Asia Morning: U.S. Stocks Pare Gains, But Close Higher

On Tuesday, U.S. stocks ended higher though paring gains throughout the session. The Dow Jones Industrial Average added 2 points to 27995, the S&P 500 rose 17 points (+0.52%) to 3401, and the Nasdaq 100 advanced 161 points (+1.43%) to 11438.

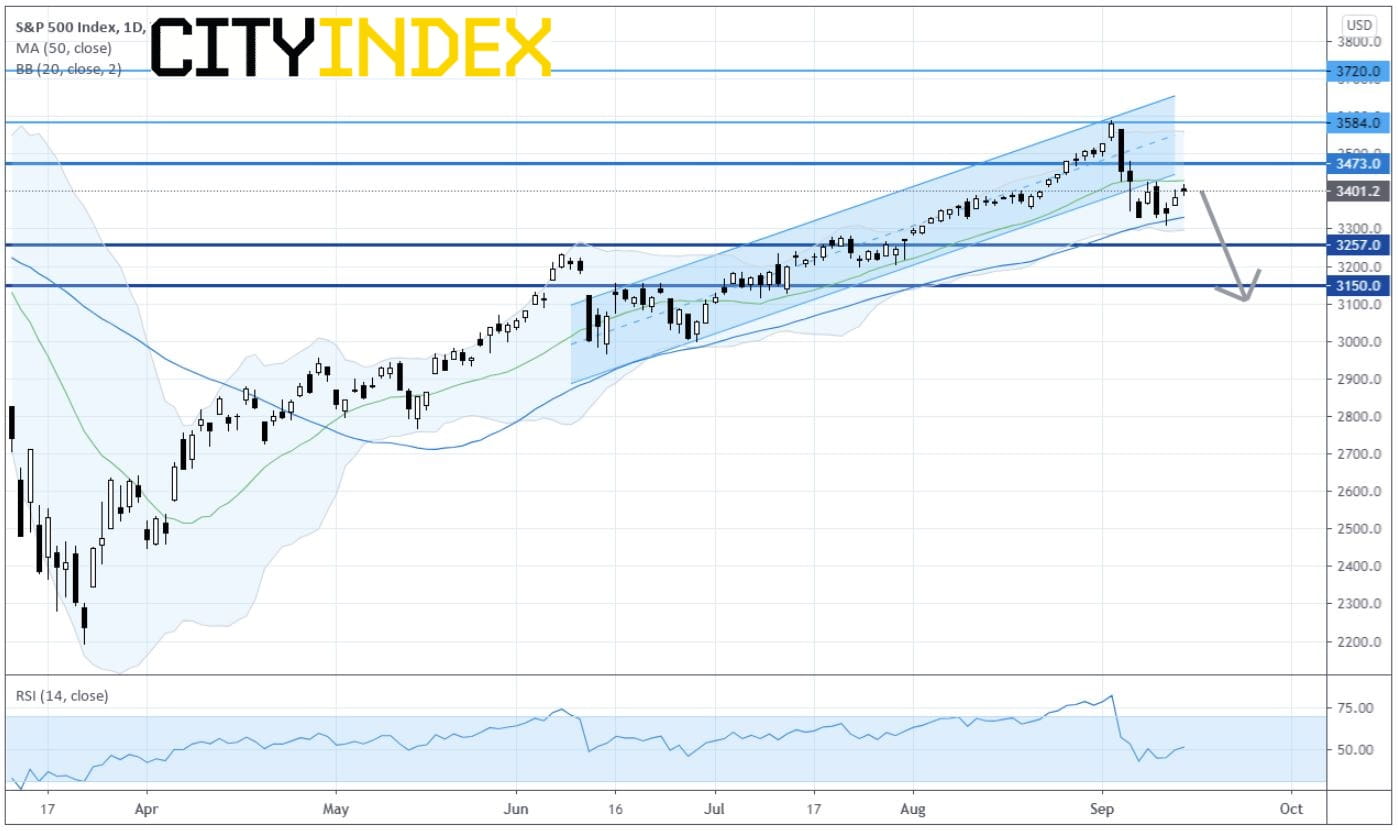

S&P 500 Index: Daily Chart

Sources: GAIN Capital, TradingView

Market sentiment was supported by upbeat U.S. economic data. The Empire Manufacturing Index jumped to 17.0 in September (6.9 expected), and Industrial Production advanced 0.4% on month in August (+1.0% expected).

Media (+1.95%), Retailing (+1.43%) and Real Estate (+1.39%) sectors performed the best. Alexion Pharmaceuticals (ALXN +6.31%), Qorvo (QRVO +5.82%) and Occidental Petroleum (OXY +5.31%) were the top gainers, while Carnival Corp (CCL -10.76%) and Citigroup (C -6.94%) were top losers.

JPMorgan Chase (JPM) dropped 3.11%.

Approximately 64.2% (60.2% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average and 52.5% (34.7% in the prior session) were trading above their 20-day moving average.

European stocks were broadly higher. The Stoxx Europe 600 Index increased 0.66%, Germany's DAX 30 added 0.18%, France's CAC 40 rose 0.32%, and the U.K.'s FTSE 100 jumped 1.32%.

The benchmark U.S. 10-year Treasury yield was stable at 0.678%.

U.S. WTI crude oil futures (October) advanced 2.7% to $38.28 a barrel. Traders were worried that the approaching Hurricane Sally would disrupt oil & gas production in northern U.S. Gulf Coast.

Spot gold jumped up to $1,972 an ounce before retreating to close at $1,954.

On the forex front, the ICE U.S. Dollar Index was flat on day at 93.07 ahead of the Federal Reserve's interest rate decision due later today. It is widely expected the central bank would stick to its accommodative monetary policy.

EUR/USD fell 0.2% to 1.1849. The German ZEW Current Situation Index improved to -66.2 in September (-72.0 expected) from -81.3 in August, and Expectations Index climbed to 77.4 (69.5 expected) from 71.5.

GBP/USD advanced 0.3% to 1.2888. Official data showed that U.K. jobless rate rose to 4.1% (as expected) in the three months to July from 3.9% in the prior period.

USD/JPY dropped 0.3% to 105.40. This morning, government data showed that Japan recorded a trade surplus of 248.3 billion yen in August (15 billion yen deficit expected), where exports declined 14.8% on year (-16.1% expected) and imports slid 20.8% (-17.8% expected).

USD/CAD gained 0.1% to 1.3188. Canada's manufacturing sales grew 7.0% on month in July (+9.0% expected), according to the government. Later today, Canada's CPI for August will be released (+0.4% on year expected).

Other commodity-linked currencies were broadly higher against the greenback. Both AUD/USD and NZD/USD gained 0.2% to 0.7303 and 0.6714 respectively. Official data showed that China's industrial production rose 5.6% on year in August (+5.1% expected) and retail sales grew 0.5% (flat expected).

S&P 500 Index: Daily Chart

Sources: GAIN Capital, TradingView

Market sentiment was supported by upbeat U.S. economic data. The Empire Manufacturing Index jumped to 17.0 in September (6.9 expected), and Industrial Production advanced 0.4% on month in August (+1.0% expected).

Media (+1.95%), Retailing (+1.43%) and Real Estate (+1.39%) sectors performed the best. Alexion Pharmaceuticals (ALXN +6.31%), Qorvo (QRVO +5.82%) and Occidental Petroleum (OXY +5.31%) were the top gainers, while Carnival Corp (CCL -10.76%) and Citigroup (C -6.94%) were top losers.

JPMorgan Chase (JPM) dropped 3.11%.

Approximately 64.2% (60.2% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average and 52.5% (34.7% in the prior session) were trading above their 20-day moving average.

European stocks were broadly higher. The Stoxx Europe 600 Index increased 0.66%, Germany's DAX 30 added 0.18%, France's CAC 40 rose 0.32%, and the U.K.'s FTSE 100 jumped 1.32%.

The benchmark U.S. 10-year Treasury yield was stable at 0.678%.

U.S. WTI crude oil futures (October) advanced 2.7% to $38.28 a barrel. Traders were worried that the approaching Hurricane Sally would disrupt oil & gas production in northern U.S. Gulf Coast.

Spot gold jumped up to $1,972 an ounce before retreating to close at $1,954.

On the forex front, the ICE U.S. Dollar Index was flat on day at 93.07 ahead of the Federal Reserve's interest rate decision due later today. It is widely expected the central bank would stick to its accommodative monetary policy.

EUR/USD fell 0.2% to 1.1849. The German ZEW Current Situation Index improved to -66.2 in September (-72.0 expected) from -81.3 in August, and Expectations Index climbed to 77.4 (69.5 expected) from 71.5.

GBP/USD advanced 0.3% to 1.2888. Official data showed that U.K. jobless rate rose to 4.1% (as expected) in the three months to July from 3.9% in the prior period.

USD/JPY dropped 0.3% to 105.40. This morning, government data showed that Japan recorded a trade surplus of 248.3 billion yen in August (15 billion yen deficit expected), where exports declined 14.8% on year (-16.1% expected) and imports slid 20.8% (-17.8% expected).

USD/CAD gained 0.1% to 1.3188. Canada's manufacturing sales grew 7.0% on month in July (+9.0% expected), according to the government. Later today, Canada's CPI for August will be released (+0.4% on year expected).

Other commodity-linked currencies were broadly higher against the greenback. Both AUD/USD and NZD/USD gained 0.2% to 0.7303 and 0.6714 respectively. Official data showed that China's industrial production rose 5.6% on year in August (+5.1% expected) and retail sales grew 0.5% (flat expected).

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM