US Futures consolidating, watch FB, MSFT, TSLA, MCD, TWTR, QCOM

The S&P 500 Futures are slightly dipping after they posted a powerful rally of over 2% yesterday, as investors were encouraged by Gilead Sciences' promising trial test results for its drug Remdesivir in treating coronavirus patients. Sentiment was also boosted by the Federal Reserve's pledge to support the economy.

Later today, the U.S. Labor Department will report initial jobless claims for the week ended April 25 (3.500 million expected). March Personal Income (-1.5% on month expected), Personal Spending (-5.0% on month expected), and the Market News International's Chicago Business Barometer for April (37.7 expected) will also be reported. In Canada, February GDP is expected at +0.1% on month and March PPI is expected at -3.0% on year.

European indices are consolidating after a positive open. The European Central Bank kept its main benchmark interest rate at 0%, as expected. "The Governing Council decided to reduce the interest rate on TLTRO III operations during the period from June 2020 to June 2021 to 50 basis points below the average interest rate on the Eurosystem’s main refinancing operations prevailing over the same period."

Later today, the U.S. Labor Department will report initial jobless claims for the week ended April 25 (3.500 million expected). March Personal Income (-1.5% on month expected), Personal Spending (-5.0% on month expected), and the Market News International's Chicago Business Barometer for April (37.7 expected) will also be reported. In Canada, February GDP is expected at +0.1% on month and March PPI is expected at -3.0% on year.

European indices are consolidating after a positive open. The European Central Bank kept its main benchmark interest rate at 0%, as expected. "The Governing Council decided to reduce the interest rate on TLTRO III operations during the period from June 2020 to June 2021 to 50 basis points below the average interest rate on the Eurosystem’s main refinancing operations prevailing over the same period."

The European Commission has posted 1Q GDP at -3.3% (vs -3.1% on year expected) and March jobless rate at 7.4% (vs 7.7% expected). The German Federal Statistical Office has reported April jobless rate at 5.8% (vs 5.2% expected) and March retail sales at -5.6% (vs -7.3% on month expected). France's INSEE has released 1Q GDP at -5.8% (vs -3.6% on year expected) and April CPI at +0.4% on year (vs +0.1% expected).

Asian indices were strongly bullish. This morning, government data showed that Japan's industrial production fell 3.7% on month in March (-5.0% estimated), and retail sales declined 4.5% (as expected). China's Manufacturing PMI fell to 50.8 in April (51.0 expected) from 52.0 in March, while non-manufacturing PMI climbed to 53.2 (52.5 expected) from 52.3. Also, the Caixin China Manufacturing PMI dropped to 49.4 in April (50.5 expected) from 50.1 in March.

WTI Crude Oil Futures remain on the upside on a brighter outlook for demand following worldwide easing of coronavirus-induced restrictions. The U.S. Energy Information Administration reported that crude-oil stockpiles increased 9 million barrels last week, less than an addition of 11 million barrels expected. At the same time, U.S. Treasury Secretary Steven Mnuchin said the government could add millions of barrels of oil to its national reserves.

Gold rose 1.54 dollar (+0.09%) to 1714.94 dollars per ounce, slightly rebounding after the Fed decision.

The EUR/USD fell 3pips to 1.087, consolidating after the ECB announcement.

USD/CAD fell 12pips to 1.3869 on bouncing oil.

US Equity Snapshot

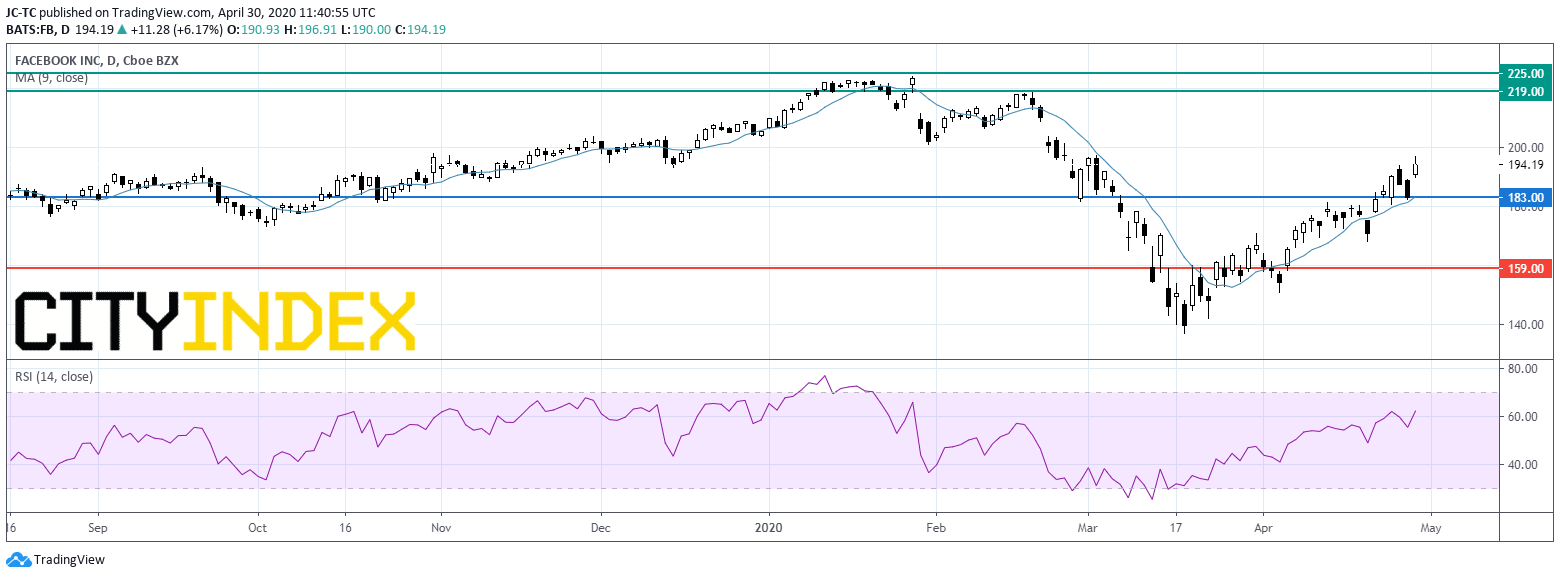

Facebook (FB), the largest online social network platform, surged in extended trading after announcing first quarter sales of 17.7 billion dollars, better than expected, up from 15.1 billion dollars a year earlier. Monthly active users increased 10% in March to 2.6 billion, above forecasts. EPS was down to 1.71 dollar from 1.89 dollar a year ago, in-line with estimates.

Microsoft (MSFT), the software development company, reported third quarter EPS of 1.40 dollar up from 1.14 dollar a year ago, on sales of 35.0 billion dollars, up from 30.6 billion dollars a year earlier. Both figures beat estimates.

Tesla (TSLA), the electric-vehicle maker, jumped after hours as the company posted first quarter adjusted EPS of 1.24 dollar while consensus anticipated a loss. Sales were up to 5.99 billion dollars from 4.5 billion dollars a year earlier.

McDonald's (MCD), the global fast-food restaurant chain, posted first quarter adjusted EPS down to 1.47 dollar, below estimates, from 1.72 dollar a year earlier. Same-restaurant sales were down 3.4%, matching forecasts.

Twitter (TWTR), the social network, is surging before hours after posting first quarter adjusted EPS of 0.11 dollar, above forecasts. Sales were up to 808 million dollars from 787 million dollars a year earlier.

QUALCOMM (QCOM), a maker of digital wireless communications equipment, unveiled second quarter adjusted EPS up to 0.88 dollar from 0.77 dollar a year ago, on sales up to 5.2 billion dollars from 4.9 billion dollars a year earlier. Both figures were better than expected.

Boeing's (BA), the aircraft manufacturer, credit rating was downgraded to "BBB-" from "BBB" at S&P Global Ratings, outlook "Stable". The rating agency stated: "Boeing Co.'s earnings and cash flow over the next few years are likely to be lower than we had previously expected due to the impact of the coronavirus on aircraft demand, with the pace of recovery in air travel still highly uncertain."

Exxon Mobil (XOM), a giant oil producer, has declared a second quarter dividend of 0.87 dollar per share, unchanged quarter on quarter. It is the first time since 13 years that the company freezes its dividend.

Tyson Foods (TSN), a food processing company, said it will temporarily pause operations at its Dakota City beef facility, one of the largest beef processing plant in the U.S., from May 1 to May 4 to complete a deep cleaning of the entire plant and screening process for plant team members for COVID-19.

Source : TradingVIEW, GAIN Capital

Latest market news

Today 08:15 AM

Today 05:45 AM

Latest Fed articles

April 22, 2024 04:33 PM

April 10, 2024 01:40 PM

April 4, 2024 02:13 PM

April 3, 2024 07:56 PM