Article 50 decision and the pound It s all about the Sewel Convention

The pound has been the top performer versus the US dollar over the past week, but key event risks in the coming days could have […]

The pound has been the top performer versus the US dollar over the past week, but key event risks in the coming days could have […]

The pound has been the top performer versus the US dollar over the past week, but key event risks in the coming days could have a major bearing on the long-term trend of the pound. The first obstacle will be the Supreme Court’s decision, announced at 0930 GMT (approx.) on Tuesday, on whether to allow the UK Parliament a vote to trigger the official start of Article 50 and Brexit negotiations with the EU.

Theresa May’s government is fighting against this decision, but is widely expected to lose the case, which means that there is likely to be more parliamentary scrutiny over the Brexit process than previously assumed. More Brexit debate at Westminster has tended to be met with pound strength; when May delivered her Brexit plan last week the pound surged on her announcement that Parliament will be able to vote on the final Brexit deal with the EU. But, the Supreme Court’s decision could contain a stinger in the tail for pound bulls.

Analysing the Sewel Convention

This decision is not nearly as simple as giving parliament the right to vote on Article 50, it also touches on the Sewel Convention, which limits what Westminster can decide for Scotland’s devolved Parliament. Tuesday’s decision will also rule on whether or not to uphold this convention, which could have major ramifications not only Britain’s Brexit negotiations, but also on the future of the UK.

What to look for from the Supreme Court

The worst outcome for May would be a ruling that curbed Westminster’s power over the devolved administrations – the Supreme Court deciding to uphold the Sewel Convention. This would open up the possibility of Theresa May having to put her Brexit plans to a vote in Scotland, and perhaps Wales and Northern Ireland. This outcome would likely delay the UK’s Brexit plans, and, trigger the breakup of the UK, especially if it leads to another Independence Referendum in Scotland.

How the market may react to the decision

The Sewel Convention is an unusual legal quirk that very few people know anything about. This makes it hard to predict how the market will react to Tuesday’s decision. In an attempt to simplify this, we believe that there are two potential outcomes. Firstly, the government loses the case, but the Sewel Convention is not upheld: this could be good news for the pound, as parliament gets to debate and vote on Article 50, and the threat of UK breakup is avoided.

However, if the government loses the case, but the Sewel Convention is upheld, then the threat of an end to the UK, all in the name of Brexit, is fundamentally bearish for GBP/USD. In this scenario we could see excess volatility in sterling, as the initial impulse could be to buy the pound, but once the market has digested what the Sewel Convention means, then we could see GBP/USD hurtling back towards 1.20. Thus, the recent rising trend in GBP could be at risk in the next 24 hours.

UK GDP: did the economy end the year on a high note?

This is the question for Thursday, when the UK’s first reading of Q4 GDP is released. The market is looking for a 0.5% quarterly growth rate, down from the 0.6% rate of Q3. The annual rate is expected to moderate to a respectable 2.1% for 2016. But, weak trade and retail sales figures in the final months of 2016 tip the balance slightly to the downside for this GDP reading, the lowest economist estimate from Bloomberg is a mere 0.3%. If the figure is indeed weaker than expected, then this would be another reason to sell the pound.

It is worth remembering that the market seems happy to short the pound and, since June, rallies in GBP have tended to be weak and fizzle out. Thus, an adverse GDP reading, combined with a pound-negative decision from the Supreme Court on Tuesday could send GBP/USD back towards the key psychological level of 1.20, yet again. Of course, an upside surprise to the data could trigger another leg higher in the pound, and we could see back to the 1.2850 highs from early December.

May meets Trump: What to expect

At the end of this week Theresa May will meet President Trump for the first time in Washington. This meeting is important for the markets for two reasons. Firstly, President Trump said in a recent newspaper interview that the UK will get to the front of the queue regarding a trade deal with the US. The market will want to know if a deal was discussed between the UK and US leaders, and if this could boost the UK’s economic prospects once it leaves the EU.

The second thing to look for from this meeting is US/UK diplomatic relations. It is well known that members of Theresa May’s team did not view Trump as a credible Republican candidate, let alone President. Will the thin-skinned President let bygones be bygones, or will he openly criticise her for coming cap in hand begging for a trade deal? The latter would be bad news for the pound. But, if Trump can maintain a diplomatic, Presidential style, and commit to a future trade agreement with the UK, then this could be good news for both currencies, as concerns about the POTUS’ unconventional style may recede and boost the beleaguered dollar.

Overall, this is an important week for the pound, and it has got off to a flying start – it is the best performer in the G10 FX space over the last 7 days. Tuesday’s Supreme Court decision is the biggest risk to this rebound in sterling, in our view. Brexit politics have acted like kryptonite for the pound in the past, and if the decision threatens the break-up of the UK then we could see the recent sterling rally end abruptly.

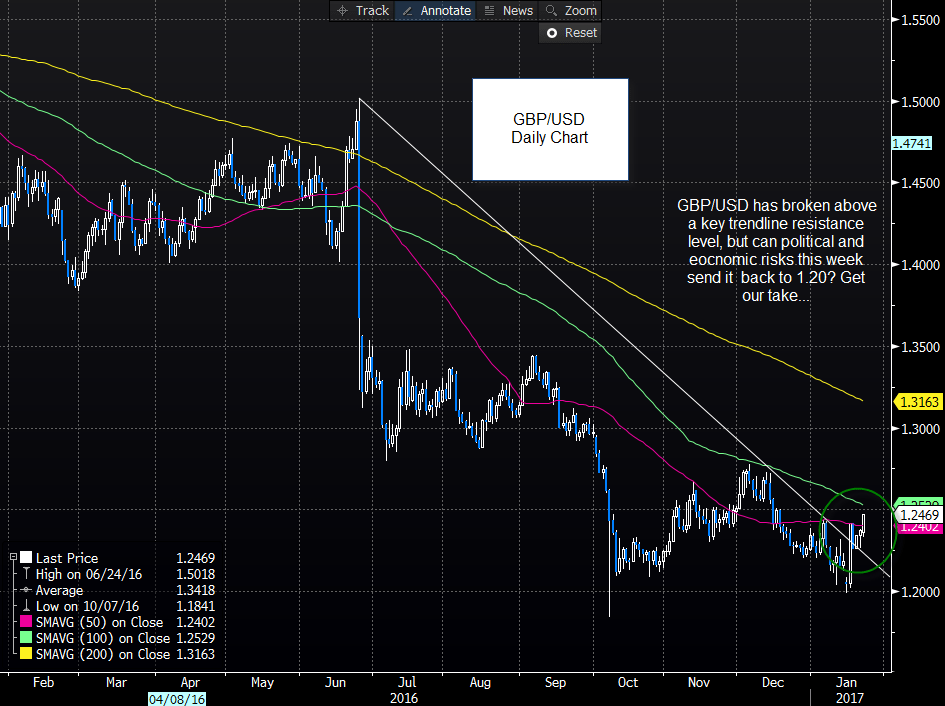

Chart 1:

Source: City Index and Bloomberg