Apple s Q1 has fair chance of turning out sweet

Apple’s quarterly report coming out shortly, will, as always, be among the highlights of the financial market year, but tonight may be one of the […]

Apple’s quarterly report coming out shortly, will, as always, be among the highlights of the financial market year, but tonight may be one of the […]

Apple’s quarterly report coming out shortly, will, as always, be among the highlights of the financial market year, but tonight may be one of the rare occasions when investors focus less on the earnings and more on outlook.

That’s because after the $582.6bn group in January released one of its worst-received quarterly updates for at least a decade—including forecasting a first quarterly sales drop in 13 years—investors have had time to secure the worst possible outcome in their minds.

Even so, Wall St. consensus for Q2 has been anchored close to guidance emitted from the Cupertino, California spaceship since January, with forecasts drifting just 0.9% lower over the last 30 days, according to Thomson Reuters.

ARTIST’S IMPRESSION OF APPLE CAMPUS II, UNDER CONSTRUCTION IN CUPERTINO CALIFORNIA, COURTESY CUPERTINO CITY COUNCIL

Furthermore, the data provider’s best ‘weighted average’ calls (weighted in terms of reliability) have barely budged within an even narrower range.

A complete set of those forecasts:

Expectation for the group’s biggest revenue generator, the iPhone, are as always just as important, and the first-ever year-on-year decline in quarterly handset sales is still widely expected.

(The newest iPhone SE was released only in the closing days of March, Apple’s quarter end.)

Consensus for Q2 handset sales has settled at 50 million compared to 74 million in Q1 and 61 million in Q2 2015.

Given unmistakeably declining handset sales, a beat now looks less probable, despite the group’s recent history of numerous positive surprises.

Persistent, albeit uncorroborated, reports over the last few weeks that key parts suppliers were notified by their client that it planned to reduce iPhone production in April-June, back the view that this really will be a fallow quarter for iPhones.

Japan’s Nikkei News, also reported earlier this month that Apple had lowered production for the January-March quarter by about 30% from a year earlier, and that it was not planning to make enough of iPhone SEs to offset a slump in the flagship series.

However, despite these unpromising signals, Apple shares have retained a good 12.5% of gains following the 21% rise off almost two-year lows of January. (The stock remained 20% lower over a year.)

Late on Tuesday, options trading patterns suggested weak demand for bearish punts, judging by prices for such options trading more cheaply than in 85% of sessions over the last year.

Data reported by Reuters this evening also puts the stock’s 30-day at-the-money implied volatility, a gauge of risk of large stock moves at 28.4%, the lowest pre-earnings for six quarters.

Options positioning together with relatively a contained pullback in the underlying stock were among signs reflecting optimism in the market that even if the group fails to pull a handset or revenue rabbit out of its hat tonight, it might at least provide better than expected revenue guidance for later 2016 quarters.

To do so, it would need to raise expectations for Q3 up from the $49.95bn Wall St. expects.

Traders and investors are also eyeing pay-outs.

Dividend forecasts were already suggesting a payment a few cents above Apple’s planned quarterly 47 cents a share dividend.

Some investors also see scope for an increase of Apple’s stock buyback plan, despite recent high-profile criticisms of the total cost of around $87bn between September 2013 and end 2015, averaging $115 a share.

Should the additional hopes outlined above turn to have been forlorn, Apple shares, which have already been in bad shape for coming up to a year, would have scope for further nasty moves.

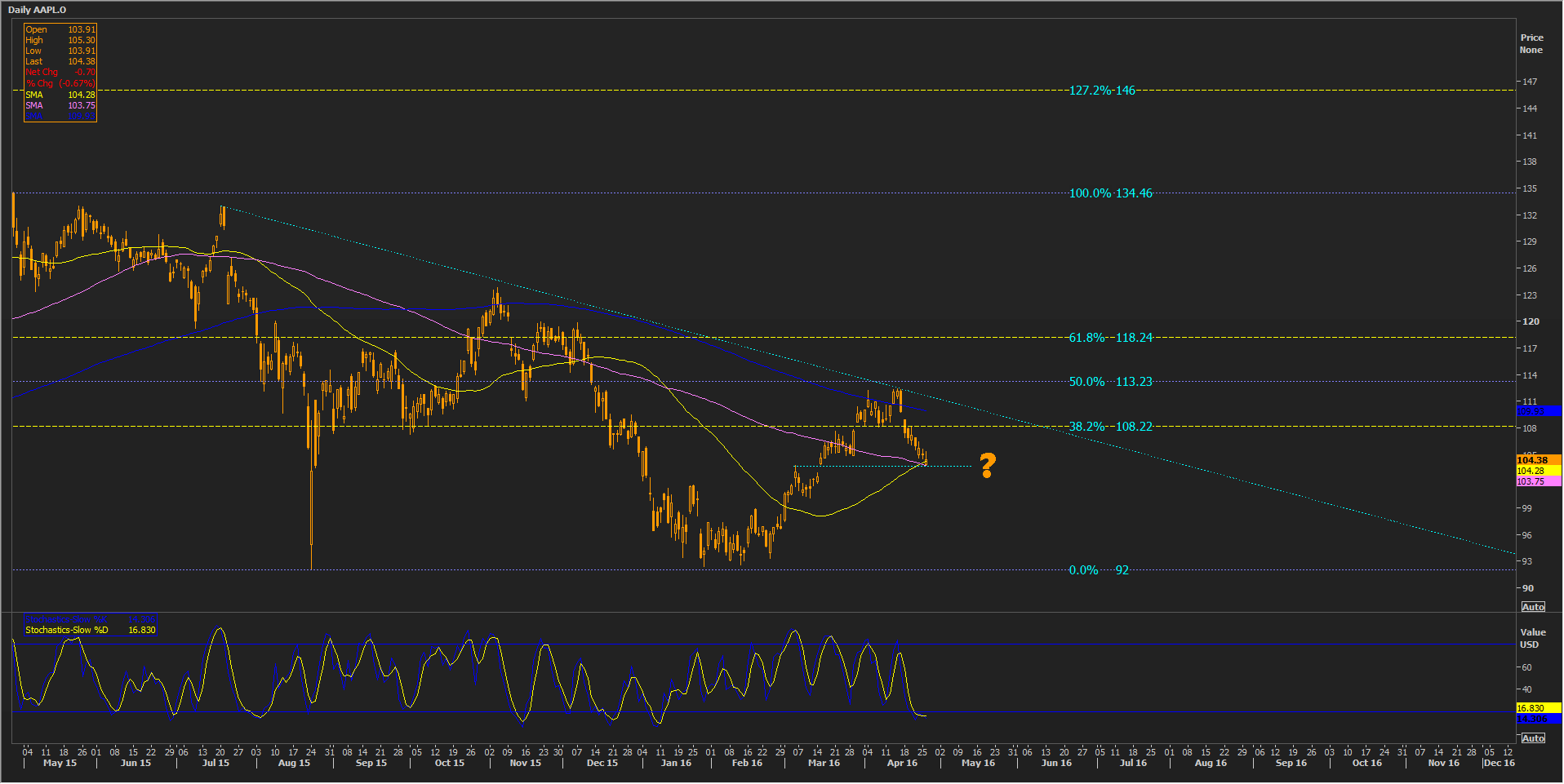

Please click image to enlarge

Trade below the widely watched 200-day moving average (blue line) is a pivotal weakness for any stock, and Apple’s has not sustainably surpassed the threshold since August.

As well, the beginnings of a descending trend can be seen, following three failures since AAPL’s record highs reached a year ago almost to the day.

Whilst shorter-term trends in confluence beneath the current price may assist, attempts to trace a clear line of support from former resistance in March doesn’t look favoured due to the well-known volatility of this stock.

Apple tends to slice through barriers that are typically strong, rather too easily (e.g., see 38.2% of decline from all time high).

If the stock remains true to that pattern in the near term, that would probably raise the prospect of a return to lows mentioned earlier, at least.

If these lows are seen, Apple’s highly significant and important 200-week moving average, last crossed about seven years ago could again come into play.

A well-received set of figures would need to fuel sufficient momentum to propel AAPL back over the 38.2% Fibonacci mentioned earlier, and definitely negate the potential downtrend before surpassing $113 highs for the year so far, in order to signal stronger gains in the reasonably near term.

This post will be updated after Apple’s earnings have been released.