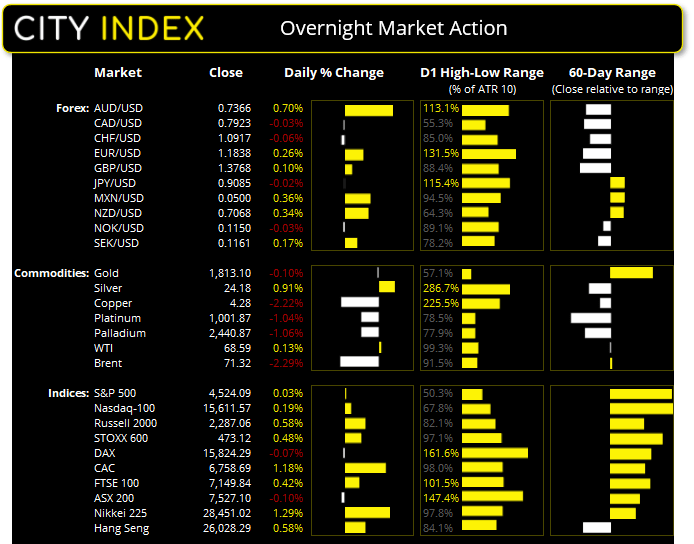

Asian Futures:

- Australia's ASX 200 futures are down -14 points (-0.19%), the cash market is currently estimated to open at 7,513.10

- Japan's Nikkei 225 futures are up 60 points (0.21%), the cash market is currently estimated to open at 28,511.02

- Hong Kong's Hang Seng futures are up 193 points (0.74%), the cash market is currently estimated to open at 26,221.29

UK and Europe:

- UK's FTSE 100 index rose 30.14 points (0.42%) to close at 7,149.84

- Europe's Euro STOXX 50 index rose 30.86 points (0.74%) to close at 4,227.27

- Germany's DAX index fell -10.8 points (-0.07%) to close at 15,824.29

- France's CAC 40 index rose 78.51 points (1.18%) to close at 6,758.69

Wednesday US Close:

- The Dow Jones Industrial fell -48.2 points (-0.14%) to close at 35,312.53

- The S&P 500 index rose 1.41 points (0.04%) to close at 4,524.09

- The Nasdaq 100 index rose 29.053 points (0.19%) to close at 15,611.57

Learn how to trade indices

US indices hand back early gains

Markets were expecting ADP employment to print around 640k jobs, so the 48k delivered was underwhelming to say the least. Anything above 556k would have erased the prior two-months losses but it was not to be. Should tomorrow’s nonfarm payroll report also drop the ball then it could push back expectations for the fed to announce tapering at their meeting later this month. Yet whilst this scenario is bullish for stocks it also likely acts as a headwind due to it undermining the economic recovery somewhat.

ISM manufacturing rose to 59.9 (a 2-month high), and new orders hit a 3-month high of 66.7. Prices paid fell to an 8-month low to show a further easing of inflationary pressures whilst the employment index contracted at its fastest rate since November at 49.0. It is by no means a bad report overall yet the employment index raises another red flag ahead of NFP tomorrow.

Wall Street gapped higher at the open and extended the rally to new high before handing back earlier gains, to close beneath the open yet above yesterday’s close. This saw the Nasdaq rise 0.19% by the close and the S&P 500 squeeze a 0.03% gain. Tech stocks remained favourites in the dovish-Fed environment with Apple (AAPL) pushing to new highs.

ASX 200 Market Internals:

ASX 200: 7527.1 (-0.10%), 01 September 2021

- Financials (0.86%) was the strongest sector and Consumer Staples (-1.54%) was the weakest

- 5 out of the 11 sectors closed higher

- 99 (49.50%) stocks advanced, 95 (47.50%) stocks declined

- 70.5% of stocks closed above their 200-day average

- 66.5% of stocks closed above their 50-day average

- 62% of stocks closed above their 20-day average

Outperformers:

- + 5.51% - Nuix Ltd (NXL.AX)

- + 4.49% - Alumina Ltd (AWC.AX)

- + 4.16% - IDP Education Ltd (IEL.AX)

Underperformers:

- -6.66% - Blackmores Ltd (BKL.AX)

- -5.71% - Mesoblast Ltd (MSB.AX)

- -5.38% - Polynovo Ltd (PNV.AX)

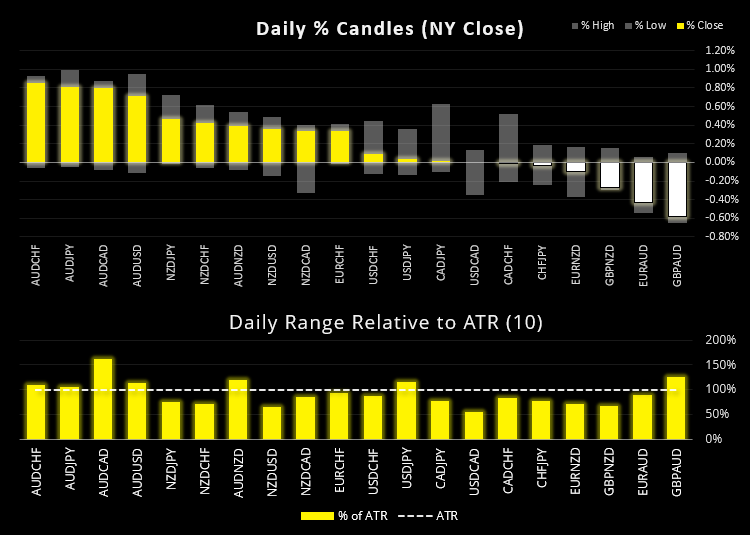

Forex: AUD and NZD extend gains

Antipodean currencies (AUD and NZD) were the strongest major overnight. The Aussie found buyers after GDP didn’t soften as much as feared whilst NZD was supported thanks to an ease in lockdown restrictions, despite a rise on COVID-19 cases yesterday.

AUD/CAD closed firmly above trend resistance (projected from the 2021 high) and has found resistance around the 0.9300 high where the weekly R2 and monthly R1 pivots reside. Our bias remains bullish above yesterday’s low.

The US dollar index (DXY) was around -0.12% lower and printed a small bearish outside day, yet bears are struggling to break it convincingly beneath the August 16th low and support has been found around the 50-day eMA.

Learn how to trade forex

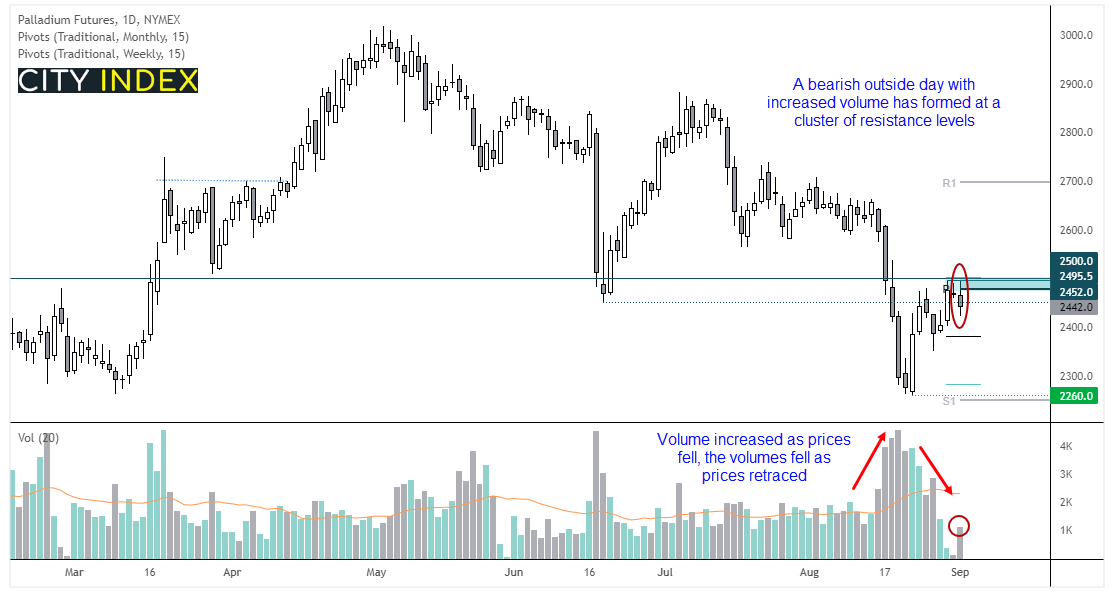

Commodities: Palladium prints potential swing high

Palladium may have set a swing high overnight below a resistance cluster. The decline from 2600 was seen in increasing volumes as bears piled in, yet the rebound from 2260 was seen on lower volumes as bears cashed out. As discussed in yesterday’s video we were looking for a reversal candle at resistance on higher volume, and yesterday’s bearish outside day at resistance ticks those boxes.

Oil prices fell over -3% yesterday before recovering later in the session, after OPEC+ decided to stick to their plan of gradually increasing output and also upgraded their demand forecasts. Separately, Iran are reportedly going ahead with oil exports in defiance against US sanction which likely capped gains. WTI settled at 68.23 and down -0.4% on the day and printing a Doji above its 20-day eMA yet below 70.0 resistance. Brent fell -0.34% and closed above its 50-day eMA.

Gold was effectively flat and produced a small Doji candle. We remain bullish above 1800 but, as of yet, the market lacks a catalyst ahead of tomorrow’s Nonfarm payrolls report.

Despite a weaker US dollar, copper prices fell to a 3-day low following softer PMI data across Europe. Due to the volatility of yesterday’s candle we’d prefer to step aside for now and wait for a higher low to form on low volatility.

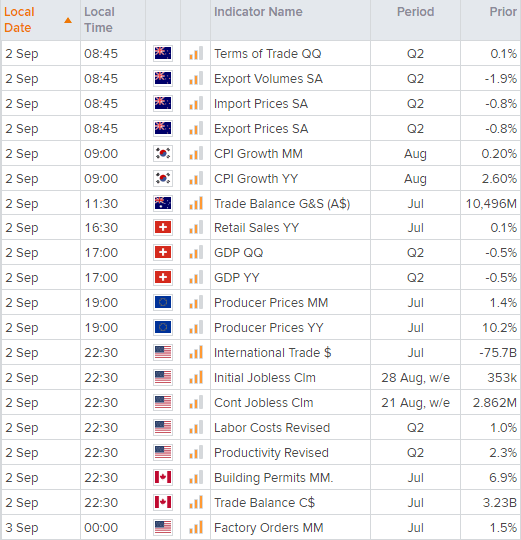

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 08:33 AM

Latest Indices articles

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM