Ashtead 8217 s shares warrant caution after stellar year

Ashtead Group shares climbed more than 10% to new all-time highs after the industrial machinery rental firm hiked full-year forecasts for the second time in […]

Ashtead Group shares climbed more than 10% to new all-time highs after the industrial machinery rental firm hiked full-year forecasts for the second time in […]

Ashtead Group shares climbed more than 10% to new all-time highs after the industrial machinery rental firm hiked full-year forecasts for the second time in 3 months.

The company, which hires out everything from small tools to large diggers and water pumps, said strong demand in its core US operations and Britain enabled a 33% surge in second-quarter pre-tax profit to £145.1m, bringing profits made in the six months to 31st October to £265.5m.

This latest upgrade from the group, follows another 33% pre-tax profit surge at the first-quarter point in September, which was also accompanied by raised guidance.

As in September, Ashtead has not quantified how much above forecasts it expects full-year profit to be.

Consensus suggests a £452m figure, judging by a poll of analysts’ forecasts compiled by Thomson Reuters.

Completing a recent hat-trick of 33% rises, the firm has also raised its interim dividend by 33% to 3p share.

Today’s earnings report again spotlights the firm as a sector darling, which continues to reap the benefits of its 85% revenue exposure to the United States, among one of the few regions in the world with an as good as unequivocal economic rebound.

One reason for its solid following in the market can be found by searching for its direct UK-listed peers. Ashtead does not appear to have any direct UK-listed rivals.

Construction tool rental firm Speedy Hire Plc. is close, but it’s not a provider of capital goods. Aggreko uses a similar rental (and leasing) business model as Ashtead, but its core service is provision of power and energy solutions.

The sparse playing field of direct Ashtead competitors helps explain its pre-eminence amongst investors in the broad industrial machinery sphere.

They have sent the stock 75% higher in the year-to-date compared with a hard-won 3% rise of the UK’s benchmark FTSE 100 index

Even so, there remain sound reasons for a degree of caution on Ashtead, even amid its bullish attitude on medium-term earnings

For one thing, we have the strong ties to the US economy.

Whilst robust, the rebound in North America has been prone to colder-than-average winter weather the States have experienced in recent years.

US GDP has dropped sharply during each winter quarter since 2011, save one, when the reading dumped almost two percentage points to near-zero, in the fourth quarter of 2012. Stabilisation always followed these economic tumbles.

Still, it’s presumptuous to dismiss 85% of revenue exposure to United States economic strength as a trivial potential risk.

It’s notable that whilst quarterly forecasts of US Industrial Production Index readings remain robust around 27 through 2015, economists’ assessments compiled by Thomson Reuters on average kick the assessment sharply lower in the first quarter of 2016, to 17.

Still, perhaps it’s too pessimistic to base Ashtead views on GDP forecasts more than a year into the future.

Especially as the firm’s earnings are backed by what seems to be a sensible capital strategy.

Its balance sheet suggests it has written down circa £300m on average in depreciation per annum in each of the last few years and beyond, whilst adjusting the P&L with a £300m capital investment each year.

The fixed asset profile of a firm like Ashtead, whose daily bread is capital goods, is important to watch, because the extent of depreciation and investment will have an impact on its book value, which in turn will affect market perceptions of valuation.

Interestingly, a group of major firms that are its closest peers suggests Ashtead trades at a forward 6% premium on price-to-book value, at 5 times, compared to Aggreko at 2.5 times and Weir on 2.3. Rotork Plc. and IMI join Ashtead with higher-than-average ratings.

Ashtead is also rated highest to group average on prospective price-to-earnings at 18.46 times, versus IMI’s 15.8 and Rotork’s 18.18.

The starkest differential is perhaps yield, which now lags almost everything in the FTSE 100 on a measly 1.1%.

The valuation needs careful thought against its almost entire dependence on the US economy, whilst the rest of the global economy is unmistakeably slowing down.

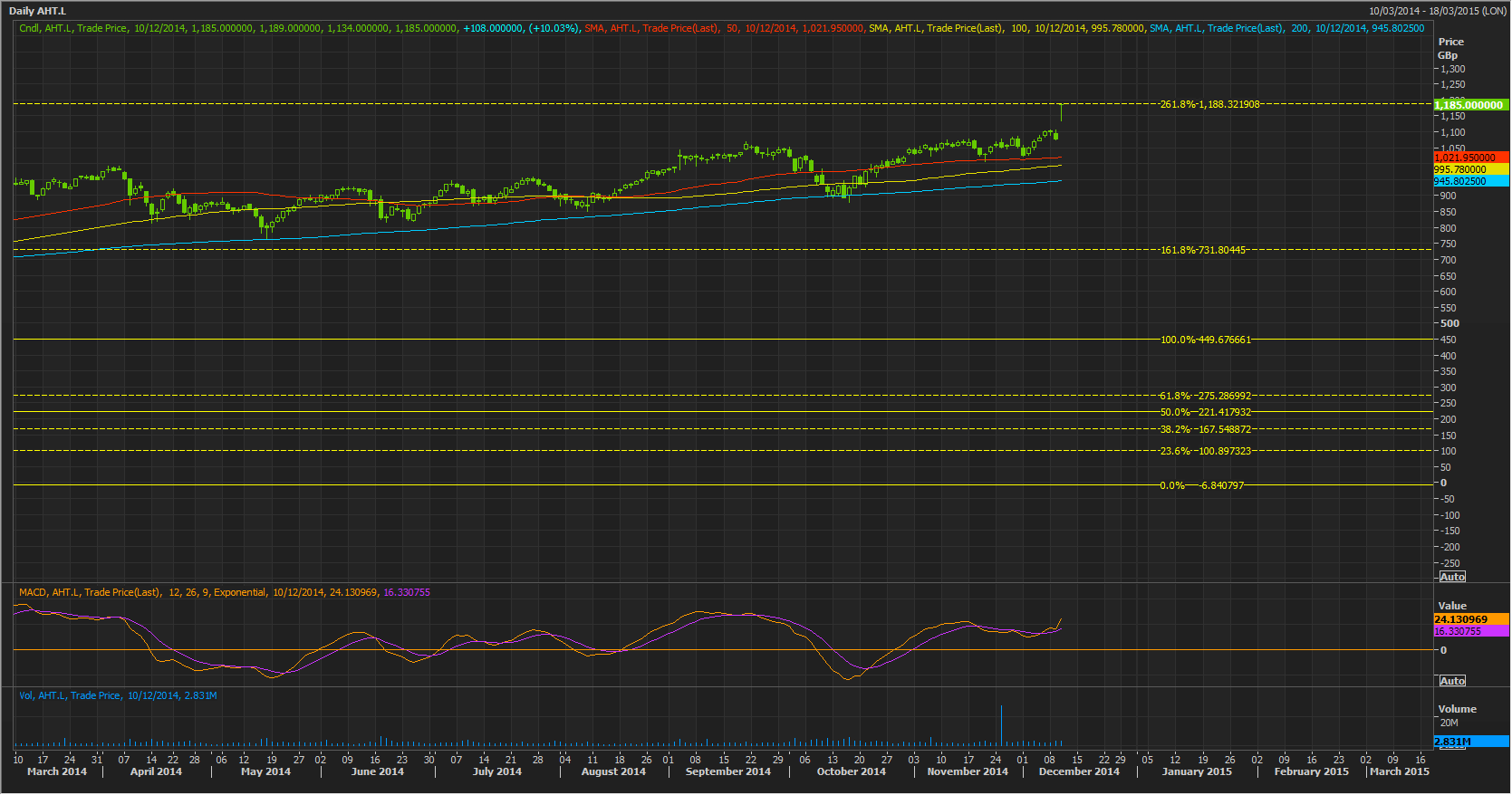

Remember Ashtead’s shares fell to to 45p during the global financial crisis, on a sharp fall in demand for industrial equipment.

The stock remains in 4 digits as I write though. Even if on a ‘first-listing date’ basis, projections off deep lows in March 2003 bring us to an immediately recognisable major Fibonacci level of 261.8%.

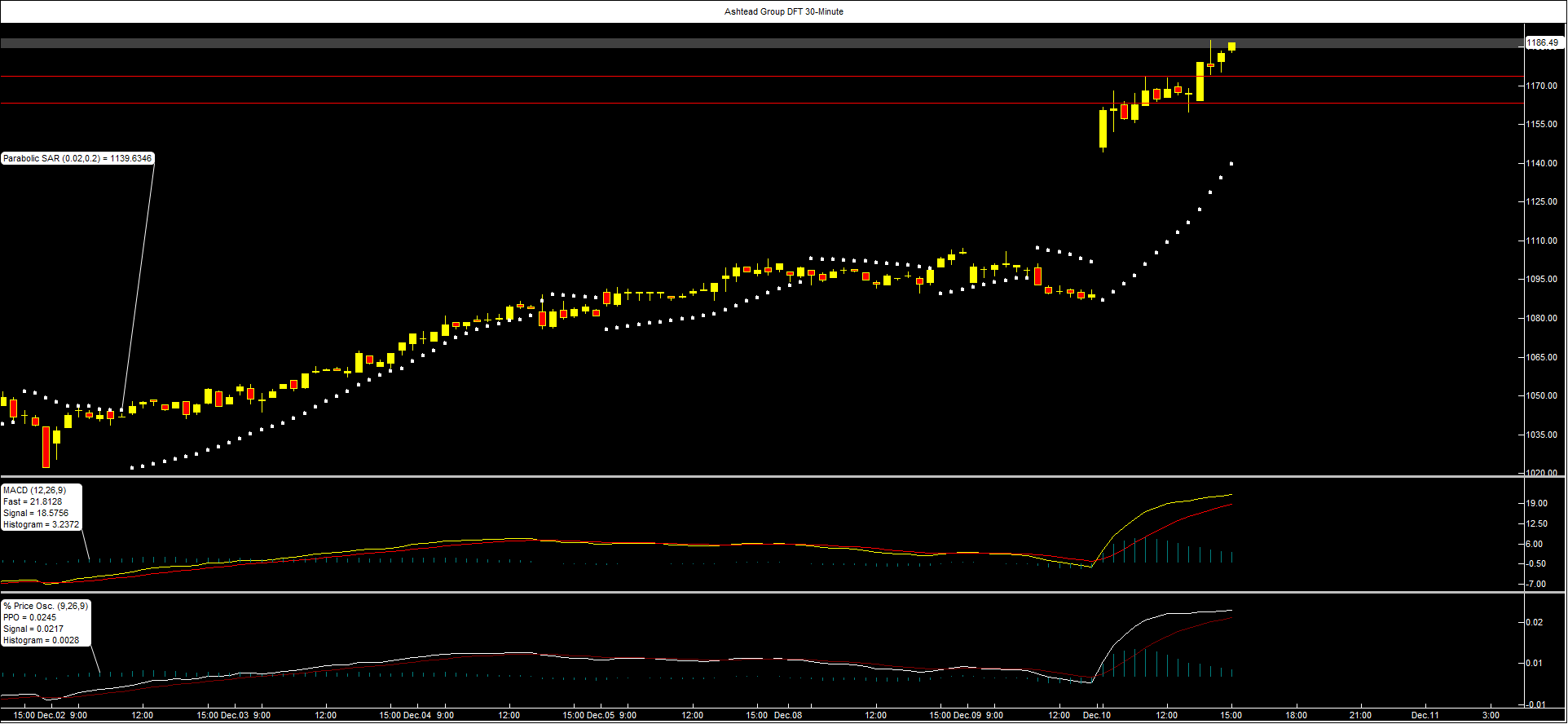

Almost inevitably, caution is creeping in amongst traders of City Index’s Ashtead Group Daily Funded Trade, which is also at equivalent all-time highs.

Still, I’m quite loath to call more than a moderate near-term softening, with likely supports nearby.