Energy companies such as Oneok (OKE -15.84%), Occidental Petroleum (OXY -16.14%) and Halliburton (HAL -15.37%) plummeted as oil prices plunged 8%.

Travel stocks such as Norwegian Cruise Line (NCLH -16.46%), American Airlines (AAL -15.51%) and Delta Air Lines (DAL -14.03%) also lost big.

On the technical side, about 51.7% (58.3% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average, and 93.3% (93.3% in the prior session) were above their 20-day moving average.

U.S. official data showed that Initial Jobless Claims fell to 1.542 million for the week ended June 6 (1.550 million expected), and Continuing Claims decreased to 20.929 million for the week ended May 30 (20.000 million expected). Producer Prices increased 0.4% on month in May (+0.1% expected),

Due later today is the University of Michigan's Consumer Sentiment Index (June preliminary reading, an increase to 75.0 expected).

European stocks were heavy yesterday, with the Stoxx Europe 600 Index shedding 4.1%. Germany's DAX sank 4.5%, France's CAC slumped 4.7%, and the U.K.'s FTSE 100 lost 4.0%.

U.S. government bonds were in demand for their haven appeal. The benchmark 10-year Treasury yield slid to 0.651% from 0.744% Wednesday.

Spot gold retreated $9.00 (-0.6%) to $1,727 an ounce, ending a three-day rebound.

Oil prices tumbled as market sentiment deteriorated sharply. U.S. WTI crude oil futures (July) plunged 8.2% to $36.34 a barrel.

On the forex front, the ICE U.S. Dollar Index rebounded 0.7% on day to 96.81, halting a three-day decline, amid risk-off sentiment.

EUR/USD slid 0.7% to 1.1295. The eurozone's April industrial production will be reported later in the day (-20.0% on month expected).

GBP/USD plunged 1.3% to 1.2580. Later today, U.K. monthly GDP growth for April (-18.7% on month expected), industrial production (-15.0% on month expected) and manufacturing production (-15.6% on month expected) will be released.

USD/JPY dipped 0.3% to 106.81, posting a four-day losing streak.

Asia Morning: U.S. Stocks Knocked by Bears, Dow Sinks 7%

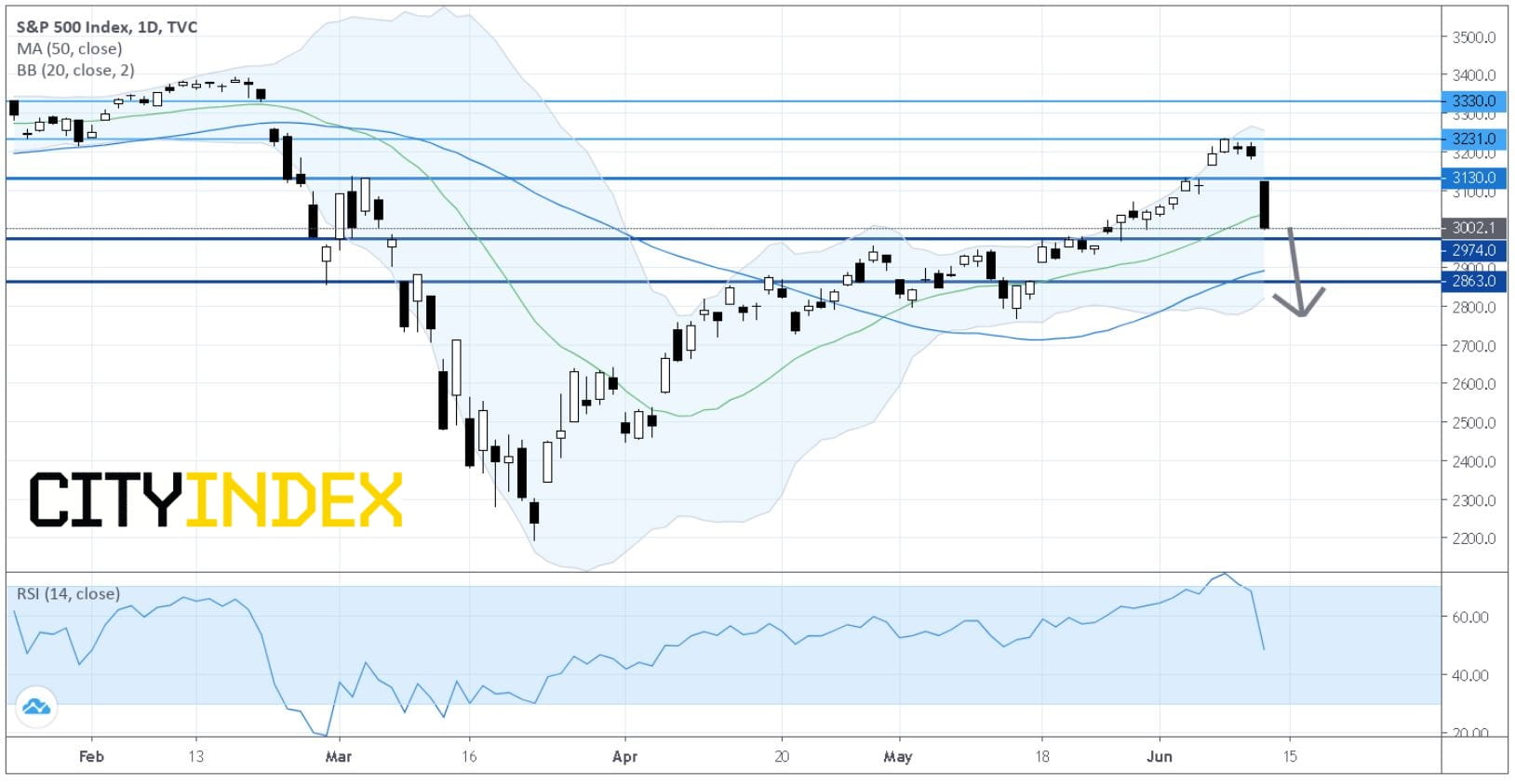

On Thursday, U.S. stocks suffered the worst sell-off since March 16, as investors were concerned about a resurgence in coronavirus infections and discouraged by the Federal Reserve's warning of a slower economic recovery. The Dow Jones Industrial Average slumped 1861 points (-6.9%) to 25128, the S&P 500 fell 188 points (-5.9%) to 3002, and the Nasdaq 100 was down 505 points (-5.0%) to 9588.

S&P 500 Index: Daily Chart

Source: GAIN Capital, TradingView

All of the S&P's sectors ended in negative territory, led by Banks (-9.6%), Energy (-9.45%) and Automobiles & Components (-9.26%).

Energy companies such as Oneok (OKE -15.84%), Occidental Petroleum (OXY -16.14%) and Halliburton (HAL -15.37%) plummeted as oil prices plunged 8%.

Travel stocks such as Norwegian Cruise Line (NCLH -16.46%), American Airlines (AAL -15.51%) and Delta Air Lines (DAL -14.03%) also lost big.

On the technical side, about 51.7% (58.3% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average, and 93.3% (93.3% in the prior session) were above their 20-day moving average.

U.S. official data showed that Initial Jobless Claims fell to 1.542 million for the week ended June 6 (1.550 million expected), and Continuing Claims decreased to 20.929 million for the week ended May 30 (20.000 million expected). Producer Prices increased 0.4% on month in May (+0.1% expected),

Due later today is the University of Michigan's Consumer Sentiment Index (June preliminary reading, an increase to 75.0 expected).

European stocks were heavy yesterday, with the Stoxx Europe 600 Index shedding 4.1%. Germany's DAX sank 4.5%, France's CAC slumped 4.7%, and the U.K.'s FTSE 100 lost 4.0%.

U.S. government bonds were in demand for their haven appeal. The benchmark 10-year Treasury yield slid to 0.651% from 0.744% Wednesday.

Spot gold retreated $9.00 (-0.6%) to $1,727 an ounce, ending a three-day rebound.

Oil prices tumbled as market sentiment deteriorated sharply. U.S. WTI crude oil futures (July) plunged 8.2% to $36.34 a barrel.

On the forex front, the ICE U.S. Dollar Index rebounded 0.7% on day to 96.81, halting a three-day decline, amid risk-off sentiment.

EUR/USD slid 0.7% to 1.1295. The eurozone's April industrial production will be reported later in the day (-20.0% on month expected).

GBP/USD plunged 1.3% to 1.2580. Later today, U.K. monthly GDP growth for April (-18.7% on month expected), industrial production (-15.0% on month expected) and manufacturing production (-15.6% on month expected) will be released.

USD/JPY dipped 0.3% to 106.81, posting a four-day losing streak.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM