U.S Futures consolidating - Watch SPGI, INFO, MRNA, GS

The S&P 500 Futures are mixed after they closed higher on Friday.

Later today, the Market News International will release Chicago PMI for November (59.2 expected). The National Association of Realtors will post October pending home sales (+1.0% on month expected). The Dallas Federal Reserve will post its Manufacturing Outlook Index for November (14.5 expected).

European indices have rebounded after a negative open. The Bank of England has released the number of mortgage approvals for October at 97,500 (vs 84,000 expected). The German Federal Statistical Office will post November CPI (-0.1% on year expected).

Asian indices all closed in the red. Japan's industrial production rose 3.8% on month in October (+2.2% expected), and retail sales grew 0.4% (+0.5% expected). China's official Manufacturing PMI rose to 52.1 in November (51.5 expected) from 51.4 in October and Non-manufacturing PMI climbed to 56.4 (56.0 expected) from 56.2.

WTI Crude Oil is on the downside. Over the weekend, OPEC+ ministers failed to reach an agreement on oil output decision in an informal online meeting, as the United Arab Emirates and Kazakhstan were opposed to delay a production increase in January, according to Bloomberg.

U.S indices closed up on Friday, lifted by Pharmaceuticals, Biotechnology & Life Sciences (+0.97%), Health Care Equipment & Services (+0.94%) and Semiconductors & Semiconductor Equipment (+0.79%) sectors.

Approximately 91% of stocks in the S&P 500 Index were trading above their 200-day moving average and 82% were trading above their 20-day moving average. The VIX Index fell 0.41pt (-1.93%) to 20.84.

On the U.S economic data front, no major economic data was released.

On Monday, Market News International's Chicago Business Barometer for November is expected to fall to 59.0 on month, from 61.1 in October. Finally, Pending Homes Sales for October are expected to rise 1.0% on month, compared to -2.2% in September.

Gold sets for its worst month in four years on equities rally while the U.S dollar hit a more than two-year low on stimulus bets.

Gold fell 15.55 dollars (-0.87%) to 1772.24 dollars.

The dollar index declined 0.19pt to 91.604.

U.S. Equity Snapshot

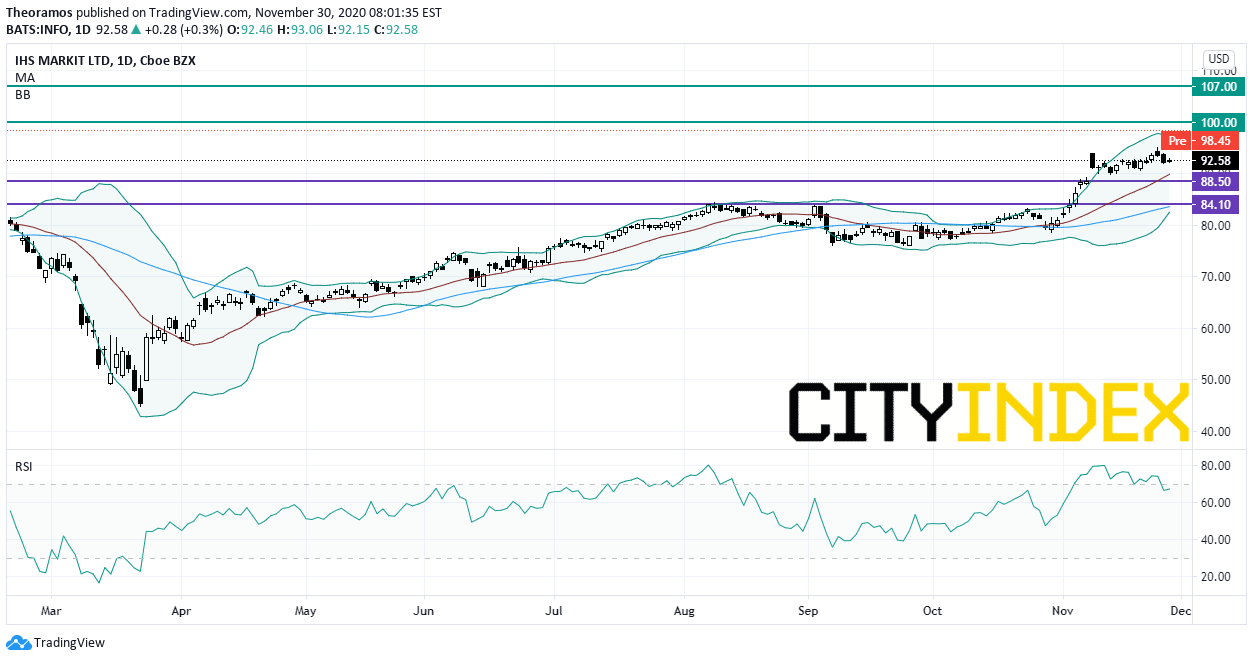

S&P Global (SPGI), the financial information services company, agreed to acquire peer IHS Markit (INFO), for about 44 billion dollars. S&P offers 0.2838 shares for each IHS Markit share, or 4 4.7% premium over November 27th, 2020, close.

Source: TradingView, GAIN Capital

Moderna (MRNA), the biotech, announced "that its vaccine efficacy against COVID-19 was 94.1%. The company plans to request today an Emergency Use Authorization (EUA) from the U.S. Food and Drug Administration (FDA) and conditional approval from the European Medicines Agency (EMA)."

Goldman Sachs (GS), the banking group, was downgraded to "underweight" from "equalweight" at Morgan Stanley.

JPMorgan (JPM) and Bank of America (BAC), the banking groups, were both downgraded to "underweight" from "overweight" at Morgan Stanley.

Apple (AAPL), the tech giant, was upgraded to "buy" from "hold" at Loop Capital.

Slack Technologies (WORK), the collaboration hub, was downgraded to "equalweight" from "overweight" at Barclays.

Later today, the Market News International will release Chicago PMI for November (59.2 expected). The National Association of Realtors will post October pending home sales (+1.0% on month expected). The Dallas Federal Reserve will post its Manufacturing Outlook Index for November (14.5 expected).

European indices have rebounded after a negative open. The Bank of England has released the number of mortgage approvals for October at 97,500 (vs 84,000 expected). The German Federal Statistical Office will post November CPI (-0.1% on year expected).

Asian indices all closed in the red. Japan's industrial production rose 3.8% on month in October (+2.2% expected), and retail sales grew 0.4% (+0.5% expected). China's official Manufacturing PMI rose to 52.1 in November (51.5 expected) from 51.4 in October and Non-manufacturing PMI climbed to 56.4 (56.0 expected) from 56.2.

WTI Crude Oil is on the downside. Over the weekend, OPEC+ ministers failed to reach an agreement on oil output decision in an informal online meeting, as the United Arab Emirates and Kazakhstan were opposed to delay a production increase in January, according to Bloomberg.

U.S indices closed up on Friday, lifted by Pharmaceuticals, Biotechnology & Life Sciences (+0.97%), Health Care Equipment & Services (+0.94%) and Semiconductors & Semiconductor Equipment (+0.79%) sectors.

Approximately 91% of stocks in the S&P 500 Index were trading above their 200-day moving average and 82% were trading above their 20-day moving average. The VIX Index fell 0.41pt (-1.93%) to 20.84.

On the U.S economic data front, no major economic data was released.

On Monday, Market News International's Chicago Business Barometer for November is expected to fall to 59.0 on month, from 61.1 in October. Finally, Pending Homes Sales for October are expected to rise 1.0% on month, compared to -2.2% in September.

Gold sets for its worst month in four years on equities rally while the U.S dollar hit a more than two-year low on stimulus bets.

Gold fell 15.55 dollars (-0.87%) to 1772.24 dollars.

The dollar index declined 0.19pt to 91.604.

U.S. Equity Snapshot

S&P Global (SPGI), the financial information services company, agreed to acquire peer IHS Markit (INFO), for about 44 billion dollars. S&P offers 0.2838 shares for each IHS Markit share, or 4 4.7% premium over November 27th, 2020, close.

Source: TradingView, GAIN Capital

Moderna (MRNA), the biotech, announced "that its vaccine efficacy against COVID-19 was 94.1%. The company plans to request today an Emergency Use Authorization (EUA) from the U.S. Food and Drug Administration (FDA) and conditional approval from the European Medicines Agency (EMA)."

Goldman Sachs (GS), the banking group, was downgraded to "underweight" from "equalweight" at Morgan Stanley.

JPMorgan (JPM) and Bank of America (BAC), the banking groups, were both downgraded to "underweight" from "overweight" at Morgan Stanley.

Apple (AAPL), the tech giant, was upgraded to "buy" from "hold" at Loop Capital.

Slack Technologies (WORK), the collaboration hub, was downgraded to "equalweight" from "overweight" at Barclays.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM