EU indices mixed | TA focus on Novartis

INDICES

Yesterday, European stocks were deeply in the red. The Stoxx Europe 600 Index dropped 1.81%, Germany's DAX 30 plunged 3.71%, France's CAC 40 lost 1.90% and the U.K.'s FTSE 100 was down 1.16%.

EUROPE ADVANCE/DECLINE

92% of STOXX 600 constituents traded lower or unchanged yesterday.

26% of the shares trade above their 20D MA vs 45% Friday (below the 20D moving average).

52% of the shares trade above their 200D MA vs 60% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 3.6pts to 31.76, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Autos, Media, Utilities

3mths relative low: Technology, Energy

Europe Best 3 sectors

travel & leisure, automobiles & parts, banks

Europe worst 3 sectors

technology, basic resources, chemicals

INTEREST RATE

The 10yr Bund yield fell 1bp to -0.57% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -18bps (below its 20D MA).

ECONOMIC DATA

FR 08:45: Sep PPI MoM, exp.: 0.1%

EC 10:00: Sep Loans to Companies YoY, exp.: 7.1%

EC 10:00: Sep M3 Money Supply YoY, exp.: 9.5%

EC 10:00: Sep Loans to Households YoY, exp.: 3%

FR 12:00: Sep Unemployment Benefit Claims, exp.: -171K

FR 12:00: Sep Jobseekers Total, exp.: 3621.5K

UK 12:00: Oct CBI Distributive Trades, exp.: 11

MORNING TRADING

In Asian trading hours, EUR/USD rebounded to 1.1820 and GBP/USD bounced to 1.3035. USD/JPY slipped to 104.70.

Spot gold climbed to $1,909 an ounce.

#UK - IRELAND#

BP, an oil giant, reported that 3Q underlying replacement cost profit slumped to 86 million dollars from 2.25 billion dollars in the prior-year period, and compared with an underlying replacement cost loss of 6.68 billion dollars in the prior quarter. The company said: "Compared to the previous quarter, the result benefitted from the absence of significant exploration write-offs and recovering oil and gas prices and demand. This was partly offset by a significantly lower oil trading result. (...) A dividend of 5.25 cents per share was announced for the quarter."

#FRANCE#

Orange, a telecommunications group, was upgraded to "equalweight" from "underweight" at Morgan Stanley.

#SPAIN#

Santander, a Spanish bank, announced that 3Q underlying profit dropped 18% on year to 1.75 billion euros on net interest income of 7.77 billion, up 1%. The bank stated: "The bank has improved its outlook on cost of credit in 2020 to c.1.3% from its previous guidance of 1.4-1.5%, due to the positive trends in customer behaviour and better macro forecasts. This better outlook, paired with strong cost control, give the bank reason to expect an underlying profit of around E5 billion for the year."

#SWITZERLAND#

Novartis, a Swiss multinational pharmaceutical group, posted 3Q core net income rose 8% on year to 3.47 billion dollars and core operating income increased 9% to 4.07 billion dollars on net sales of 12.26 billion dollars, up 1% (flat at constant currency). The company has raised its full-year core operating income growth forecast to "low double digit to mid teens" from "low double digit" previously and expects net sales to grow mid single digit.

UPM-Kymmene, a Finnish forest industry company, is expected to report 3Q results.

Yesterday, European stocks were deeply in the red. The Stoxx Europe 600 Index dropped 1.81%, Germany's DAX 30 plunged 3.71%, France's CAC 40 lost 1.90% and the U.K.'s FTSE 100 was down 1.16%.

EUROPE ADVANCE/DECLINE

92% of STOXX 600 constituents traded lower or unchanged yesterday.

26% of the shares trade above their 20D MA vs 45% Friday (below the 20D moving average).

52% of the shares trade above their 200D MA vs 60% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 3.6pts to 31.76, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Autos, Media, Utilities

3mths relative low: Technology, Energy

Europe Best 3 sectors

travel & leisure, automobiles & parts, banks

Europe worst 3 sectors

technology, basic resources, chemicals

INTEREST RATE

The 10yr Bund yield fell 1bp to -0.57% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -18bps (below its 20D MA).

ECONOMIC DATA

FR 08:45: Sep PPI MoM, exp.: 0.1%

EC 10:00: Sep Loans to Companies YoY, exp.: 7.1%

EC 10:00: Sep M3 Money Supply YoY, exp.: 9.5%

EC 10:00: Sep Loans to Households YoY, exp.: 3%

FR 12:00: Sep Unemployment Benefit Claims, exp.: -171K

FR 12:00: Sep Jobseekers Total, exp.: 3621.5K

UK 12:00: Oct CBI Distributive Trades, exp.: 11

MORNING TRADING

In Asian trading hours, EUR/USD rebounded to 1.1820 and GBP/USD bounced to 1.3035. USD/JPY slipped to 104.70.

Spot gold climbed to $1,909 an ounce.

#UK - IRELAND#

BP, an oil giant, reported that 3Q underlying replacement cost profit slumped to 86 million dollars from 2.25 billion dollars in the prior-year period, and compared with an underlying replacement cost loss of 6.68 billion dollars in the prior quarter. The company said: "Compared to the previous quarter, the result benefitted from the absence of significant exploration write-offs and recovering oil and gas prices and demand. This was partly offset by a significantly lower oil trading result. (...) A dividend of 5.25 cents per share was announced for the quarter."

