Asia Morning: U.S. Stocks Charge Higher, Travel Shares Soar

On Wednesday, U.S. stocks advanced further. The Dow Jones Industrial Average gained 227 points (+0.85%) to 26870 extending its winning streak to a fourth session. The S&P 500 rose 29 points (+0.91%) to 3226, and the Nasdaq 100 was up 12 points (+0.11%) to 10701.

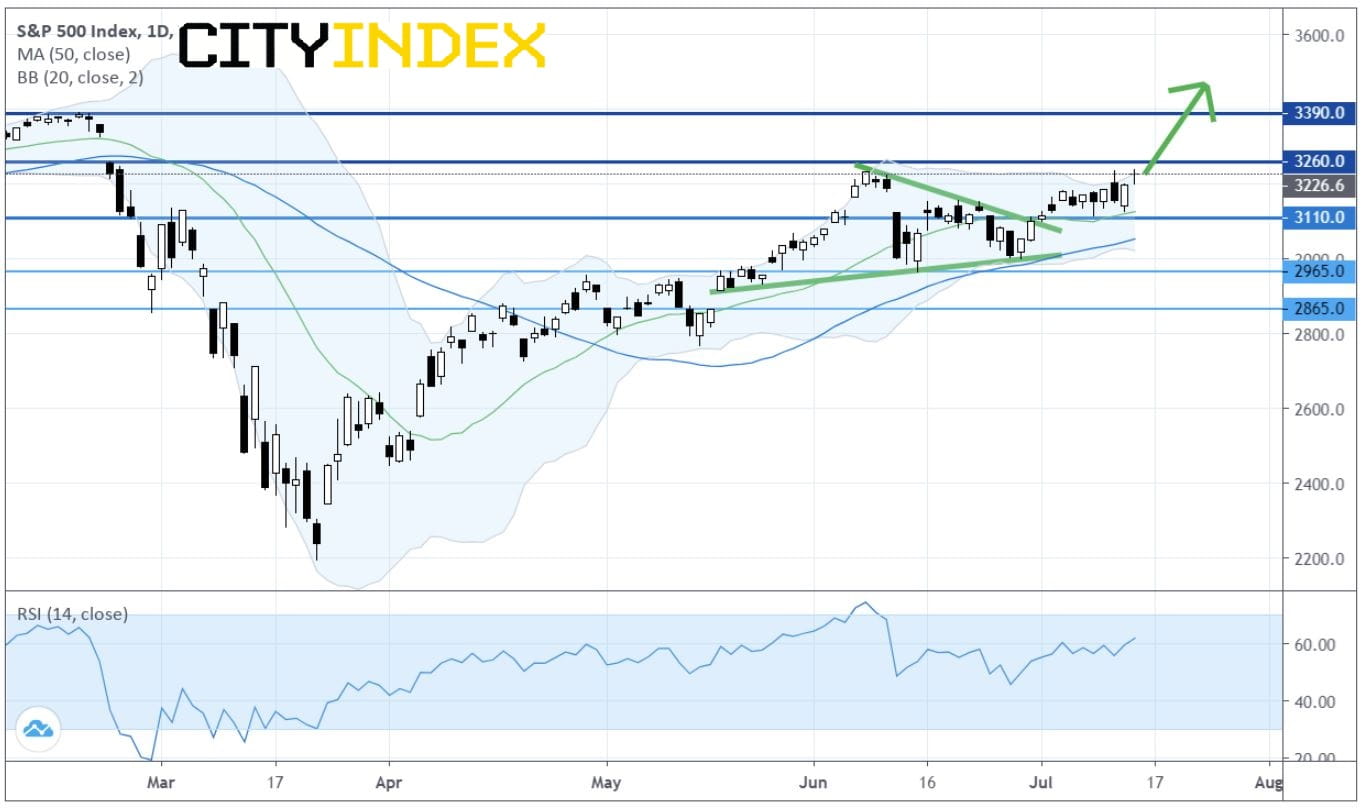

S&P 500 Index: Daily Chart

Source: GAIN Capital, TradingView

Investors were cheered by positive results from a COVID-19 vaccine trial by Moderna (MRNA +6.90%). Goldman Sachs' (GS +1.35%) better-than-expected earnings and President Donald Trump's remarks on infrastructure projects also boosted market sentiment.

Automobiles & Components (+4.99%), Consumer Services (+4.32%) and Transportation (+2.92%) sectors performed the best.

Travel-related stocks such as Royal Caribbean Cruises (RCL +21.20%), Norwegian Cruise Line (NCLH +20.68%), Carnival Corp (CCL +16.22%), American Airlines (AAL +16.16%), United Airlines (UAL +14.59% to $36.37) and Delta Air Lines (DAL +9.54% to $28.6) were top gainers.

On the technical side, about 46.8% (42.6% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average, and 65.1% (47.7% in the prior session) were trading above their 20-day moving average.

The U.S. Federal Reserve's latest Beige Book economic report stated that economic activity increased in most Districts, but remained far below where it was before the COVID-19 pandemic. And payrolls in all Districts were well below pre-COVID levels, the report said.

U.S. official data showed that Industrial Production rose 5.4% on month in June (+4.3% expected). The Empire Manufacturing Index spiked to 17.2 in July (10.0 expected).

