US Futures mixed - Watch CRM, AAPL, TSLA, NIO, HP, INTU

The S&P 500 Futures remain flat after they closed mixed yesterday. While both the S&P 500 and the Nasdaq 100 closed at record levels again, the Dow Jones Industrial Average eased 60 points (-0.21%) to 28248. Market sentiment was boosted by progress in the U.S.-China phase-one trade deal.

Later today, the U.S. Commerce Department will report Durable Goods Orders for July (+4.5% on month expected).

European indices are rebounding after a pessimistic open. France's INSEE has posted Consumer Confidence Index for August at 94, as expected.

Asian indices all closed in the red. Official data showed that New Zealand recorded a trade surplus of 282 million New Zealand dollars (293 million New Zealand dollars surplus expected), where exports totaled 4.91 billion New Zealand dollars (as expected).

WTI Crude Oil futures are still well directed. The American Petroleum Institute (API) reported that U.S. crude-oil inventories fell 4.5 million barrels for week ended August 21. IHS Markit estimated that global oil demand would be between 92M - 95M b/d through the 1Q of 2021, the level below pre-Covid level. Later today, the U.S. Energy Information Administration (EIA) will release official crude oil inventories data for the same week.

Gold consolidates before Jerome Powell speech scheduled tomorrow while the US dollar steadies after falling yesterday following disappointing US consumer confidence index data.

Gold fell 8.35 dollars (-0.43%) to 1919.32 dollars.

The dollar index rose 0.03pt to 93.048.

U.S. Equity Snapshot

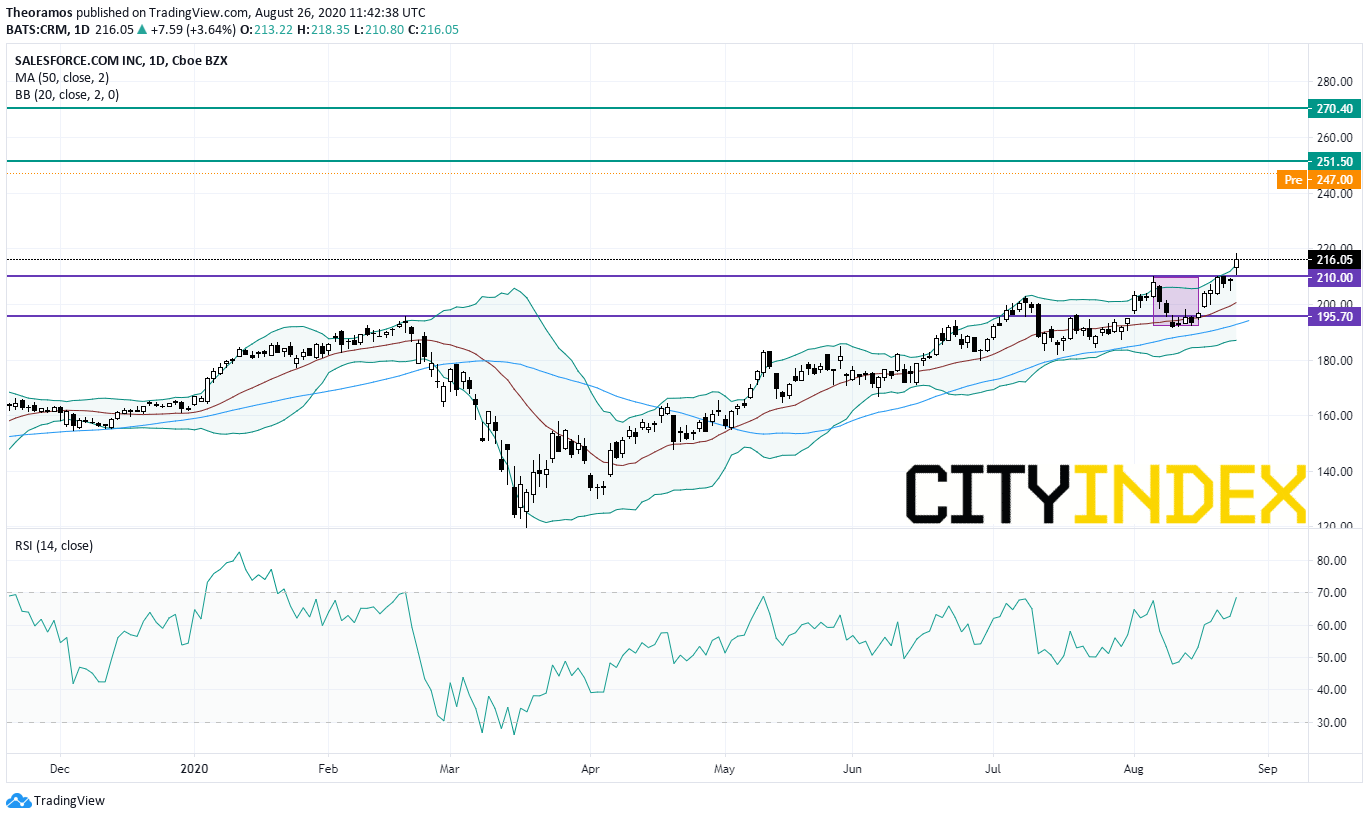

Salesforce.com (CRM), a developer of business software, disclosed second quarter adjusted EPS of 1.44 dollar, higher than anticipated, up from 0.66 dollar a year earlier, on revenue of 5.2 billion dollars, exceeding the consensus, up from 4.0 billion dollars a year ago.

Source: TradingView, GAIN Capital

Nio (NIO), the Chinese electric-vehicle maker, was upgraded to "overweight" from "equalweight" at Morgan Stanley.

HP (HPE), a supplier of information technology products and services, announced third quarter adjusted EPS of 0.32 dollar, beating the consensus, down from 0.45 dollar a year ago on net revenue of 6.8 billion dollars, also exceeding forecasts, down from 7.2 billion dollars in the prior year.

Intuit (INTU), a developer and marketer of accounting software for small and medium sized businesses, unveiled fourth adjusted quarter EPS of 1.81 dollar, above estimates, vs an adjusted LPS of 0.09 dollar a year ago, on net revenue of 1.8 billion dollars, better than predicted, up from 994.0 million dollars a year earlier.

Nordstrom (JWN), the fashion retailer, released second quarter adjusted LPS of 1.62 dollar, missing estimates, vs an adjusted EPS of 0.91 dollar a year ago on net sales of 1.8 billion dollars, worse than expected, down from 3.8 billion dollars a year earlier.

Toll Brothers (TOL), the home construction company, gained ground in extending trading after releasing quarterly earnings that beat estimates.

Urban Outfitters (URBN), the clothing retailer, is expected to soar after posting better than expected quarterly earnings.

Autodesk (ADSK), a provider of computer-aided design software, lost some ground after hours as third quarter adjusted EPS forecast missed estimates.

Roku (ROKU), the video streaming platform, was rated "buy" in a new coverage at Citi.

Later today, the U.S. Commerce Department will report Durable Goods Orders for July (+4.5% on month expected).

European indices are rebounding after a pessimistic open. France's INSEE has posted Consumer Confidence Index for August at 94, as expected.

Asian indices all closed in the red. Official data showed that New Zealand recorded a trade surplus of 282 million New Zealand dollars (293 million New Zealand dollars surplus expected), where exports totaled 4.91 billion New Zealand dollars (as expected).

WTI Crude Oil futures are still well directed. The American Petroleum Institute (API) reported that U.S. crude-oil inventories fell 4.5 million barrels for week ended August 21. IHS Markit estimated that global oil demand would be between 92M - 95M b/d through the 1Q of 2021, the level below pre-Covid level. Later today, the U.S. Energy Information Administration (EIA) will release official crude oil inventories data for the same week.

Gold consolidates before Jerome Powell speech scheduled tomorrow while the US dollar steadies after falling yesterday following disappointing US consumer confidence index data.

Gold fell 8.35 dollars (-0.43%) to 1919.32 dollars.

The dollar index rose 0.03pt to 93.048.

U.S. Equity Snapshot

Salesforce.com (CRM), a developer of business software, disclosed second quarter adjusted EPS of 1.44 dollar, higher than anticipated, up from 0.66 dollar a year earlier, on revenue of 5.2 billion dollars, exceeding the consensus, up from 4.0 billion dollars a year ago.

Source: TradingView, GAIN Capital

Apple's (AAPL), the tech giant, price target was raised to 600 dollars from 515 dollars at Wedbush.

Tesla's (TSLA), the electric-vehicle maker, price target was raised to 2,500 dollars from 1,200 dollars at Jefferies.Nio (NIO), the Chinese electric-vehicle maker, was upgraded to "overweight" from "equalweight" at Morgan Stanley.

HP (HPE), a supplier of information technology products and services, announced third quarter adjusted EPS of 0.32 dollar, beating the consensus, down from 0.45 dollar a year ago on net revenue of 6.8 billion dollars, also exceeding forecasts, down from 7.2 billion dollars in the prior year.

Intuit (INTU), a developer and marketer of accounting software for small and medium sized businesses, unveiled fourth adjusted quarter EPS of 1.81 dollar, above estimates, vs an adjusted LPS of 0.09 dollar a year ago, on net revenue of 1.8 billion dollars, better than predicted, up from 994.0 million dollars a year earlier.

Nordstrom (JWN), the fashion retailer, released second quarter adjusted LPS of 1.62 dollar, missing estimates, vs an adjusted EPS of 0.91 dollar a year ago on net sales of 1.8 billion dollars, worse than expected, down from 3.8 billion dollars a year earlier.

Toll Brothers (TOL), the home construction company, gained ground in extending trading after releasing quarterly earnings that beat estimates.

Urban Outfitters (URBN), the clothing retailer, is expected to soar after posting better than expected quarterly earnings.

Autodesk (ADSK), a provider of computer-aided design software, lost some ground after hours as third quarter adjusted EPS forecast missed estimates.

Roku (ROKU), the video streaming platform, was rated "buy" in a new coverage at Citi.

Latest market news

Today 07:55 AM

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Yesterday 08:00 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM