U.S Futures sliding - Watch DIS, MU, GOOGL, REGN, SBUX

The S&P 500 Futures remain under pressure after a first acrimonious presidential debate between Donald Trump and Joe Biden.

Later today, final readings of 2Q annualized GDP will be expected at -31.7% on quarter. The Automatic Data Processing (ADP) will post private jobs for September (+648,000 jobs expected). The Market News International will report Chicago PMI for September (52.0 expected). The National Association of Realtors will release August pending home sales (+3.2% on month expected).

European indices are on the downside. The German Federal Statistical Office has reported September jobless rate at 6.3% (vs 6.5% expected) and August retail sales at +3.1% (vs +0.4% on month expected). France's INSEE has posted CPI for September at +0.1% (vs +0.2% on year expected). The U.K. Office for National Statistics has released final readings of 2Q GDP at -19.8% (vs -20.4% on quarter expected). The Nationwide Building Society has posted its House Price Index for September at +0.9% (vs +0.5% on month expected).

Asian indices closed on a strong down move except the Hong Kong HSI which ended in the green. China's official Manufacturing PMI rose to a 6-month high of 51.5 in September (51.3 expected) from 51.0 in August and Non-manufacturing PMI climbed to the highest level since November 2013 at 55.9 (54.7 expected) from 55.2. On the other hand, China's Caixin Manufacturing PMI slipped to 53.0 in September (53.1 expected) from 53.1 in August. Japan's industrial production grew 1.7% on month in August (+1.4% expected) and retail sales rose 4.6% (+2.0% expected).

WTI Crude Oil futures remain bearish. The American Petroleum Institute (API) reported that U.S. crude-oil inventories fell 831,000 barrels in the week ending September 25. Later today, the U.S. Energy Information Administration (EIA) will release official crude oil inventories data for the same period.

Gold lost ground as the U.S dollar strengthens on COVID-19 fears

Gold fell 12.54 dollars (-0.66%) to 1885.54 dollars.

The dollar index rose 0.2pt to 94.091.

U.S. Equity Snapshot

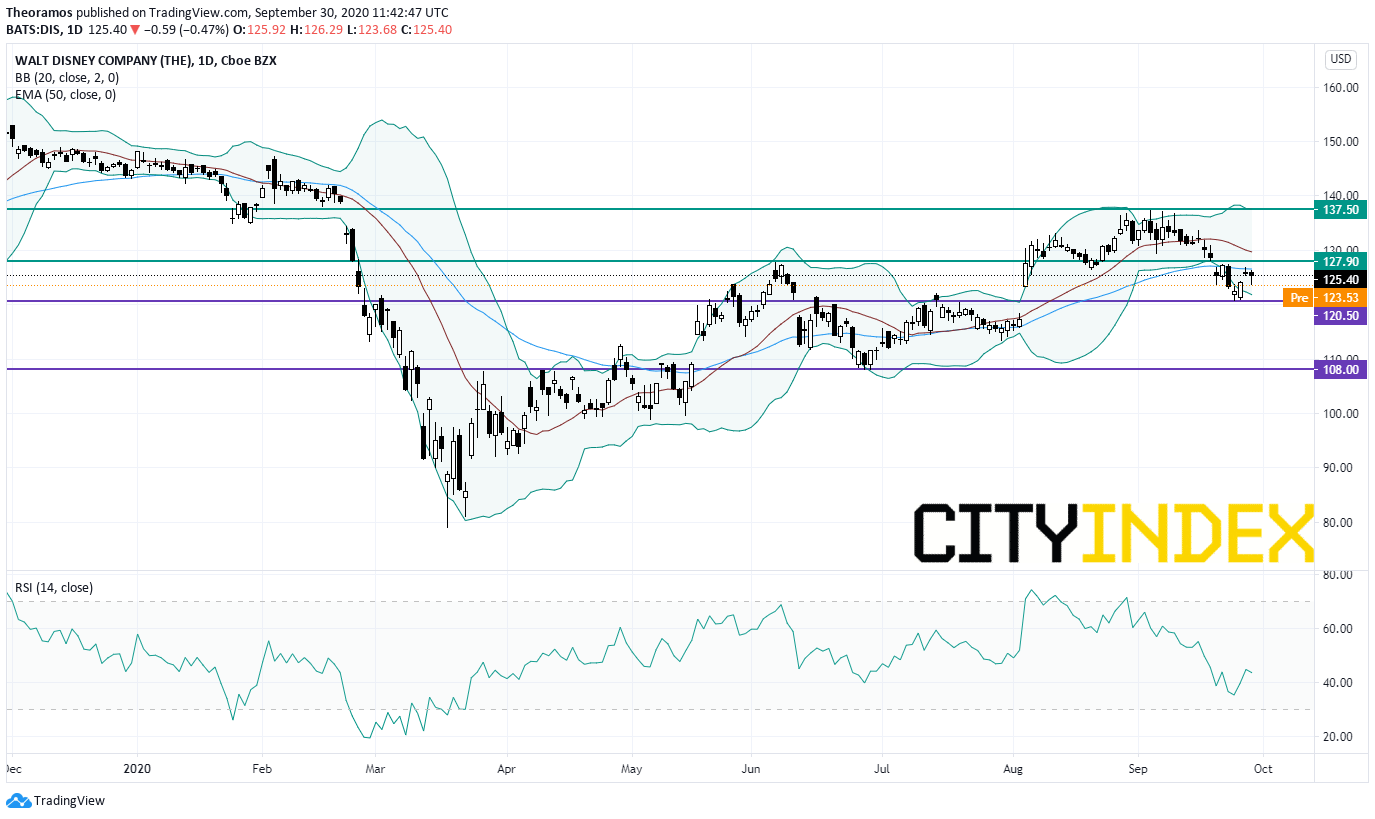

Walt Disney (DIS), the entertainment and media giant, plans to lay off 28,000 employees in its theme parks, amid COVID-19 restrictions.

Source: TradingView, GAIN Capital

Regeneron Pharmaceuticals (REGN), a biotech, announced "the first data from a descriptive analysis of a seamless Phase 1/2/3 trial of its investigational antibody cocktail REGN-COV2 showing it reduced viral load and the time to alleviate symptoms in non-hospitalized patients with COVID-19."

Starbucks (SBUX), the global specialty coffee chain, was upgraded to "outperform" from "market perform" at Cowen.

Later today, final readings of 2Q annualized GDP will be expected at -31.7% on quarter. The Automatic Data Processing (ADP) will post private jobs for September (+648,000 jobs expected). The Market News International will report Chicago PMI for September (52.0 expected). The National Association of Realtors will release August pending home sales (+3.2% on month expected).

European indices are on the downside. The German Federal Statistical Office has reported September jobless rate at 6.3% (vs 6.5% expected) and August retail sales at +3.1% (vs +0.4% on month expected). France's INSEE has posted CPI for September at +0.1% (vs +0.2% on year expected). The U.K. Office for National Statistics has released final readings of 2Q GDP at -19.8% (vs -20.4% on quarter expected). The Nationwide Building Society has posted its House Price Index for September at +0.9% (vs +0.5% on month expected).

Asian indices closed on a strong down move except the Hong Kong HSI which ended in the green. China's official Manufacturing PMI rose to a 6-month high of 51.5 in September (51.3 expected) from 51.0 in August and Non-manufacturing PMI climbed to the highest level since November 2013 at 55.9 (54.7 expected) from 55.2. On the other hand, China's Caixin Manufacturing PMI slipped to 53.0 in September (53.1 expected) from 53.1 in August. Japan's industrial production grew 1.7% on month in August (+1.4% expected) and retail sales rose 4.6% (+2.0% expected).

WTI Crude Oil futures remain bearish. The American Petroleum Institute (API) reported that U.S. crude-oil inventories fell 831,000 barrels in the week ending September 25. Later today, the U.S. Energy Information Administration (EIA) will release official crude oil inventories data for the same period.

Gold lost ground as the U.S dollar strengthens on COVID-19 fears

Gold fell 12.54 dollars (-0.66%) to 1885.54 dollars.

The dollar index rose 0.2pt to 94.091.

U.S. Equity Snapshot

Walt Disney (DIS), the entertainment and media giant, plans to lay off 28,000 employees in its theme parks, amid COVID-19 restrictions.

Source: TradingView, GAIN Capital

Micron Technology (MU), a manufacturer of memory chips, lost ground after hours as current quarter sales forecast missed estimates.

Alphabet (GOOGL): according to Reuters, China may launch antitrust probe into Google.Regeneron Pharmaceuticals (REGN), a biotech, announced "the first data from a descriptive analysis of a seamless Phase 1/2/3 trial of its investigational antibody cocktail REGN-COV2 showing it reduced viral load and the time to alleviate symptoms in non-hospitalized patients with COVID-19."

Starbucks (SBUX), the global specialty coffee chain, was upgraded to "outperform" from "market perform" at Cowen.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM