Asia Morning: US Stocks Wiped Out Previous Gains, Pound Slumps

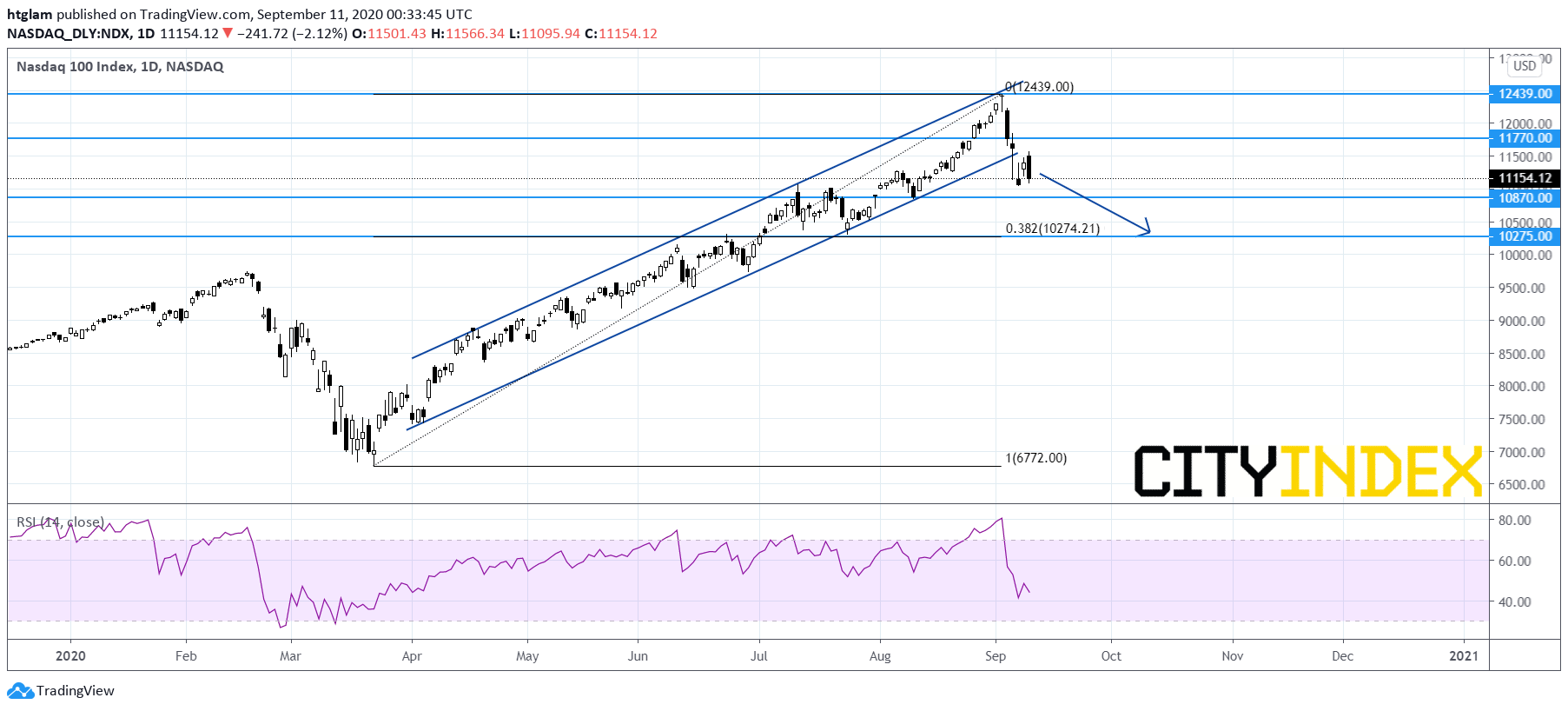

On Thursday, U.S. stocks closed lower and wiped out most of the gains in the prior session. The Dow Jones Industrial Average lost 405 points (-1.5%) to 27534, S&P 500 dropped 59 points (-1.8%) to 3339 and Nasdaq 100 slid 241 points (-2.1%) to 11154.

Nasdaq 100 daily chart:

Source: Gain Capital, TradingView

Energy (-3.67%), Automobiles & Components (-3.05%) and Technology Hardware & Equipment (-3.01%) sectors led the decline. Approximately 61.8% of stocks in the S&P 500 Index were trading above their 200-day moving average and 41.4% were trading above their 20-day moving average.

Regarding U.S. economic data, PPI fell 0.2% on year in August (-0.3% expected), while initial jobless claims totaled 884,000 in the week ending September 5 (850,000 expected), same as the prior week.

Later today, the U.S. Labor Department will release August CPI (+1.2% on year expected).

European stocks were broadly lower. The Stoxx Europe 600 Index lost 0.4%, Germany's DAX 30 slipped 0.2%, France's CAC 40 fell 0.4% and U.K.'s FTSE 100 was down 0.2%.

The benchmark U.S. 10-year Treasury yield retreated to 0.6772% from 0.7001% Wednesday.

WTI crude oil futures (October) slid 2.0% to $37.30 a barrel. The U.S. Energy Information Administration (EIA) reported that crude oil inventories rose 2.03 million barrels in the week ending September 4 (-1.96 million barrels expected).

Spot gold marked a day-high near $1,966 before closing flat at $1,946.

On the forex front, the U.S. dollar showed resilience as the ICE Dollar Index ended up 0.1% on day to 93.35, after marking a day-low at 92.70.

EUR/USD gained 0.2% to 1.1826. The European Central Bank kept its key rates and 1.35 trillion euros Pandemic Emergency Purchase Programme unchanged as expected, while lifting its 2020 eurozone GDP growth forecast to -8.0% from -8.7% previously. ECB President Christine Lagarde said "the Governing Council discussed the appreciation of the euro" and "will have to monitor carefully such matter", as exchange rate fluctuation could impact inflation.

GBP/USD plunged 1.4% to 1.2814. The European Commission warned the U.K. that "violating the terms of the Withdrawal Agreement would break international law" and called on the British government to withdraw its plan to overwrite parts of the Northern Ireland protocol by the end of the month. However, U.K. cabinet minister Michael Gove said they had made it "perfectly clear" it would not withdraw the bill.

On the other hand, U.K. July GDP growth (+6.7% on month expected) and industrial production (+4.1% on month expected) will be released later today.

USD/JPY was relatively flat at 106.15.

Commodity-linked currencies were broadly lower against the greenback. AUD/USD slipped 0.2% to 0.7265 and NZD/USD was down 0.5% to 0.6648, while USD/CAD gained 0.3% to 1.3186.

Latest market news

Today 08:15 AM

Today 05:45 AM

Latest Forex articles

Yesterday 11:09 PM

Yesterday 04:00 PM