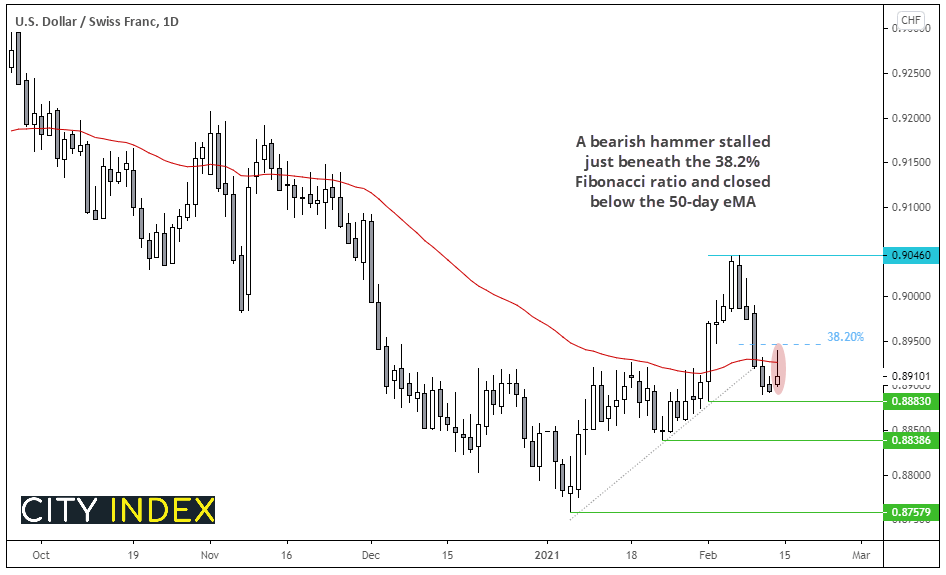

The daily chart also produced a bearish reversal pattern. Last week we outlined our case for a lower USD/CHF, although we needed to wait for a minor bounce higher. That appears to have materialised with a bearish hammer stopping just shy of the 38.2% Fibonacci ratio. The bearish reversal candle also closed back beneath the 50-day eMA and prices have remained beneath the broken retracement line.

- A break beneath 0.8830 invalidates the low two weeks ago and assumes bearish continuation

- The initial target is 0.8838 and then 0.8760 (just above a major swing low)

- The bias remains bearish below 0.8950

Up Next (Time in Sydney GMT +11)

- It’s a bank holiday in the US on Monday (President’s day) so US markets will be closed, which likely means lower trading volumes overall and smaller trading ranges.

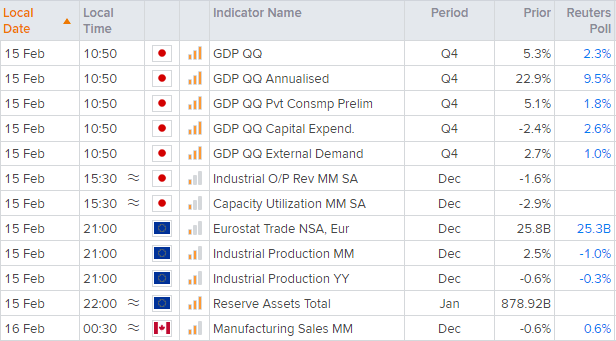

- Q4 GDP (growth domestic product) for Japan kicks the calendar off at 10:50 today and is the main event. Given rumours are surfacing that BOJ (Bank of Japan) may look to ease in their March policy meeting, it makes today's GDP print all the more important. A weak could translate to weaker yen (and firmer USD/JPY) as traders price in further easing from BOJ.

- European industrial production is more ‘mid-tier’ data, but something that could provide a volatile reaction for the Euro STOXX 600 index, should the report deviate too much from expectations.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM