Another Prime Minister resigns New Zealand Potential downside pressure on the Kiwi

Its seems that 2016 will go down as a year of political uncertainty as we have witnessed Brexit, the rise of populism in Europe (Italians […]

Its seems that 2016 will go down as a year of political uncertainty as we have witnessed Brexit, the rise of populism in Europe (Italians […]

Its seems that 2016 will go down as a year of political uncertainty as we have witnessed Brexit, the rise of populism in Europe (Italians rejection of constitutional reforms) and U.S. (the victory of President-elect Donald Trump).

Today in the Asia-Pacific region, the New Zealand Prime Minister John Key has announced his sudden resignation and also stepping down as the leader of the incumbent National Party. John Key has now pushed for his deputy, Bill English, also the current Finance Minister to be his successor to lead the National Party into the next general election in 2017.

Given that we are only a year away from the next general election in New Zealand, the sudden resignation of John Key is likely to create a short-term uncertainty in the direction of regulations which can lead business confidence to dip. In fact, the business climate in New Zealand is already lukewarm as business confidence has continued to decline for three consecutive months since September 2016 with the latest November 2016 reading at 20.5.

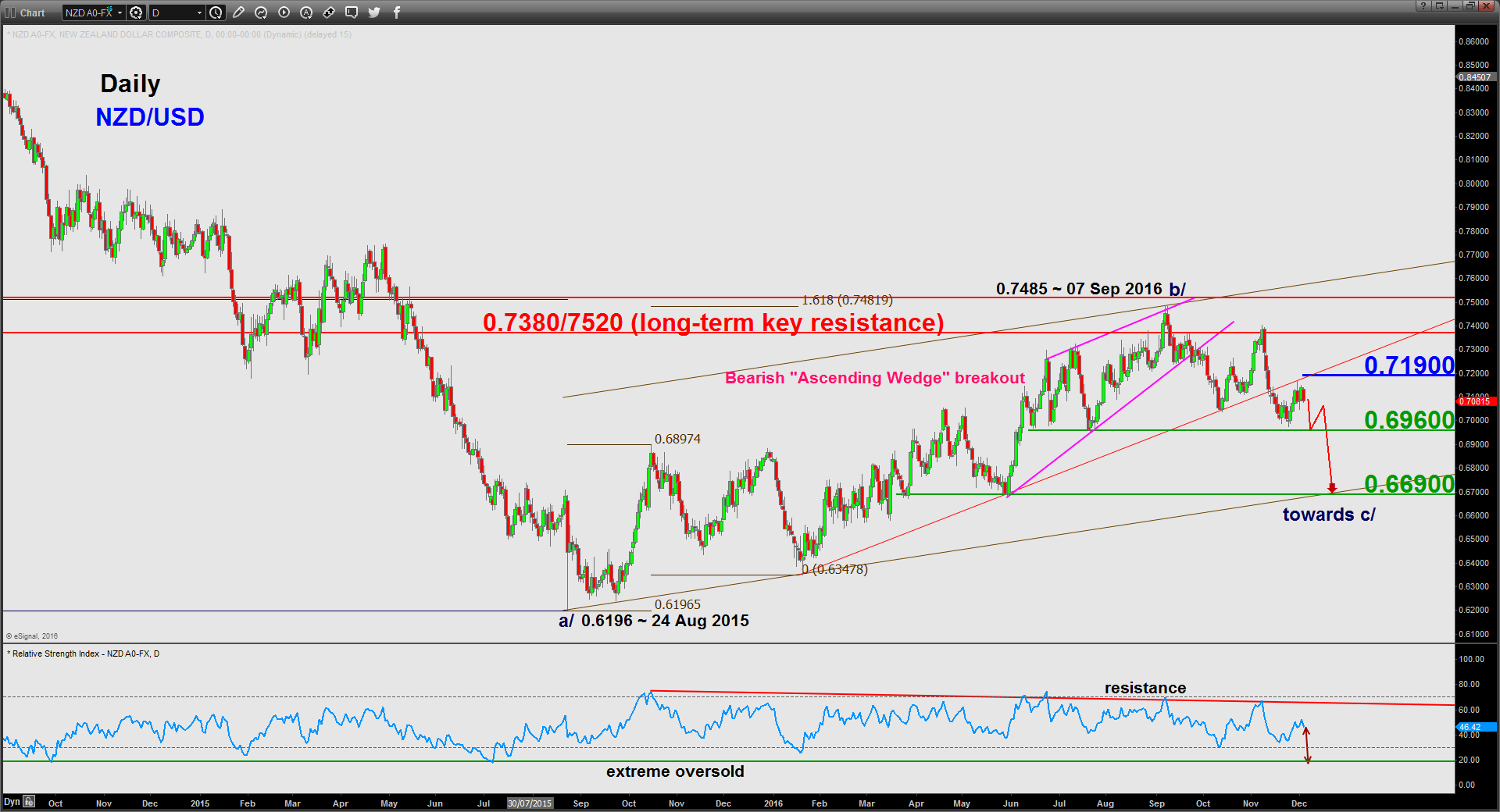

The NZD/USD has continued to trade in a sideways range environment since its August 2015 low of 0.6196 and one of the fundamental reasons is the higher yield differential in interest rates between the Kiwi and the USD where the New Zealand benchmark policy interest rate is still above 1%, at 1.75% after the recent 25bps cut by its central bank, RBNZ versus sub-zero and negative interest rates seen in the other majors such as the Euro, GBP and JPY.

However, these near-term uncertainties coupled pre-election jitters can create a negative feedback loop into the Kiwi dollar. From a technical analysis, the NZD/USD (see chart below) has started to crack after the recent breakdown from its bearish “Ascending Wedge” formation right at the top of the ascending range in place since the August 2015 low. In addition, the recent rebound from the 0.6970 low of 24 November 2016 has stalled right at a pull-back resistance from 20 January 2016 low. Therefore, as long as the 0.7190 medium-term pivotal resistance holds, the NZD/USD is likely to see further potential downside movement in the medium-term (1 to 3 weeks) towards 0.6960 before targeting the lower boundary (support) of the ascending range at 0.6690.

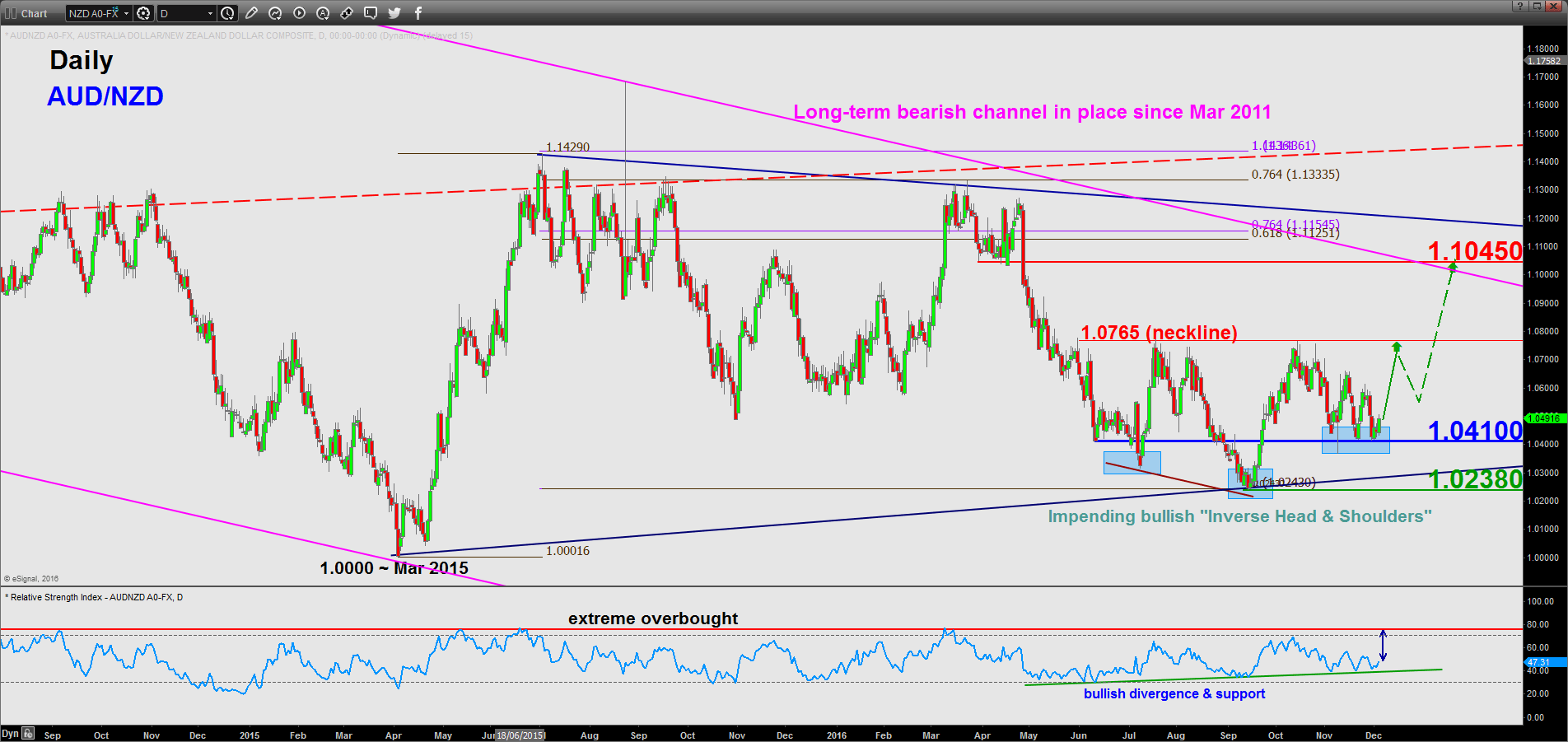

Even in the AUD/NZD cross pair (see chart below), impending negative technical elements have also started to emerge in the Kiwi. The AUD/NZD has started to trace out a bullish “Inverse Head & Shoulders” formation right at the lower boundary (support) of a longer-term “Symmetrical Triangle” range configuration in place since March 2015 parity low. Thus, as long as the 1.0410 medium-term pivotal support holds, the AUD/NZD is likely to see a potential upside movement in the medium-term (1 to 3 weeks) to stage an assault on the 1.0765 neckline resistance of the aforementioned “Inverse Head & Shoulders”. Only a clear break above 1.0765 may see a further rally to target the next resistance at 1.1045 (the upper boundary of the “Symmetrical Triangle” & the long-term bearish channel in place since March 2011).

(Click to enlarge charts)

(Click to enlarge charts)

Charts are from eSignal