#FRANCE#

Orange, a telecommunications group, was upgraded to "equalweight" from "underweight" at Morgan Stanley.

#SPAIN#

Santander, a Spanish bank, announced that 3Q underlying profit dropped 18% on year to 1.75 billion euros on net interest income of 7.77 billion, up 1%. The bank stated: "The bank has improved its outlook on cost of credit in 2020 to c.1.3% from its previous guidance of 1.4-1.5%, due to the positive trends in customer behaviour and better macro forecasts. This better outlook, paired with strong cost control, give the bank reason to expect an underlying profit of around E5 billion for the year."

#SWITZERLAND#

Novartis, a Swiss multinational pharmaceutical group, posted 3Q core net income rose 8% on year to 3.47 billion dollars and core operating income increased 9% to 4.07 billion dollars on net sales of 12.26 billion dollars, up 1% (flat at constant currency). The company has raised its full-year core operating income growth forecast to "low double digit to mid teens" from "low double digit" previously and expects net sales to grow mid single digit.

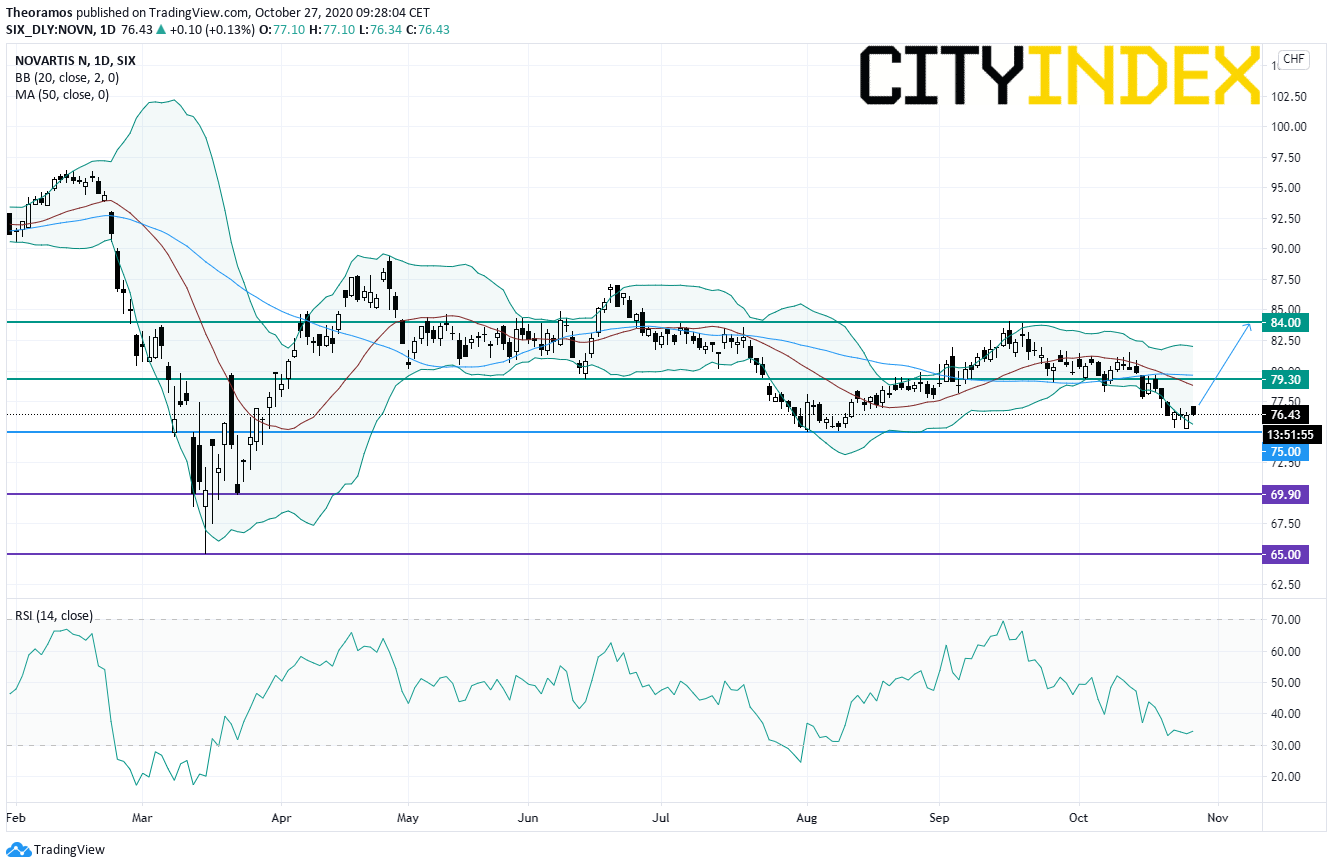

From a technical point of view, the stock is rebounding from the lower end of the short term trading range at 75CHF. As long as this key level is support, readers may consider the potential for opening long positions with the overlap area at 79.3CHF and the previous top of September at 84CHF as targets. Alternatively, a break below 75CHF would call for a new down leg towards 69.9CHF.

Source: TradingView, GAIN Capital

UPM-Kymmene, a Finnish forest industry company, is expected to report 3Q results.

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Commodities articles

Yesterday 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM