Apple shares resume advance after blockbuster first quarter

Apple shares are set for a significant advance after the biggest company in the world by market capitalisation broke further records overnight with its first-quarter […]

Apple shares are set for a significant advance after the biggest company in the world by market capitalisation broke further records overnight with its first-quarter […]

Apple shares are set for a significant advance after the biggest company in the world by market capitalisation broke further records overnight with its first-quarter earnings.

Quarterly revenue was among the beats, with a 29.5% surge, helped by the well-trailed record iPhone 6 and iPhone 6 Plus sales.

74.7 million were sold, far above the estimate of 69 million that Wall Street settled on—with perhaps a little encouragement from Apple in recent weeks.

Still, 69 million was a classic ‘whisper’ number and the fact that actual units sold were far higher is a clear positive, even taking Apple’s expert ‘expectations management’ into account.

Wall St.’s best forecast for EPS was not close either, $2.69 was expected—and this was really the upper-end of expectations that consensus had gravitated to in the last few day.

With the help of a 70% expansion in Chinese revenues, Apple beat EPS calls too, posting $3.06.

Adding further spectacle as the night wore on, it emerged Apple had in fact broken not just its own records, but records for any other listed company in history.

It made an $18 billion profit in Q1, the biggest ever reported by a public company, worldwide, according to S&P.

Apple is also left with almost a record cash pile of $178bn. I think this once again raises the issue of whether Apple will again take the opportunity to tap the debt markets at the ultra-low rate it can command for the combined due reasons of sheers size of its cash reserve and of course, the lowest borrowing costs in modern history.

The circumstances surrounding the prior time it tapped bond markets just over a year ago have not changed: it cannot re-domicile most of the cash it has in reserve overseas without incurring the punitive US taxation it has so cunningly avoided, like many other large US corporations. Therefore, Apple can only get around its ‘cash problem’, if required by borrowing.

As suspected, Apple has not been immune to the re-emergence of a new high-value dollar era.

Still, I think the potential negative effect of this “clear headwind”, to use Apple CFO Luca Maestri’s words, has effectively been subsumed and even neutralized to a degree by the strength of the top and bottom line and net cash position, not to mention that Apple’s forecast range for Q2 revenues is $52bn-$55bn.

I think there will be few analysts who will contemplate the lower end at this stage.

There were no clear updates on Apple Watch (apart from that it will start shipping in April) and Apple Pay (apart from that it got off to a good “first inning”).

These are minor negatives.

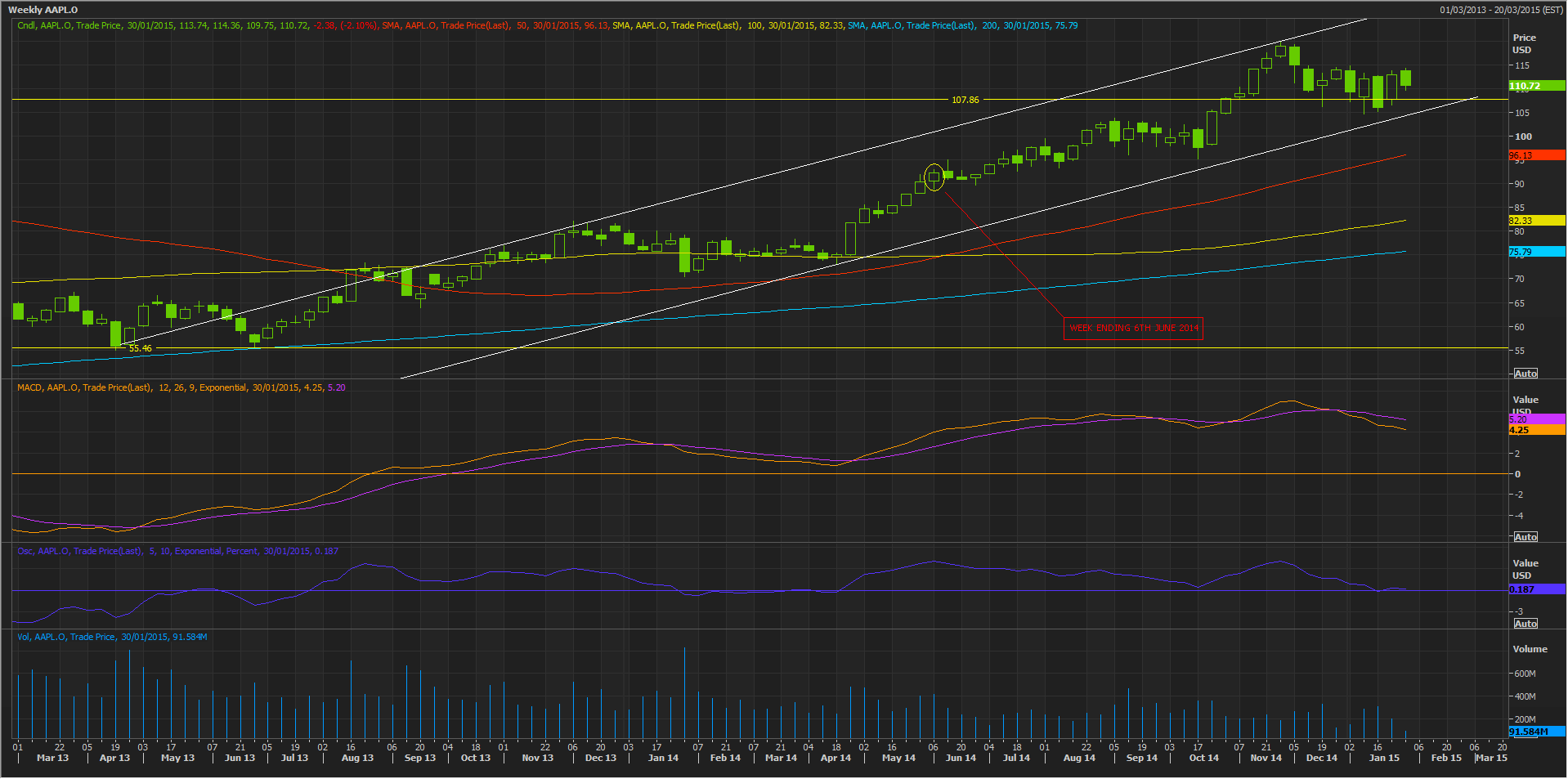

Overall, there was nothing in Apple’s update tonight in my view to prevent the inherent bullishness of the APPL’s trajectory over the last several weeks from being realised.

I expect the stock to quickly gravitate back to the upper bound of the rising trend channel it’s travelled in since early March 2013 (adjusted for the split in June 2014). The first target should be no lower than $116.

The stock added 6% in the US ‘after-hours’ session overnight following its results. It also bodes well that its Frankfurt listed stock is trading 5% higher as this article goes online.

The late-night revival of the stock was all the more telling given that it closed in the main session down more than 3% and down a net 2% for the month.