US Stocks Broadly Lower, RBA's Rates Decision in Focus

On Monday, the three major U.S. indices closed mixed. The Dow Jones Industrial Average lost 271 points (-0.9%) to 29638 and the S&P 500 slid 16 points (-0.5%) to 3621, while the Nasdaq 100 Index gained 10 points (+0.1%) to 12268. Energy (-5.4%), Banks (-2.9%) and Insurance (-2.0%) were the worst performing sectors.

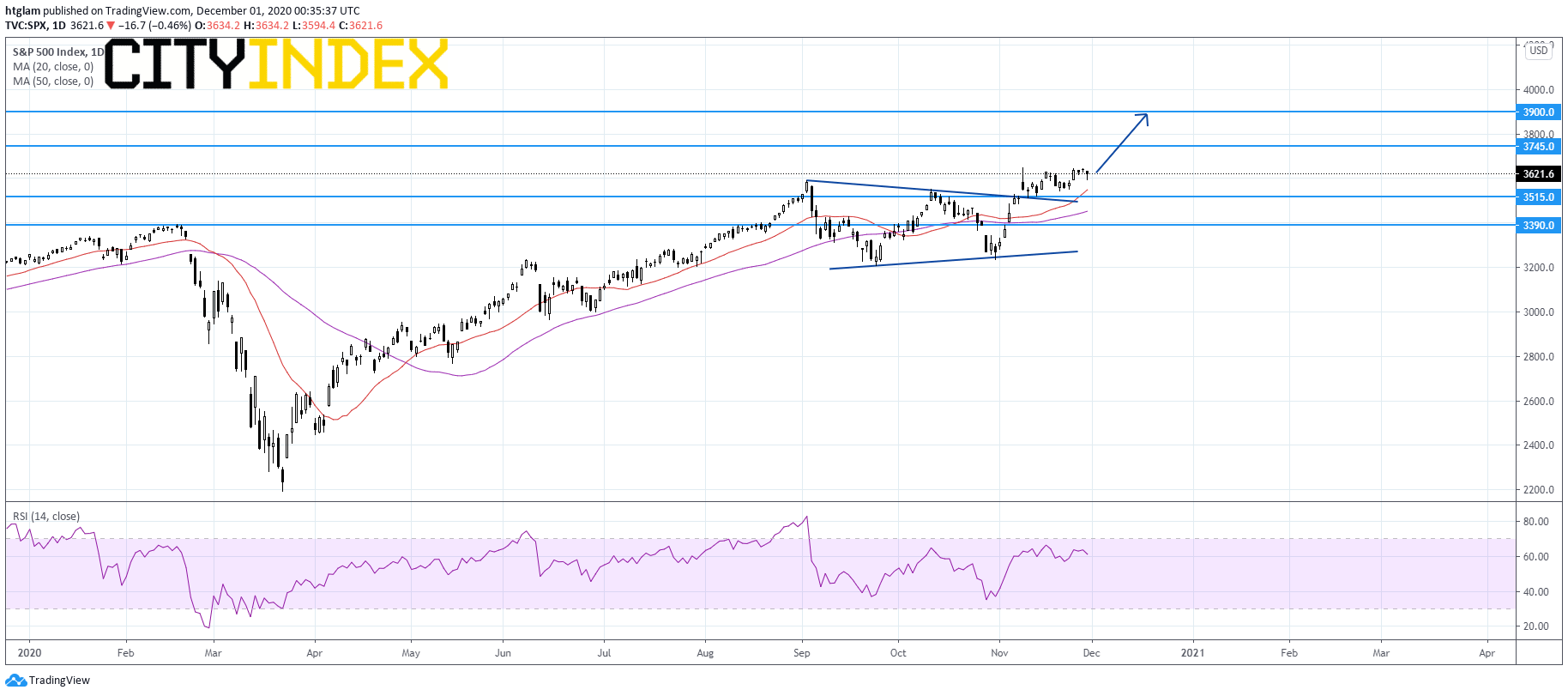

S&P 500 Index Daily Chart:

Source: GAIN Capital, TradingView

Approximately 93% of stocks in the S&P 500 Index were trading above their 200-day moving average and 82% were trading above their 20-day moving average. The VIX Index declined 0.25pt (-1.2%) to 20.59.

Regarding U.S. economic data, the Market News International's Chicago PMI fell to 58.2 in November (59.0 expected) from 61.1 in October, and pending home sales dropped 1.1% on month in October (+1.0% expected). Later today, the ISM Manufacturing Index for November (58.0 expected) and construction spending for October (+0.8% on month expected) will be released.

European stocks were broadly under pressure. The Stoxx Europe 600 declined 1.0%, Germany's DAX fell 0.3%, France's CAC 40 slid 1.4%, and the U.K.'s FTSE 100 sank 1.6%.

The benchmark U.S. 10-year Treasury yield climbed to 0.8389% from 0.8373% in the prior session.

WTI crude futures slipped 0.4% to $45.34 a barrel.

Spot gold dropped 0.6% to $1,777 an ounce.

On the forex front, the ICE U.S. Dollar Index rebounded from a seven-month low, climbing 0.3% to 91.99.

EUR/USD lost 0.3% to 1.1933. The eurozone's CPI for November will be reported later in the day (-0.2% on year expected).

GBP/USD was broadly flat at 1.3328.

USD/JPY bounced 0.2% to 104.35. This morning, government data showed that Japan's jobless rate rose to 3.1% in October (as expected) from 3.0% in September, while capital spending dropped 10.6% on year in the third quarter (-12.1% expected).

USD/CAD gained 0.1% to 1.3000. Investor will focus on Canada's third quarter annualized GDP data due later today (+47.7% on quarter expected).

AUD/USD slid 0.7% to 0.7347 despite stronger-than-expected Chinese economic data. China's official Manufacturing PMI rose to 52.1 in November (51.5 expected) from 51.4 in October and Non-manufacturing PMI climbed to 56.4 (56.0 expected) from 56.2. Later today, the Reserve Bank of Australia is expected to keep its benchmark rate at 0.10% unchanged.

Latest market news

Today 07:55 AM

Today 04:47 AM

Latest SPX 500 articles

Yesterday 04:54 PM

Yesterday 01:15 PM

April 14, 2024 08:20 PM

April 12, 2024 01:38 PM