There was a sense of calm in the markets, but again without any fundamental news to suggest this is perhaps the bottom. Global equity indices and US futures continued their recovery after the comeback on Wall Street the day before. But as we have seen time and time again, stocks have struggled to sustain any recovery attempts as traders have been quick to take profit on rebounds amid a bearish macro back drop – rising interest rates, low growth and high inflation. As I mentioned on Thursday, when the Nasdaq was some 30% off the record highs, there was good a chance for a bear market rebound, especially as yields have come down a tad in recent trade. This may be that bounce I was looking for. Whether this will turn out to be just a small bounce or a sizeable one remains to be seen. But remember that we are now in a bear market and rallies tend to get sold into more often than dips being bought.

Just take a look how much cryptos have suffered and there is no reason why equities cannot fall further. Stagflation concerns are mounting, and monetary conditions may have to tighten a lot further to bring price pressures lower. Though Powell has reiterated that 75-bps hikes are not a base case, the fact that both PPI and CPI eased less than expected suggests the Fed will not hit the pause button any time soon.

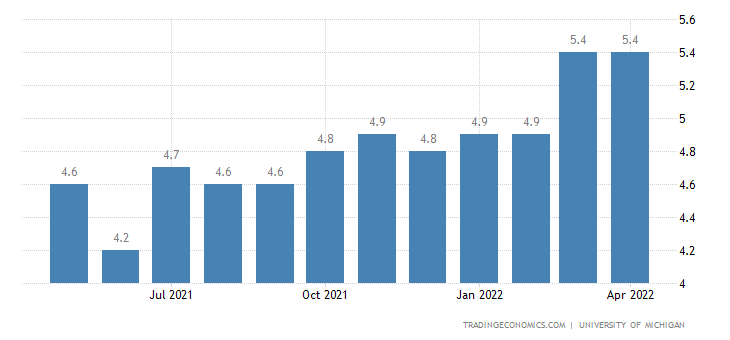

Consumer inflation expectations

The latest measure of US inflation – the University of Michigan’s 1-Year Inflation Expectations index – will be release later and it will be interesting to see if respondents report even higher price projections than they did last month, which was 5.4% - a 40-year high:

Expectations of future inflation can manifest into real inflation, as workers will push for higher wages when they believe prices will rise. So, until we see the trend turn downwards for consumer inflation expectations, it is likely risk appetite will remain low.

Looking ahead to next week

In the week ahead, we will have Chinese retail sales and industrial production on Monday, US retail sales on Tuesday and UK CPI on Wednesday, among the week’s macro highlights. The recent lockdowns in China means economic activity has slowed down sharply and we will find out the extent of it with these macro pointers. If we get weak numbers, then expect renewed weakness in risk assets as investor worries about a Chinese slowdown is revived. Globally, consumers are feeling the pinch with surging inflation. We will get a picture of how bad things really are at the world’s biggest economies. In the UK, meanwhile, inflation has climbed to a whopping 7.0% year-over-year in March, but there is hope that price pressures will come back down as the economy slows and due to base effects. Still, concerns over stagflation are likely to keep the pound and UK stocks under pressure for a while longer.

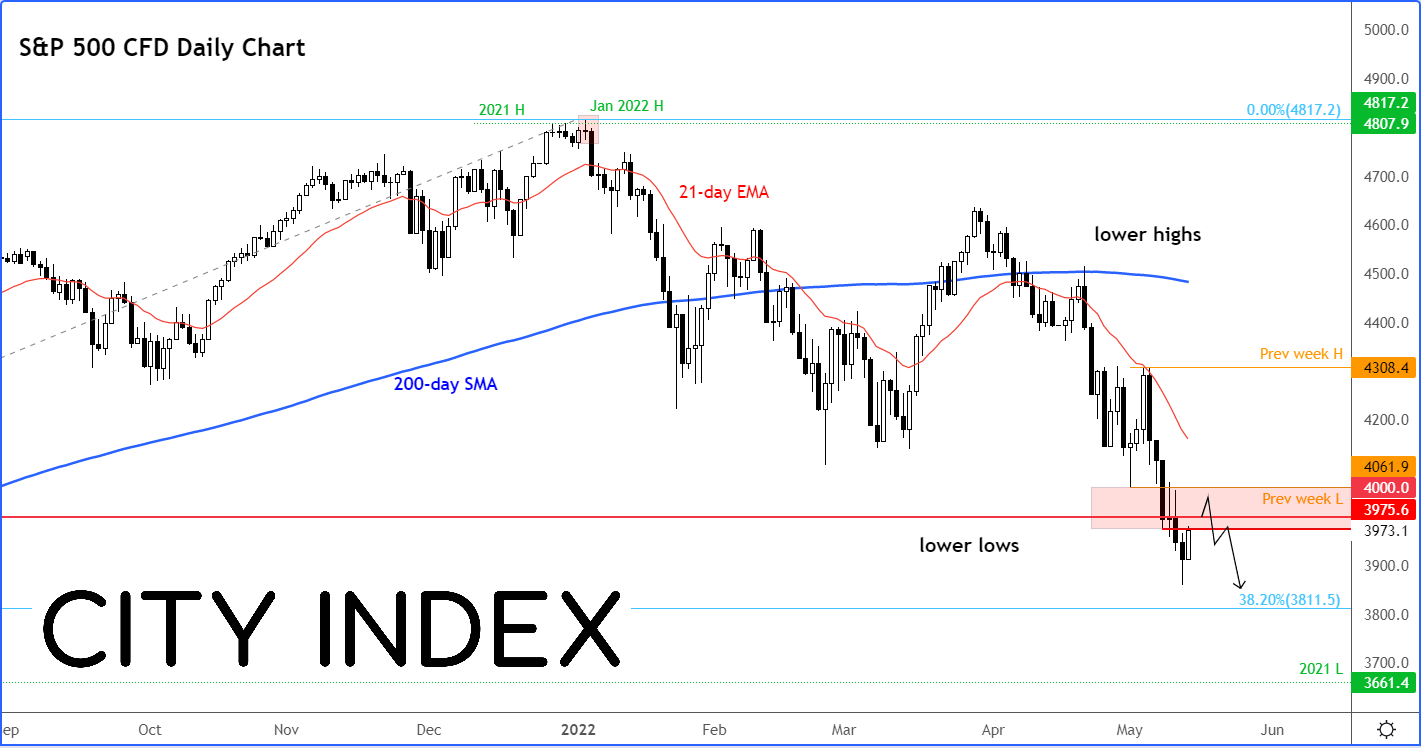

S&P bounces but faces key resistance

The S&P 500 is testing the bottom end of key resistance range between 3975 to 4061, shaded in red, where it had previously found some mild support. Unless that area is now reclaimed, the risks remain skewed to the downside, towards the long-term 38.2% Fibonacci retracement level (derived from the entire upswing from March 2020 low)

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 08:33 AM

Latest Stocks articles

Yesterday 11:00 AM

March 21, 2024 04:05 AM

March 7, 2024 05:03 AM

February 7, 2024 05:52 PM