ARM shares advance as it wins wrestle with growth critics

ARM Holdings shares led the UK’s benchmark FTSE 100 index this morning after it continued a run of earnings that confounded growth concerns. The British […]

ARM Holdings shares led the UK’s benchmark FTSE 100 index this morning after it continued a run of earnings that confounded growth concerns. The British […]

ARM Holdings shares led the UK’s benchmark FTSE 100 index this morning after it continued a run of earnings that confounded growth concerns.

The British company behind the processor in Apple’s iPhone 6 reported a better than expected 25% rise in profits on Wednesday, and predicted royalty income was set to get a big boost from smartphones.

With 3.5 billion chips made from designs owned by ARM in the prior quarter, pre-tax profit galloped 19% higher to £225.m, with an even split between licensing income and royalties, ARM said.

This beat forecasts in the market that had largely centred on a figure closer to £113m, according to data compiled by Thomson Reuters.

On top of that the firm’s chief financial officer Tim Score noted strong demand for its newest technology, which was currently powering chips in the top end of the smartphone segment, including the iPhone 6, launches in September.

“The outlook for royalty revenues this year is very encouraging,” he said.

“Most of the benefit we are going to see from the higher royalty rates is out in the future,” he told reporters.

His optimism seemed to be focused on ARM’s V8 architecture, through which the company claims to provide improved processing performance whilst maintaining the low-power consumption profile of its prior designs.

“By the time we exit 2015 probably as many as half of the smartphones that are out there will incorporate version 8 of the architecture,” Score told reporters on Wednesday morning.

By this means ARM said it expected total group dollar revenues for the first quarter to grow about 10% year on year, based on strengthening royalty revenue growth.

All in all, ARM today seems to be continuing to win the argument with critics who cite slowing overall demand for smartphones amid faster growth in cheaper handsets from Chinese manufacturers that command lower royalty rates.

It looks like the expanding market in the higher-margin chip designs will bolster ARM’s net income in the near term, whereas the view that its earnings could flatten over that period had been gaining traction in recent months.

Still, CFO Tim Score was careful not to suggest there was much chance of a resumption of ARM’s circa-15% dollar revenue growth rate of the last few years.