Due later today are reports on Retail Sales (+5.0% on month in June expected) and Initial Jobless Claims (a decline to 1.250 million for the week ended July 11 expected).

European stocks rebounded. The Stoxx Europe 600 Index jumped 1.76%. Germany's DAX 30 advanced 1.84%, France's CAC 40 surged 2.03%, and the U.K.'s FTSE 100 was up 1.83%.

U.S. government bond prices eased, as the benchmark 10-year Treasury yield climbed to 0.629% from 0.617% Tuesday.

Spot gold price added $1.00 to $1,810 an ounce posting a three-session rally.

Oil prices jumped after the U.S. Energy Information Administration reported a surprise reduction of 7.49 million barrels in crude-oil stockpiles last week, in contrast to an addition of 250,000 barrels expected. U.S. WTI crude oil futures (August) gained 0.5% to $40.29 a barrel.

On the forex front, the ICE U.S. Dollar Index slipped 0.1% on day to 96.04, posting a four-day decline.

EUR/USD gained 0.2% to 1.1416. Investors will focus on the European Central Bank's interest rates decision due later in the day (expected to be unchanged).

GBP/USD climbed 0.3% to 1.2593. Official data showed that U.K. CPI grew 0.6% on year in June (+0.4% expected). On the other hand, Bank of England monetary policy committee member Silvana Tenreyro said she is ready to vote for further action to support the U.K. economy.

USD/JPY fell 0.3% to 106.91. The Bank of Japan, as widely expected, kept its benchmark rate unchanged at -0.10% and maintained 10-year government bond target at about 0%.

USD/CAD dropped 0.8% to 1.3506. The Bank of Canada held its benchmark rate at 0.25% as expected and said the rate will be maintained at current level until inflation objective is achieved. Meanwhile, government data showed that Canada's manufacturing sales increased 10.7% on month in May (+9.0% expected).

S&P 500 Index: Daily Chart

Source: GAIN Capital, TradingView

Investors were cheered by positive results from a COVID-19 vaccine trial by Moderna (MRNA +6.90%). Goldman Sachs' (GS +1.35%) better-than-expected earnings and President Donald Trump's remarks on infrastructure projects also boosted market sentiment.

Automobiles & Components (+4.99%), Consumer Services (+4.32%) and Transportation (+2.92%) sectors performed the best.

Travel-related stocks such as Royal Caribbean Cruises (RCL +21.20%), Norwegian Cruise Line (NCLH +20.68%), Carnival Corp (CCL +16.22%), American Airlines (AAL +16.16%), United Airlines (UAL +14.59% to $36.37) and Delta Air Lines (DAL +9.54% to $28.6) were top gainers.

On the technical side, about 46.8% (42.6% in the prior session) of stocks in the S&P 500 Index were trading above their 200-day moving average, and 65.1% (47.7% in the prior session) were trading above their 20-day moving average.

The U.S. Federal Reserve's latest Beige Book economic report stated that economic activity increased in most Districts, but remained far below where it was before the COVID-19 pandemic. And payrolls in all Districts were well below pre-COVID levels, the report said.

U.S. official data showed that Industrial Production rose 5.4% on month in June (+4.3% expected). The Empire Manufacturing Index spiked to 17.2 in July (10.0 expected).

Due later today are reports on Retail Sales (+5.0% on month in June expected) and Initial Jobless Claims (a decline to 1.250 million for the week ended July 11 expected).

European stocks rebounded. The Stoxx Europe 600 Index jumped 1.76%. Germany's DAX 30 advanced 1.84%, France's CAC 40 surged 2.03%, and the U.K.'s FTSE 100 was up 1.83%.

U.S. government bond prices eased, as the benchmark 10-year Treasury yield climbed to 0.629% from 0.617% Tuesday.

Spot gold price added $1.00 to $1,810 an ounce posting a three-session rally.

Oil prices jumped after the U.S. Energy Information Administration reported a surprise reduction of 7.49 million barrels in crude-oil stockpiles last week, in contrast to an addition of 250,000 barrels expected. U.S. WTI crude oil futures (August) gained 0.5% to $40.29 a barrel.

On the forex front, the ICE U.S. Dollar Index slipped 0.1% on day to 96.04, posting a four-day decline.

EUR/USD gained 0.2% to 1.1416. Investors will focus on the European Central Bank's interest rates decision due later in the day (expected to be unchanged).

GBP/USD climbed 0.3% to 1.2593. Official data showed that U.K. CPI grew 0.6% on year in June (+0.4% expected). On the other hand, Bank of England monetary policy committee member Silvana Tenreyro said she is ready to vote for further action to support the U.K. economy.

USD/JPY fell 0.3% to 106.91. The Bank of Japan, as widely expected, kept its benchmark rate unchanged at -0.10% and maintained 10-year government bond target at about 0%.

USD/CAD dropped 0.8% to 1.3506. The Bank of Canada held its benchmark rate at 0.25% as expected and said the rate will be maintained at current level until inflation objective is achieved. Meanwhile, government data showed that Canada's manufacturing sales increased 10.7% on month in May (+9.0% expected).

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM