Asia Morning: U.S. Stocks Charge Higher

On Thursday, U.S. stocks advanced further. The Dow Jones Industrial Average edged up 35 points (+0.13%) to 27816, the S&P 500 gained 17 points (+0.53%) to 3380, and the Nasdaq 100 jumped 165 points (+1.45%) to 11583.

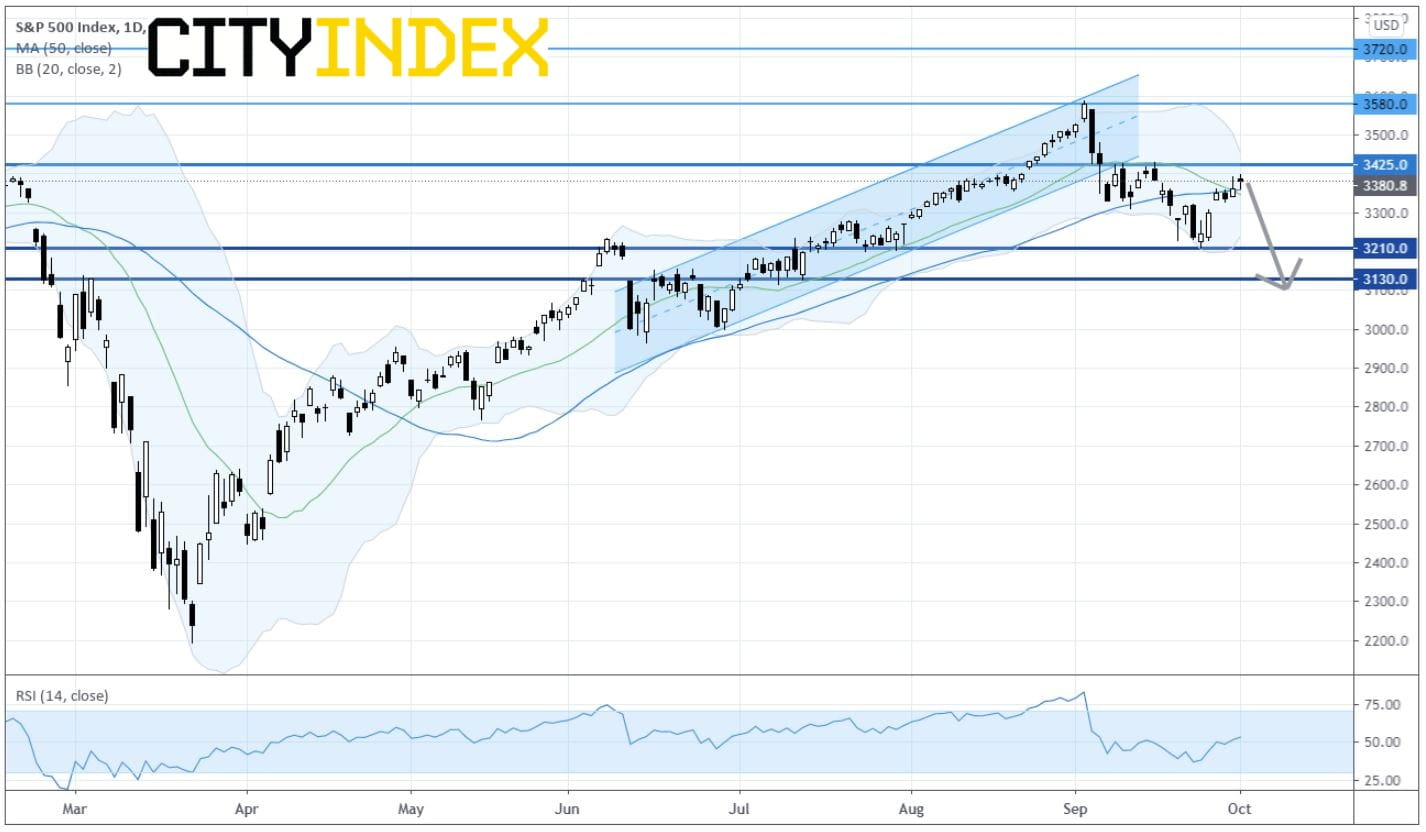

S&P 500 Index: Daily Chart

Sources: GAIN Capital, TradingView

The U.S. Labor Department reported that Initial Jobless Claims fell to 837,000 for the week ended September 26 (850,000 expected). Meanwhile, investors are eyeing closely the September Jobs Report due later today (an addition of 872,000 Nonfarm Payrolls, a drop in Jobless Rate to 8.2% expected).

Automobiles & Components (+2.18%), Retailing (+1.75%) and Media (+1.64%) sectors performed the best. Nordstrom (JWN +5.70%), Under Armour (UAA +5.61%), Coty (COTY +5.56%) and Netflix (NFLX +5.50%) were top gainers. Energy and related stocks, such as Halliburton (HAL -8.09%), Valero Energy (VLO -7.44%) and Marathon Petroleum (MPC -5.73%), lost big along with slumping oil prices.

Approximately 61% (59% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average and 49% (37% in the prior session) were trading above their 20-day moving average.

Official data showed that Personal Income slipped 2.7% on month in August (-2.5% expected). The Markit U.S. Manufacturing Purchasing Managers' Index unexpectedly declined to 53.2 in September (53.5 expected).

European stocks closed mixed. The Stoxx Europe 600 Index rose 0.20%, France's CAC 40 climbed 0.43% and the U.K.'s FTSE 100 was up 0.23%, while Germany's DAX 30 fell 0.23%,

In Japan, the Tokyo Stock Exchange halted all stock trading for an entire day Thursday citing a technical glitch. Normal trading is expected to resume on Friday.

The benchmark U.S. 10-year Treasury yield was little changed at 0.679%.

Spot gold rebounded $20 to $1,906 an ounce.

Crude oil encountered a sell-off for the second time this week. U.S. WTI crude oil futures (November) plunged 3.7% to $48.72 a barrel.

On the forex front, the U.S. dollar still lacked upward momentum. The ICE Dollar Index eased further to 93.72, extending its losing streak to a fourth session.

EUR/USD rose 0.24% to 1.1728. The Markit Germany Manufacturing Purchasing Managers' Index (PMI) for September posted at 56.4 (lower than 56.6 expected), and the Markit France Manufacturing PMI at 51.2 (higher than 50.9 expected).

GBP/USD declined 0.21% to 1.2892, halting a three-day rally. The Markit U.K. Manufacturing PMI for September was reported at 54.1 (lower than 54.3 expected).

USD/JPY edged up to 105.52. The Bank of Japan Tankan Large Manufacturers Index posted -27 for the third quarter (-24 expected) and the Outlook Index was -17 (-16 expected).

AUD/USD gained 0.31% to 0.7184, posting a four-day winning streak.

S&P 500 Index: Daily Chart

Sources: GAIN Capital, TradingView

The U.S. Labor Department reported that Initial Jobless Claims fell to 837,000 for the week ended September 26 (850,000 expected). Meanwhile, investors are eyeing closely the September Jobs Report due later today (an addition of 872,000 Nonfarm Payrolls, a drop in Jobless Rate to 8.2% expected).

Automobiles & Components (+2.18%), Retailing (+1.75%) and Media (+1.64%) sectors performed the best. Nordstrom (JWN +5.70%), Under Armour (UAA +5.61%), Coty (COTY +5.56%) and Netflix (NFLX +5.50%) were top gainers. Energy and related stocks, such as Halliburton (HAL -8.09%), Valero Energy (VLO -7.44%) and Marathon Petroleum (MPC -5.73%), lost big along with slumping oil prices.

Approximately 61% (59% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average and 49% (37% in the prior session) were trading above their 20-day moving average.

Official data showed that Personal Income slipped 2.7% on month in August (-2.5% expected). The Markit U.S. Manufacturing Purchasing Managers' Index unexpectedly declined to 53.2 in September (53.5 expected).

European stocks closed mixed. The Stoxx Europe 600 Index rose 0.20%, France's CAC 40 climbed 0.43% and the U.K.'s FTSE 100 was up 0.23%, while Germany's DAX 30 fell 0.23%,

In Japan, the Tokyo Stock Exchange halted all stock trading for an entire day Thursday citing a technical glitch. Normal trading is expected to resume on Friday.

The benchmark U.S. 10-year Treasury yield was little changed at 0.679%.

Spot gold rebounded $20 to $1,906 an ounce.

Crude oil encountered a sell-off for the second time this week. U.S. WTI crude oil futures (November) plunged 3.7% to $48.72 a barrel.

On the forex front, the U.S. dollar still lacked upward momentum. The ICE Dollar Index eased further to 93.72, extending its losing streak to a fourth session.

EUR/USD rose 0.24% to 1.1728. The Markit Germany Manufacturing Purchasing Managers' Index (PMI) for September posted at 56.4 (lower than 56.6 expected), and the Markit France Manufacturing PMI at 51.2 (higher than 50.9 expected).

GBP/USD declined 0.21% to 1.2892, halting a three-day rally. The Markit U.K. Manufacturing PMI for September was reported at 54.1 (lower than 54.3 expected).

USD/JPY edged up to 105.52. The Bank of Japan Tankan Large Manufacturers Index posted -27 for the third quarter (-24 expected) and the Outlook Index was -17 (-16 expected).

AUD/USD gained 0.31% to 0.7184, posting a four-day winning streak.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM