October 21, 2019 1:20 AM

The U.S. dollar index, the DXY is on course for its biggest monthly fall since January 2018. Hopes of an end to Brexit, the U.S. – China trade truce and an expectation that the Federal Reserve will cut rates again next week have all played a part in undermining support for the U.S. dollar.

Factors closer to home have also contributed to the revival of Antipodean FX pairs the AUDUSD and the NZDUSD.

Our short-term bullish view of the AUDUSD has been in place since early October. It was aided last week by a better than expected Australian employment report and upbeat comments from RBA Governor Lowe during a speech to the IMF that included the economy is “gradually improving” and that the prospect of negative rates in Australia is “extremely unlikely.” The latter goes against the view of many prominent economists who expect the RBA to use unconventional monetary policy to support the Australian economy next year.

In New Zealand, last week’s Q3 Consumer Price Index (CPI) data has provided some support for the beleaguered NZDUSD. Although the headline rate fell further to 1.5% y/y, the 0.7% rise in Q3 and the larger than expected rise in domestic (non-tradable) inflation to 3.2%, driven by housing-related price gains, were both stronger than expected.

The technical picture also supports the subtle shift in the macro narrative for the NZD vs the U.S. dollar.

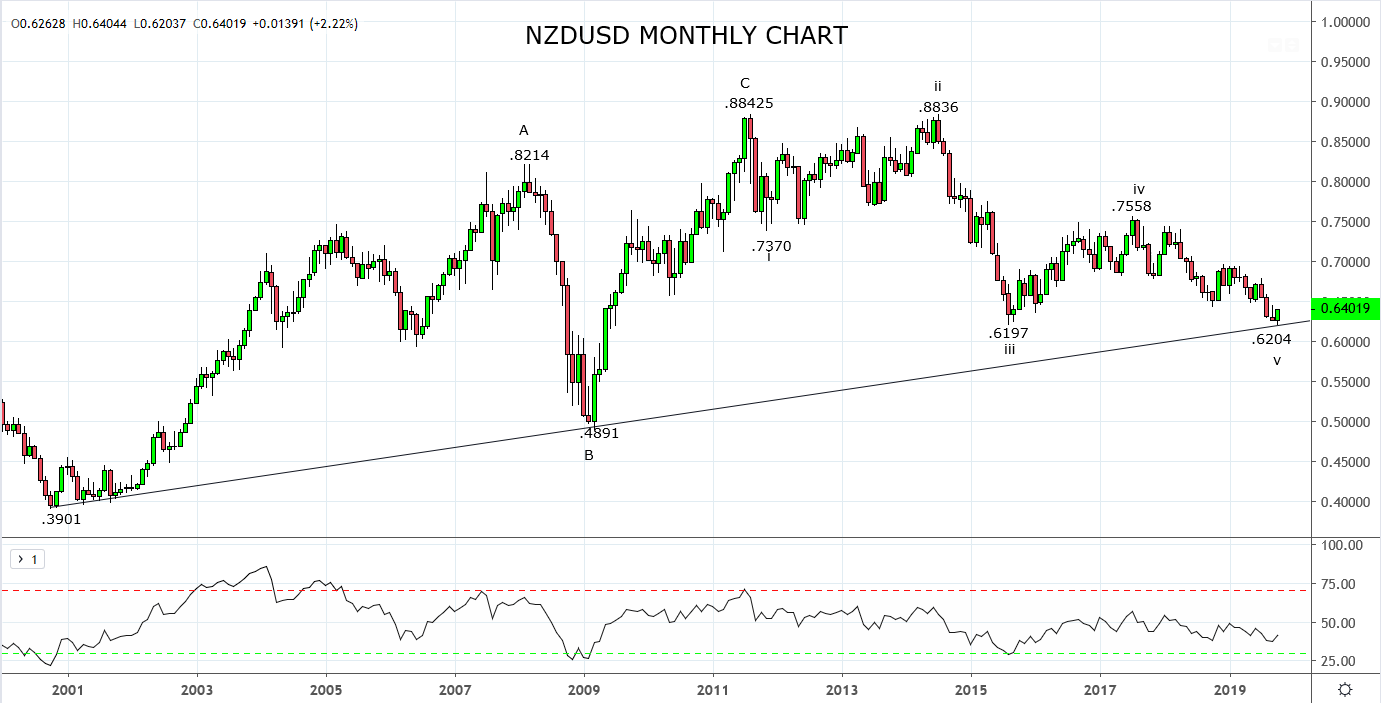

The monthly chart immediately below confirms the recent .6204 low was made in the vicinity of long-term uptrend support coming from the .3901 low from October 2000. It was also in the area of horizontal support from the August 2015, .6197 low.

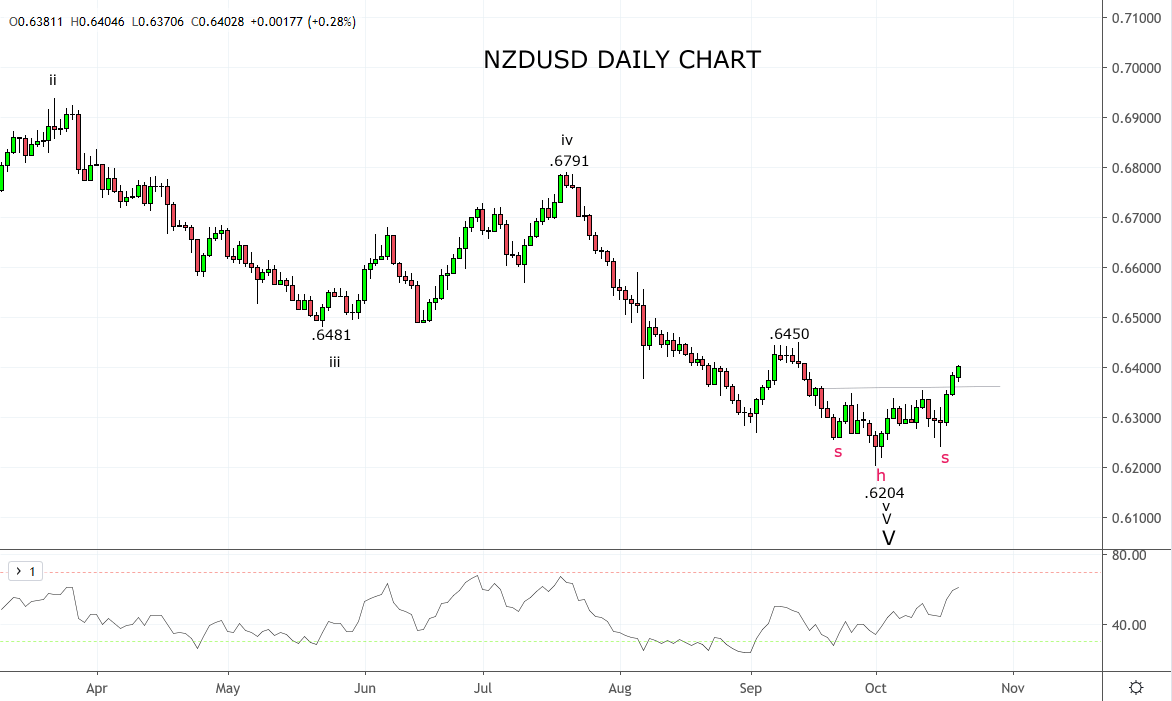

The daily chart below reveals an inverted head and shoulders bottoming pattern, bullish divergence via the RSI and a possible Elliott Wave, 5th Wave low in place at .6204.

In summary, after breaking above the neckline of the inverted head and shoulders .6355/65 area, the NZD is well-positioned to make further upside progress against the U.S. dollar. Dips should be well supported back to .6370/60ish and the initial upside target for the NZDUSD is the .6450 high from September followed by the confluence of resistance .6480/.6500 that includes the inverted head and shoulders target.

Source Tradingview. The figures stated areas of the 21st of October 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Disclaimer

TECH-FX TRADING PTY LTD (ACN 617 797 645) is an Authorised Representative (001255203) of JB Alpha Ltd (ABN 76 131 376 415) which holds an Australian Financial Services Licence (AFSL no. 327075)

Trading foreign exchange, futures and CFDs on margin carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange, futures or CFDs you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss in excess of your deposited funds and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange, futures and CFD trading, and seek advice from an independent financial advisor if you have any doubts. It is important to note that past performance is not a reliable indicator of future performance.

Any advice provided is general advice only. It is important to note that:

- The advice has been prepared without taking into account the client’s objectives, financial situation or needs.

- The client should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation or needs, before following the advice.

- If the advice relates to the acquisition or possible acquisition of a particular financial product, the client should obtain a copy of, and consider, the PDS for that product before making any decision.

Latest market news

Yesterday 10:40 PM

Yesterday 04:00 PM

Latest Forex articles

Yesterday 11:30 AM

Yesterday 03:42 AM