Asia Morning: US Stocks Dragged By US-China Tensions, Jobless Claims

On Thursday U.S. stocks closed lower, dragged by renewed tensions between the U.S. and China. While reiterating his disappointment with China's response to the coronavirus crisis, U.S. President Donald Trump claimed China was behind a disinformation and propaganda attack on the U.S. and Europe.

Sentiment was also dampened by an official report that over two million Americans applied for unemployment benefits.

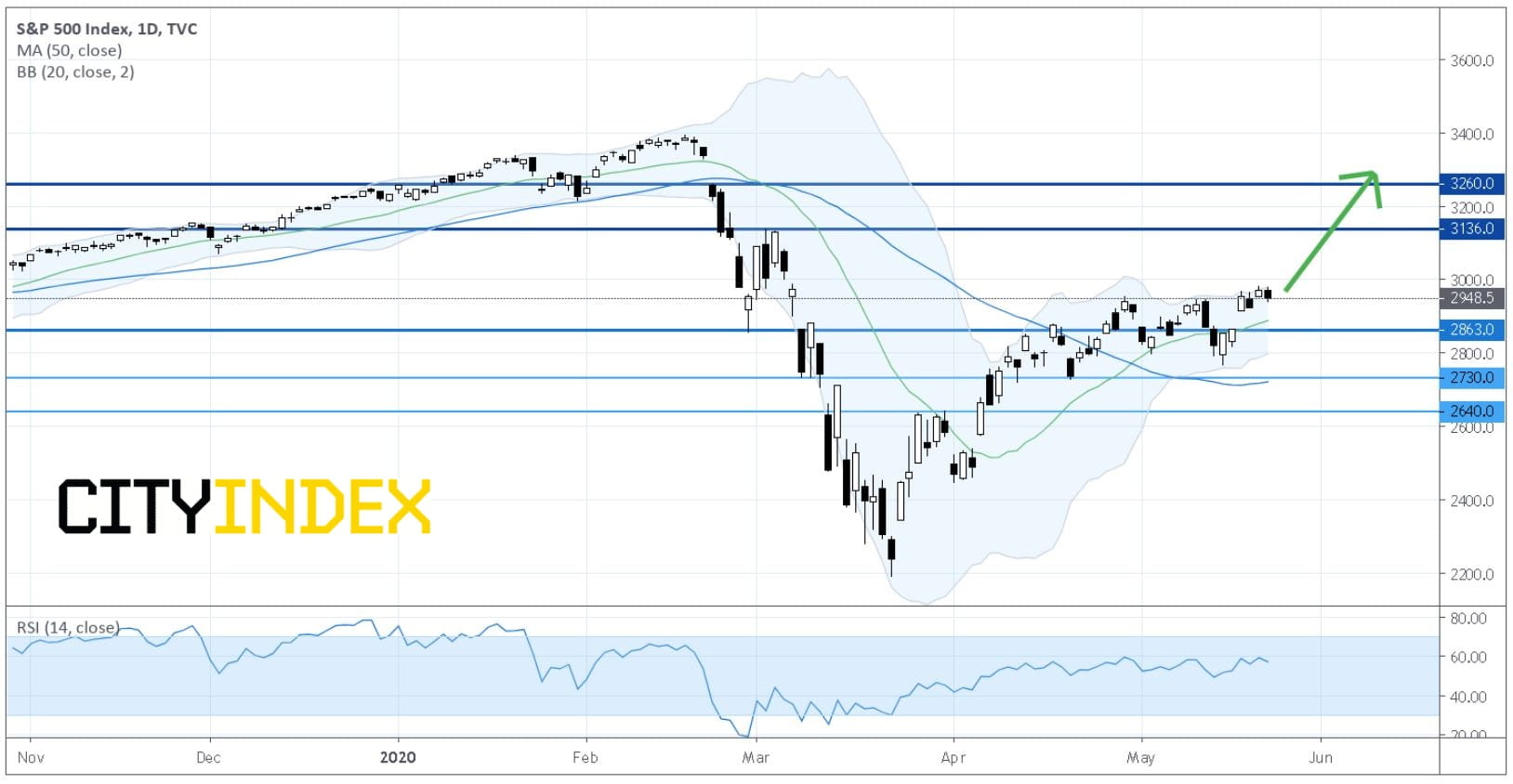

The Dow Jones Industrial Average fell 101 points (-0.4%) to 24474, the S&P 500 dropped 23 points (-0.8%) to 2948, and the Nasdaq 100 was down 107 points (-1.1%) to 9378.

Source: GAIN Capital, TradingView

Semiconductors & Semiconductor Equipment (-2.53%), Energy (-1.48%) and Software & Services (-1.27%) sectors lost the most.

National Oilwell Varco (NOV -6.77%), DXC Technology (DXC -6.65%), Boston Scientific (BSX -6.43%) and Take-Two Interactive Software (TTWO -5.89%) were top losers. Meanwhile, L Brands (LB +18.25%), Gap (GPS +11.58) and Norwegian Cruise Line (NCLH +9.78%) gained the most.

On the technical side, about 35.0% (30.0% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average, and 73.1% (61.2% in the prior session) were above their 20-day moving average.

The U.S. Labor Department reported that Initial Jobless Claims declined to 2.438 million (2.400 million expected) in the week ended May 16 while Continuing Claims surged to 25.073 million in the week ended May 9 (24.250 million expected),

U.S. Existing Home Sales decreased to an annualized rate of 4.33 million units in April (4.22 million units expected). The Markit U.S. Manufacturing Purchasing Mangers' Index (preliminary reading) rose to 39.8 in May (40.0 expected). The Conference Board Leading Index fell 4.4% on month in April (-5.4% expected).

European stocks eased, with the Stoxx Europe 600 Index dropping 0.8%. Germany's DAX lost 1.4%, the U.K.'s FTSE 100 declined 0.9% and France's CAC was down 1.2%.

U.S. Treasury prices advanced further, as the benchmark 10-year Treasury yield slipped to 0.667% from 0.679%.

Spot gold price shed $21 (-1.2%) to $1,725 an ounce.

U.S. WTI crude oil futures (July) marked a day-high of $34.66 before retreating to close at $33.64, up 0.5% on day.

On the forex front, the ICE U.S. Dollar Index rebounded 0.2% on day to 99.42, snapping four-day decline. Federal Reserve Vice Chairman Richard Clarida said "additional support from both monetary and fiscal policies may be called for", while Treasury Secretary Steven Mnuchin said another fiscal package is likely to be needed to support the economy.

Sentiment was also dampened by an official report that over two million Americans applied for unemployment benefits.

The Dow Jones Industrial Average fell 101 points (-0.4%) to 24474, the S&P 500 dropped 23 points (-0.8%) to 2948, and the Nasdaq 100 was down 107 points (-1.1%) to 9378.

Source: GAIN Capital, TradingView

Semiconductors & Semiconductor Equipment (-2.53%), Energy (-1.48%) and Software & Services (-1.27%) sectors lost the most.

National Oilwell Varco (NOV -6.77%), DXC Technology (DXC -6.65%), Boston Scientific (BSX -6.43%) and Take-Two Interactive Software (TTWO -5.89%) were top losers. Meanwhile, L Brands (LB +18.25%), Gap (GPS +11.58) and Norwegian Cruise Line (NCLH +9.78%) gained the most.

On the technical side, about 35.0% (30.0% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average, and 73.1% (61.2% in the prior session) were above their 20-day moving average.

The U.S. Labor Department reported that Initial Jobless Claims declined to 2.438 million (2.400 million expected) in the week ended May 16 while Continuing Claims surged to 25.073 million in the week ended May 9 (24.250 million expected),

U.S. Existing Home Sales decreased to an annualized rate of 4.33 million units in April (4.22 million units expected). The Markit U.S. Manufacturing Purchasing Mangers' Index (preliminary reading) rose to 39.8 in May (40.0 expected). The Conference Board Leading Index fell 4.4% on month in April (-5.4% expected).

European stocks eased, with the Stoxx Europe 600 Index dropping 0.8%. Germany's DAX lost 1.4%, the U.K.'s FTSE 100 declined 0.9% and France's CAC was down 1.2%.

U.S. Treasury prices advanced further, as the benchmark 10-year Treasury yield slipped to 0.667% from 0.679%.

Spot gold price shed $21 (-1.2%) to $1,725 an ounce.

U.S. WTI crude oil futures (July) marked a day-high of $34.66 before retreating to close at $33.64, up 0.5% on day.

On the forex front, the ICE U.S. Dollar Index rebounded 0.2% on day to 99.42, snapping four-day decline. Federal Reserve Vice Chairman Richard Clarida said "additional support from both monetary and fiscal policies may be called for", while Treasury Secretary Steven Mnuchin said another fiscal package is likely to be needed to support the economy.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM