September 12, 2019 12:19 PM

After ECB Rate Decision, All Eyes on Fed

The ECB had cut rates 10 bps, as the market was expecting. However, as we noted in our ECB Recap, the ECB also announced that they would introduce OPEN- ENDED QE at a rate of EUR 20bln/month. The ECB sent a message to the market that there is no targeted end date to QE.

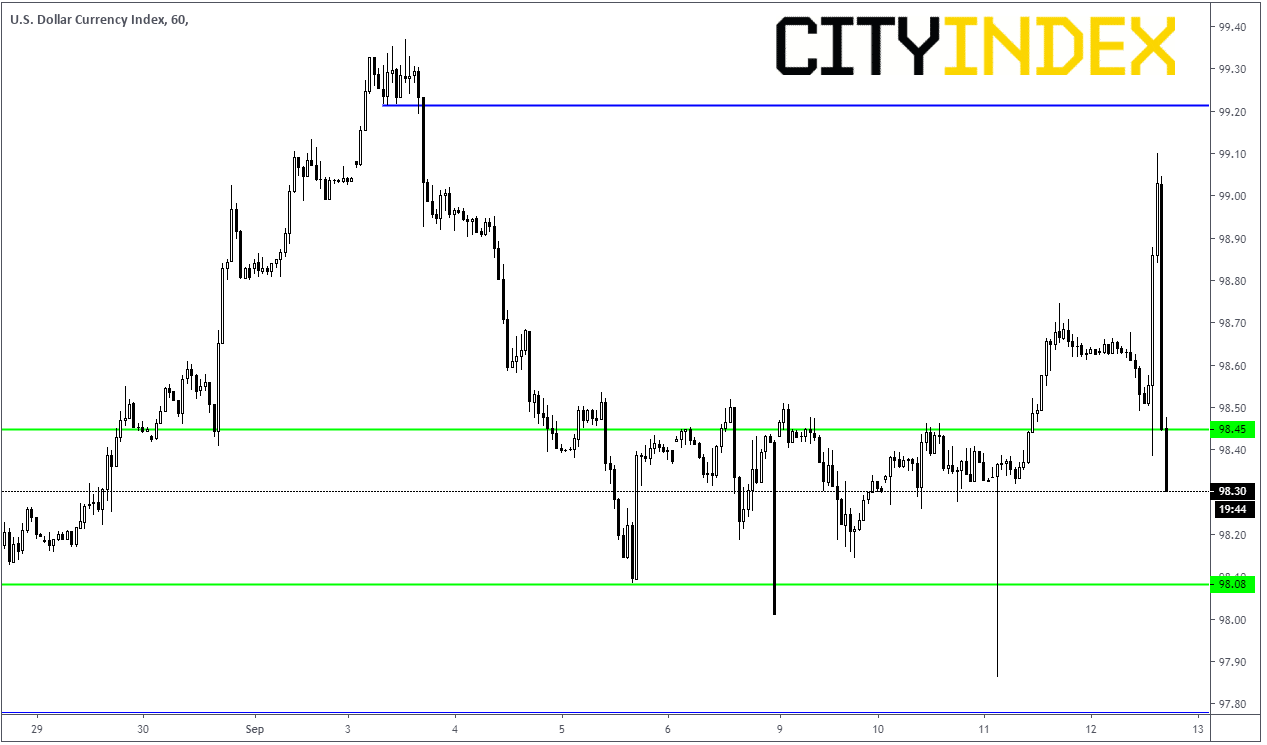

The market took the news as dovish, as EUR/USD dropped 100 pips to previous lows from September 3rd, while DXY rose 50 pips, near towards resistance from the same date.

Souce: Tradingview, City Index

Source: Tradingvew, City Index

However a half hour later, US President Trump came out a message of his own:

“European Central Bank, acting quickly, Cuts Rates 10 Basis Points. They are trying, and succeeding, in depreciating the Euro against the VERY strong Dollar, hurting U.S. exports.... And the Fed sits, and sits, and sits. They get paid to borrow money, while we are paying interest!”

As you can see from the charts above, EUR/USD and DXY quickly reversed course and surpassed levels from before the ECB announcement! Why? Because now all eyes are on the FOMC meeting next week on September 18. The market is currently pricing in a 100% chance of a rate cut next week, a majority of which is expecting a 25bps cut.

Powell insists the Fed is an independent government body (as it should be). But one needs to consider…will the FOMC feel the pressure from President Trump to cut more than it really wants to (even after he called Powell a “bonehead’ yesterday)?

Latest market news

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest EUR articles

April 13, 2024 08:00 PM

March 25, 2024 02:55 AM

January 22, 2024 04:19 AM

January 18, 2024 04:46 AM