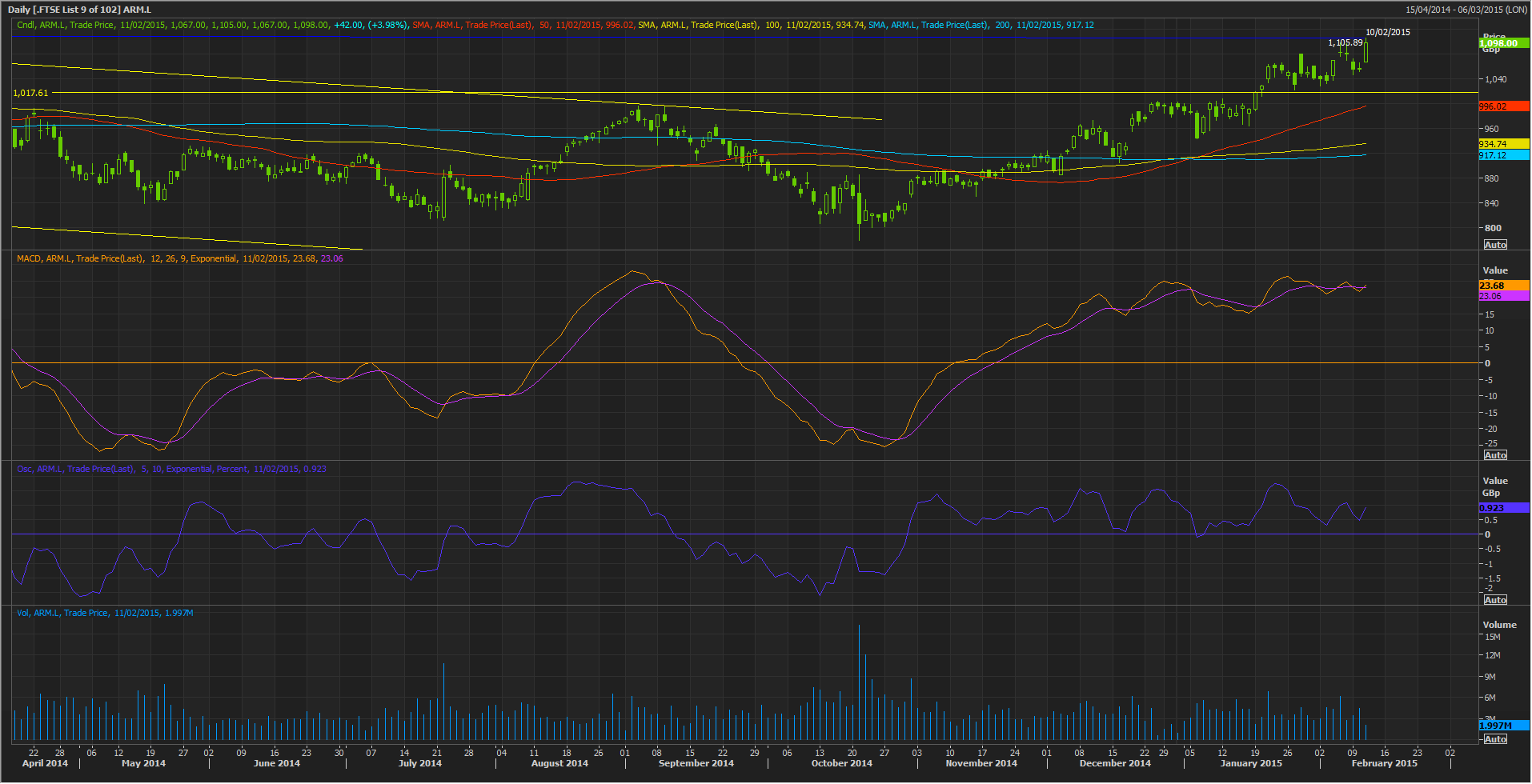

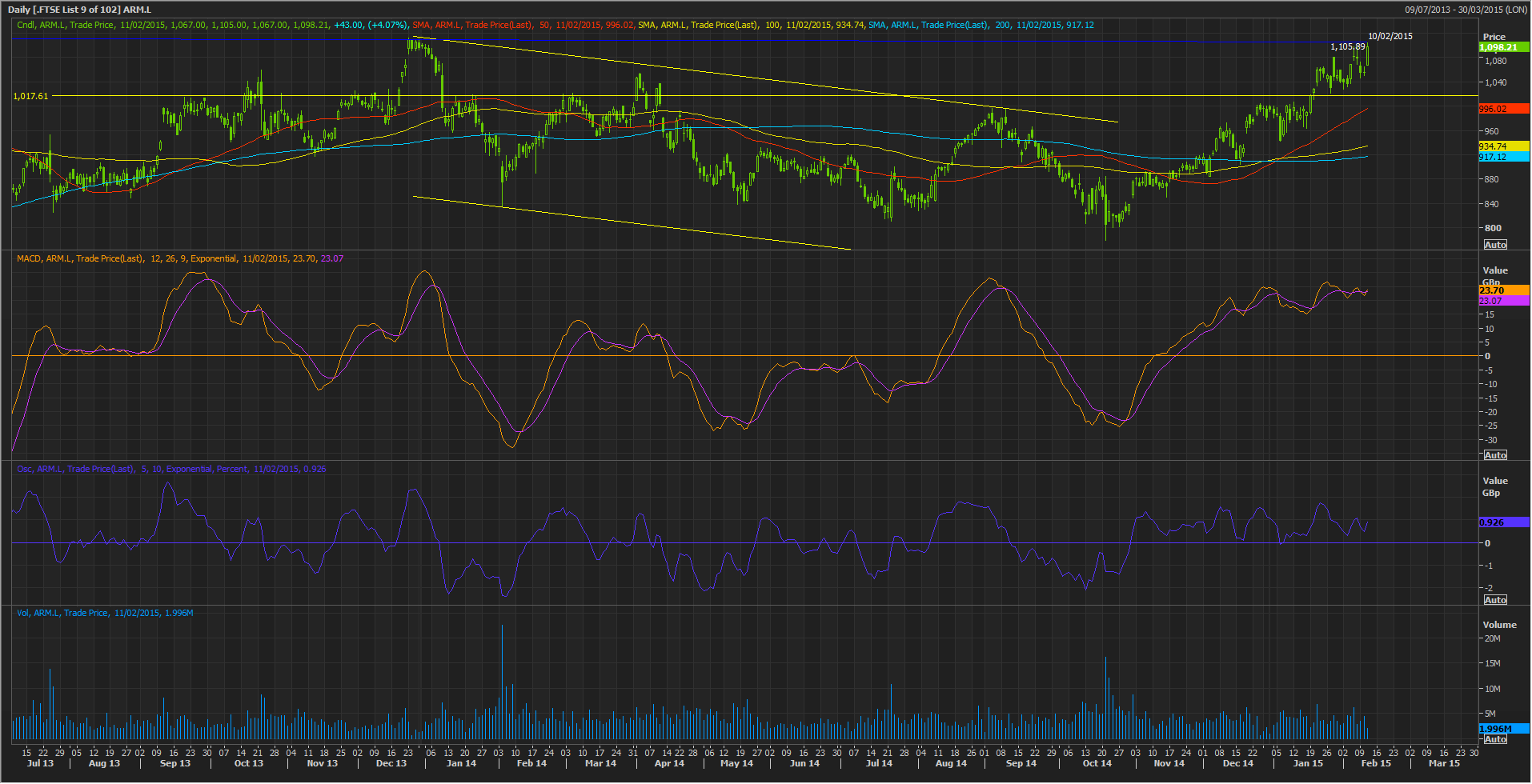

Overall then, cheer from the strong quarter essentially returns ARM, and its stock to the same confrontation with all-time highs that it faced twice two years ago, and didn’t quite reach last year.

It has to be said the stock’s chances of breaching this persistent resistance have never looked better.

The rebound from last autumn’s lows and the confirmation that it’s broken out of a wide descending trend channel that it entered in the latter part of 2013, are combining with strong upside momentum, on the daily chart.