ARM Holdings shares hinge on Q2 guidance not Apple

ARM Holdings will release earnings on Tuesday 21st April, though it may also have to fend off questions about being a potential takeover target. The […]

ARM Holdings will release earnings on Tuesday 21st April, though it may also have to fend off questions about being a potential takeover target. The […]

ARM Holdings will release earnings on Tuesday 21st April, though it may also have to fend off questions about being a potential takeover target.

The designer of the main microchips for virtually every smartphone in existence will report first-quarter earnings that are expected to be robust.

The Cambridge, United Kingdom-based firm already dropped strong hints about its Q1 in February.

ARM guided in its final quarterly earnings for 2014 that revenues in Q1 of the current year would probably be up at least 10%.

It cited “strengthening royalty revenue growth, and our expectation of the profile of licence revenue through the year.”

Since then however, the US dollar has risen by a further 5.5%, extending its longest and strongest uptrend for decades into an eighth month.

Given that ARM invoices in US dollars (whilst reporting earnings in sterling) its top-line earnings might well look stronger than guidance.

| ARM Holdings Q1 results: consensus forecasts | ||

| Year/year growth | ||

| Revenue | £222.60m | 19.2% |

| Cash EPS | £7.21 | 23.5% |

| Underlying net profit | £96.55m | 43.4% |

Forecasts compiled by Thomson Reuters

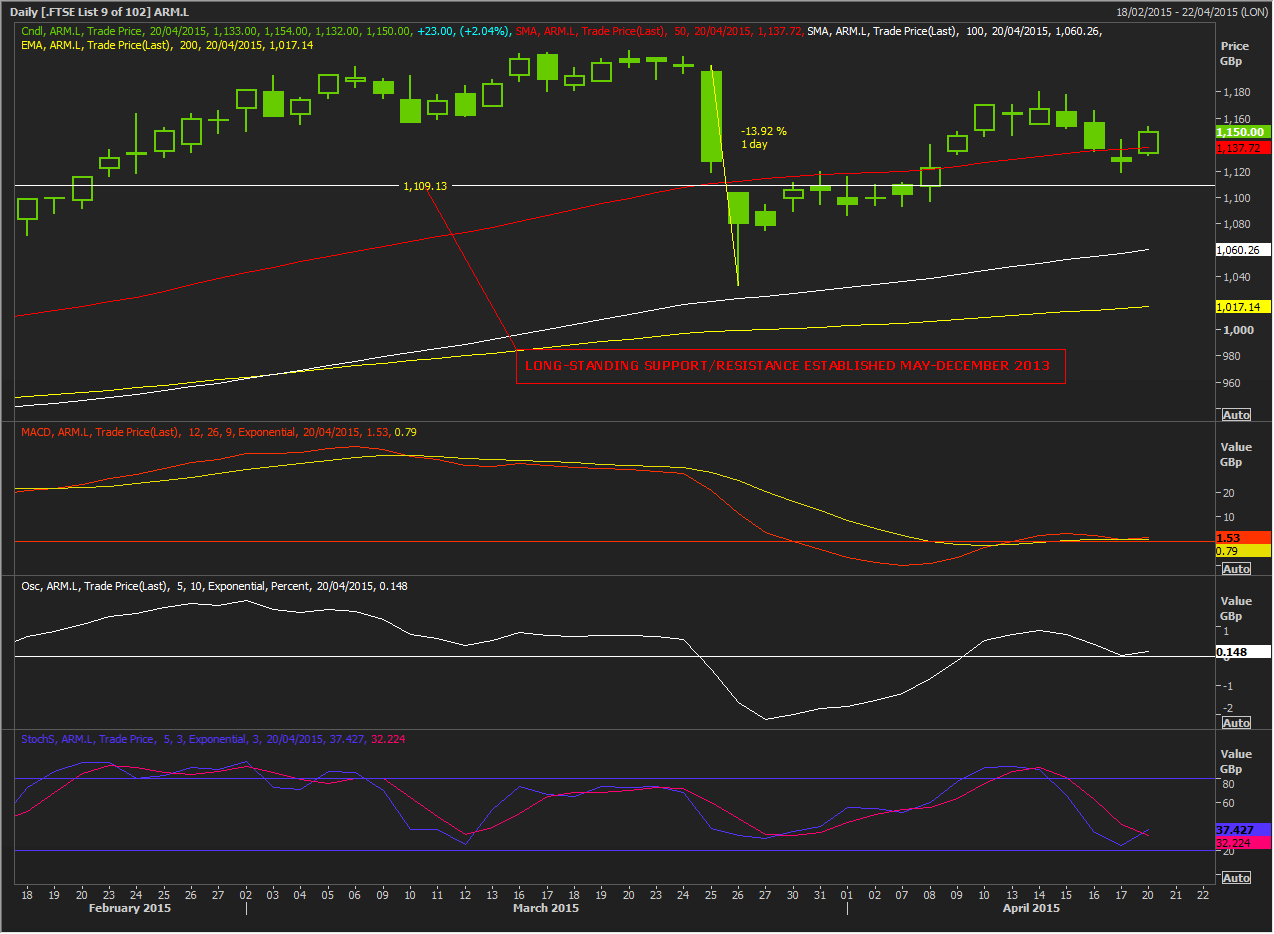

However, ARM has still been indirectly impacted by the dollar’s rally, with its shares dropping as much as 14% on an intraday basis between 25th and 26th March, as investors reacted to revenue forecast cuts by peer SanDisk.

More pointedly, ARM customer Taiwan Semiconductor Manufacturing (TSM) was also forced to warn last week that increasingly ferocious competition, easing smartphone demand in emerging markets and the rise of Taiwan’s dollar would push the Taipei-based firm’s Q2 sales 6.7% lower versus Q1.

TSM is certainly a bellwether for international chip sales, and this was backed up by industry data firm IDC saying smartphone shipments would grow 12% in 2015 from 26% in 2014.

If ARM customer purchases are indeed slowing down, the weakness could gradually start to show in ARM’s revenues in later quarters, and that has evidently begun to worry investors.

Especially after ARM shares advanced 53% between October and March.

It’s interesting how the emergence of such niggles often coincides with takeover talk.

Such talk is often a re-hash of already aired rumours too, and this was the case for ARM, when rumours apparently stemming from a Chinese news report bumped its stock up 21p on Thursday 9th April.

Once again, ARM’s lucrative and long-lasting relationship with Apple Inc. was at the root of the talk.

But common sense alone continues to argue against a consumation of the sort some market participants enthused about.

For one thing, Apple would be going about buying the UK firm in an odd way given that it has been steadily reducing its stake for years since its holding in ARM peaked in February 1999.

The Cupertino, California giant does not appear to own a level of ARM shares that would oblige it to report the holding to market regulators, according to ARM’s shareholder register.

More to the point, Apple’s purchase of ARM, close to the highest market value of the UK firm in its history, would risk ARM’s other clients taking their custom elsewhere.

It would be quite a silly acquisition on that basis.

A more pressing point to watch out for is whether currency effects have begun to weigh on consumer behaviour enough to impact ARM sales later in 2015.

Apple’s iPhone 6 phones especially are known to have seen record sales.

Sales of the new Samsung Galaxy S6 have also been the subject of promising reports.

These royalties would begin to show in the next quarter, making guidance a major focus.

Any updates on progress in adoption of ARM’s 64-bit V8 architecture, and big.LITTLE mobile processor should also be scrutinised closely.