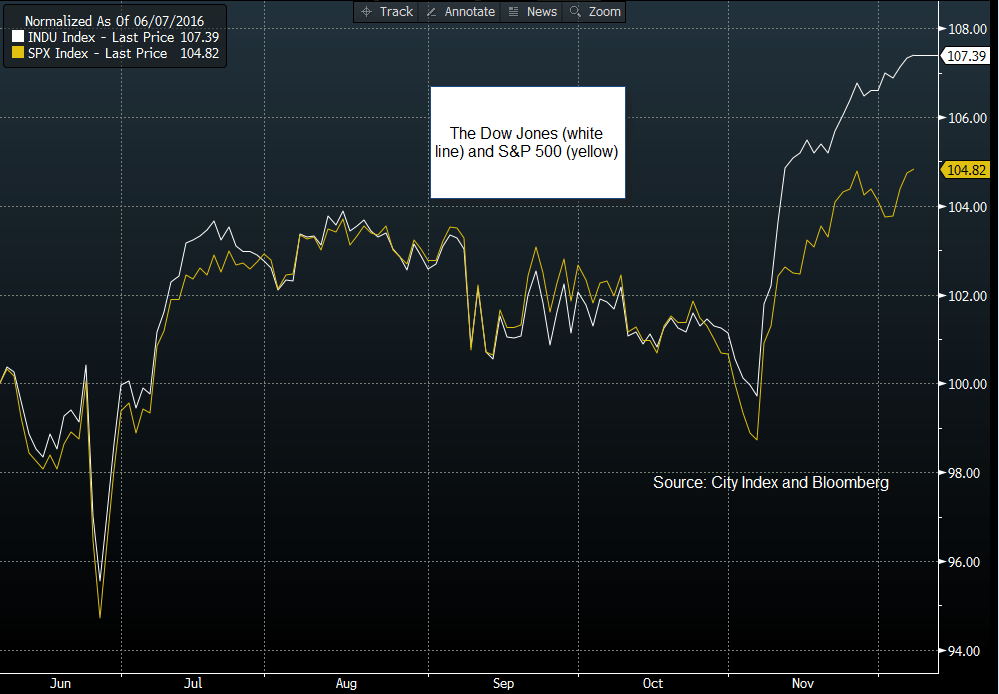

A month of Trump Dow leaves S amp P 500 in its shadow

An interesting development has taken place since the US Presidential election, the Dow has outperformed the S&P 500, see figure 1. This is not really […]

An interesting development has taken place since the US Presidential election, the Dow has outperformed the S&P 500, see figure 1. This is not really […]

An interesting development has taken place since the US Presidential election, the Dow has outperformed the S&P 500, see figure 1. This is not really surprising, the industrial and financial sectors make up a combined 37% of the Dow Jones, compared to 25% for the S&P 500. Since the election of Donald Trump, these sectors have powered ahead, for example the Dow Jones banking index has retraced 61.8% of its total decline since the financial crisis.

Stocks on steroids: thank Trump

Trump is acting like a steroid for some US stocks. The prospect of huge infrastructure spending and fiscal largesse during his Presidency is well and truly getting priced into US industrial stocks. For example, Caterpillar has hit a 2-year high and jumped sharply since November’s Presidential election. US banks are also benefitting from the Trump effect, the prospect of a reversal of some Dodd Frank legislation during Trump’s term as President has increased the attractiveness of banks including Bank of America, its share price has surged to a 8-year high in the past month.

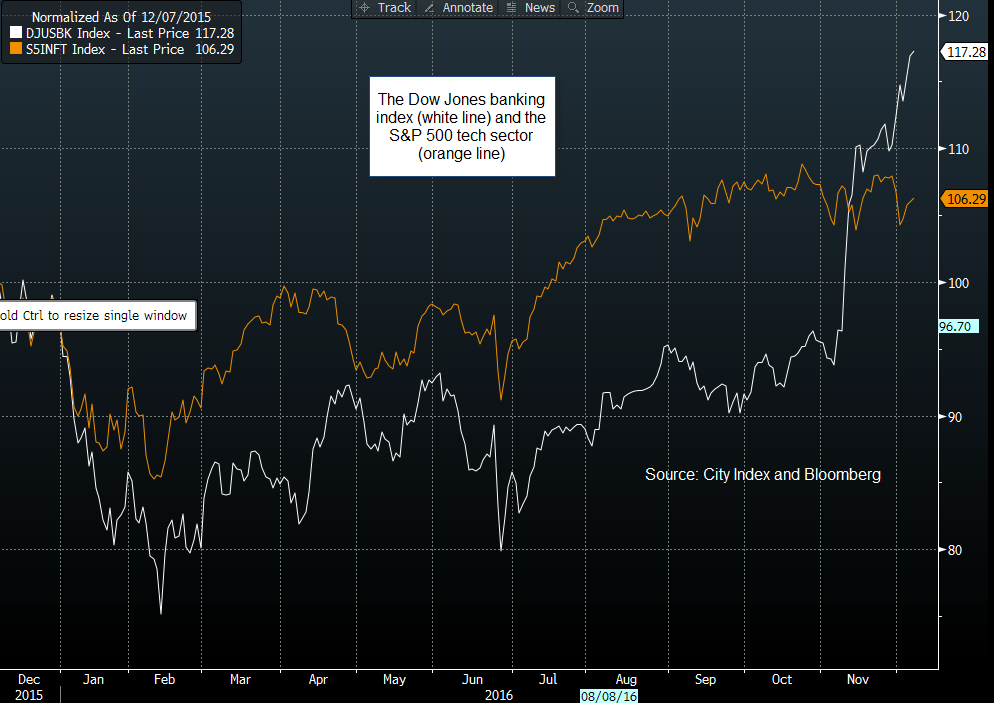

The poison Apple takes a bite out of the S&P 500

This is all good news for the Dow, but why isn’t the US’s other major stock index able to match these highs? It’s all down to the technology sector. Figure 2 (attached) shows the Dow Jones banking index and the S&P 500 technology index. As you can see in figure 2, the Dow’s banks are trumping the S&P’s tech stars as life gets more difficult for companies like Apple. Unfortunately for the S&P 500, the tech sector makes up 20% of the index. Unlike banks and industrials that could benefit from a Trump Presidency, the tech sector might not be so lucky. If Trump imposes protectionist policies and trade tariffs, then heavy exporters like Apple etc. could struggle over the next four years.

But where will stocks go next?

The Dow banking index looks strong, the 61.8% Fib level of resistance is key, if US banks become ‘unburdened’ by the Dodd-Frank rule, as some think, then 2017 could be the year when we see bank stocks make a stab at their pre financial crisis highs. This is a big call, but this Trump trade has muscle and there are plenty of people looking towards a more profitable future for banking stocks in the US, less so in Europe.

Silicon Valley’s hipsters not so cool under Trump

The tech sector in the S&P 500 could be one sector to avoid in 2017. Not only are big companies like Apple struggling to come up with new products and new revenue opportunities, but uncertainties around Trump’s trade policies could keep tech stocks in the shadows next year.

Overall, the stock market rally looks good, for now. We think that certain sectors will outperform, notably banks and industrials, which makes the Dow more attractive than the S&P 500. Unless we see a shock move higher in bond yields – to 3% or above in US 10-year Treasury yields – then this rally could have legs, at least into Q1 next year.

Figure 1:

Source: Bloomberg and City Index

Figure 2:

Source: Bloomberg and City Index