US Futures still red, watch BA, DD, ACN, KBH

The S&P 500 Futures remain weak after U.S. stocks lost over 2% on Wednesday as investors' confidence in the economic recovery was shaken by resurging coronavirus cases. The U.S. recorded a one-day total of more than 36,000 new cases, the highest level since late April. California, Florida and Oklahoma reported record highs in new cases. Also, the International Monetary Fund downgraded its global economic outlook, projecting a contraction of 4.9% this year, compared with a decline of 3.0% previously estimated in April.

Later today, the U.S. Commerce Department will report final readings of 1Q annualized GDP (-5.0% on quarter expected), May durable goods orders, wholesale inventories and advance goods trade balance. The Labor Department will post initial jobless claims in the week ended June 20 (1.3 million expected).

European indices are recovering. On the statistical front, Germany's GfK Consumer Confidence Index for July rose from -18.6 to -9.6 (-12.0 expected).

Asian indices ended sharply lower. The Japanese Nikkei lost 1.22% lower and the Australian ASX 200 dropped by 2.48% while the Mainland China and Hong Kong markets were closed

WTI Crude Oil Futures was little changed during Asian session. The U.S. Energy Information Administration (EIA) reported that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 1.4M barrels from the previous week to 540.7M barrels for week ended June 19. Besides, U.S. crude oil production rebounded to 11M b/d last week from 10.5M b/d in the prior period.

Gold remains firm after nearly hitting a 8-year high on rising global COVID-19 cases.

Gold rose 1.38 dollars (+0.08%) to 1762.56 dollars.

The US dollar edges higher on increasing fears regarding economic growth.

The dollar index gained 0.25pt to 97.397.

Later today, the U.S. Commerce Department will report final readings of 1Q annualized GDP (-5.0% on quarter expected), May durable goods orders, wholesale inventories and advance goods trade balance. The Labor Department will post initial jobless claims in the week ended June 20 (1.3 million expected).

European indices are recovering. On the statistical front, Germany's GfK Consumer Confidence Index for July rose from -18.6 to -9.6 (-12.0 expected).

Asian indices ended sharply lower. The Japanese Nikkei lost 1.22% lower and the Australian ASX 200 dropped by 2.48% while the Mainland China and Hong Kong markets were closed

WTI Crude Oil Futures was little changed during Asian session. The U.S. Energy Information Administration (EIA) reported that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 1.4M barrels from the previous week to 540.7M barrels for week ended June 19. Besides, U.S. crude oil production rebounded to 11M b/d last week from 10.5M b/d in the prior period.

Gold remains firm after nearly hitting a 8-year high on rising global COVID-19 cases.

Gold rose 1.38 dollars (+0.08%) to 1762.56 dollars.

The US dollar edges higher on increasing fears regarding economic growth.

The dollar index gained 0.25pt to 97.397.

US Equity Snapshot

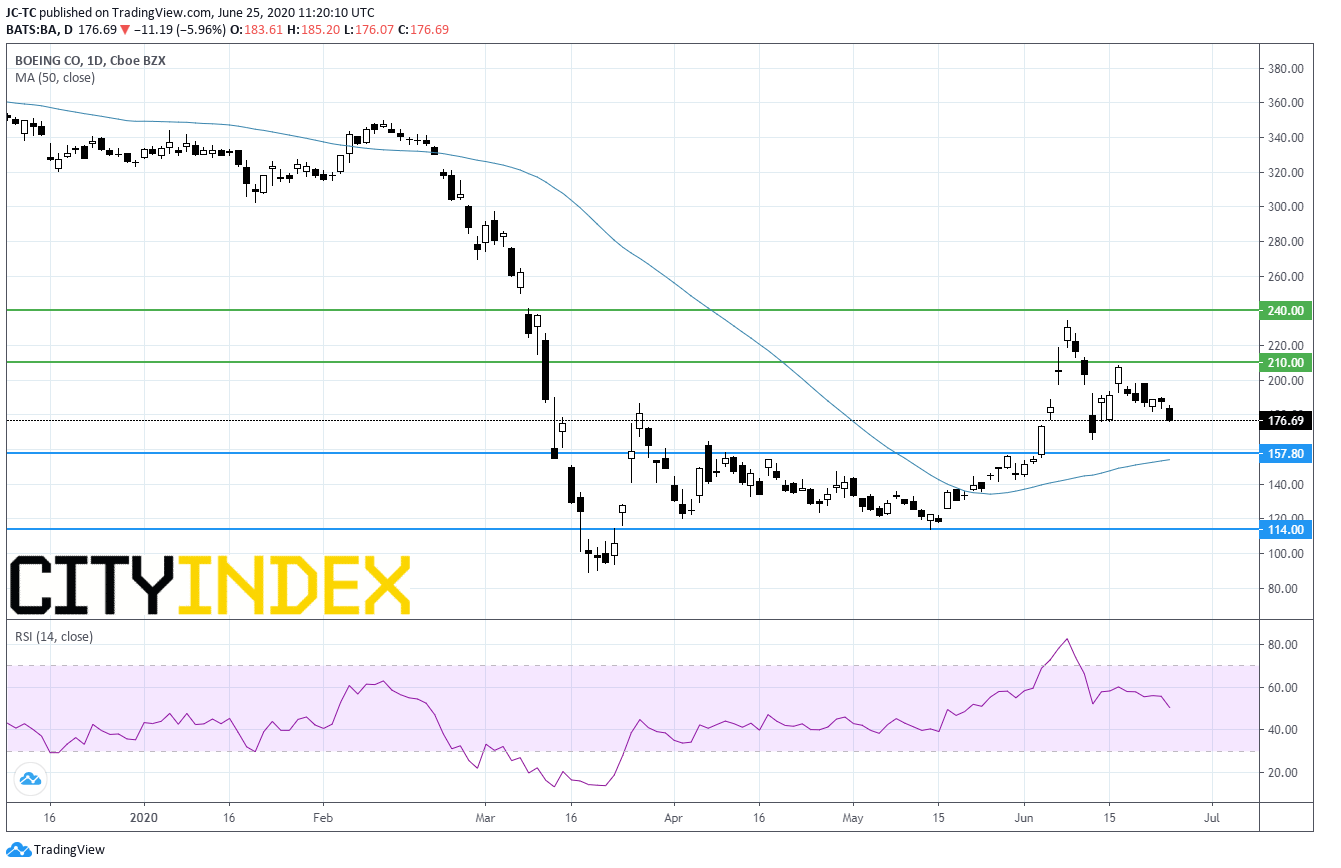

Boeing (BA), the aircraft maker, was downgraded to "sell" from "hold" at Berenberg.

DuPont (DD), a diversified specialty chemicals company, maintains quarterly dividend of 0.30 dollar per share. Separately, the stock was upgraded to "outperform" from "sector perform" at RBC Capital.

Accenture (ACN), a leading global professional services company, expects full year sales growth to be 3.5% to 4.5% vs a previous forecast of 3%-6%. Full year EPS is seen at 7.57-7.70 dollars vs a previous estimate of 7.48-7.70 dollars. Separately, the company posted third quarter EPS down to 1.90 dollar from 1.93 dollar a year earlier, on sales down 1% to 11 billion dollars.

KB Home (KBH), the homebuilder, plunged after hours after posting second quarter net orders down 57%. Sales were down to 914 million dollars, lower than expected, from 1.02 billion dollars a year earlier.

Source : TradingVIEW, Gain Capital

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM