U.S Futures mixed- Watch HPQ, IBM, DE, GPS, F, JWN

The S&P 500 Futures are little changed after they rallied further yesterday, pushing the Dow Jones Industrial Average (+455 points or 1.54% to 30046) to close above the key 30,000 level for the first time. Investors were encouraged by news reports that formal transition for Joe Biden's potential administration has begun, and that Biden would appoint former Federal Reserve Chair Janet Yellen as his would-be Treasury Secretary.

Later today, the U.S. Federal Reserve will release its latest FOMC meeting minutes. The U.S. Labor Department will post initial jobless claims in the week ending November 21 (0.73 million expected). The Commerce Department will post the second estimate of 3Q annualized GDP (+33.1% on quarter expected), October durable goods orders (+0.9% on month expected), wholesale inventories (+0.4% on month expected), personal spending (+0.4% on month expected), personal income (flat on month expected) and new home sales (0.98 million units expected). The University of Michigan will publish its final readings of Consumer Sentiment Index for November (77.0 expected).

European indices are posting a pull back after a positive open.

Asian indices closed on the upside except the Chinese CSI. NZD/USD hit 0.7000 for the first time since June 2018, as it was widely expected that New Zealand may not see further interest-rate cuts.

WTI Crude Oil is still bullish. The American Petroleum Institute (API) reported that U.S. crude-oil inventories rose 3.8M barrels in the week ending November 20 (+0.1 million barrels expected). Later today, the International Energy Agency (EIA) will release official crude oil inventories data for the same week (+0.2 million barrels expected).

U.S indices closed up on Tuesday, lifted by Banks (+5.52%), Energy (+5.16%) and Automobiles & Components (+4.66%) sectors.

Approximately 90% of stocks in the S&P 500 Index were trading above their 200-day moving average and 80% were trading above their 20-day moving average. The VIX Index fell 1.02pt (-4.5%) to 21.64 and WTI Crude Oil jumped $1.82 (+4.23%) to $44.88 at the close.

On the U.S economic data front, the Conference Board's Consumer Confidence Index fell to 96.1 on month in November (98.0 expected), from a revised 101.4 in October.

Gold edges higher on consolidating U.S dollar.

Gold rose 4.89 dollars (+0.27%) to 1812.49.

The dollar index was flat at 92.23.

U.S. Equity Snapshot

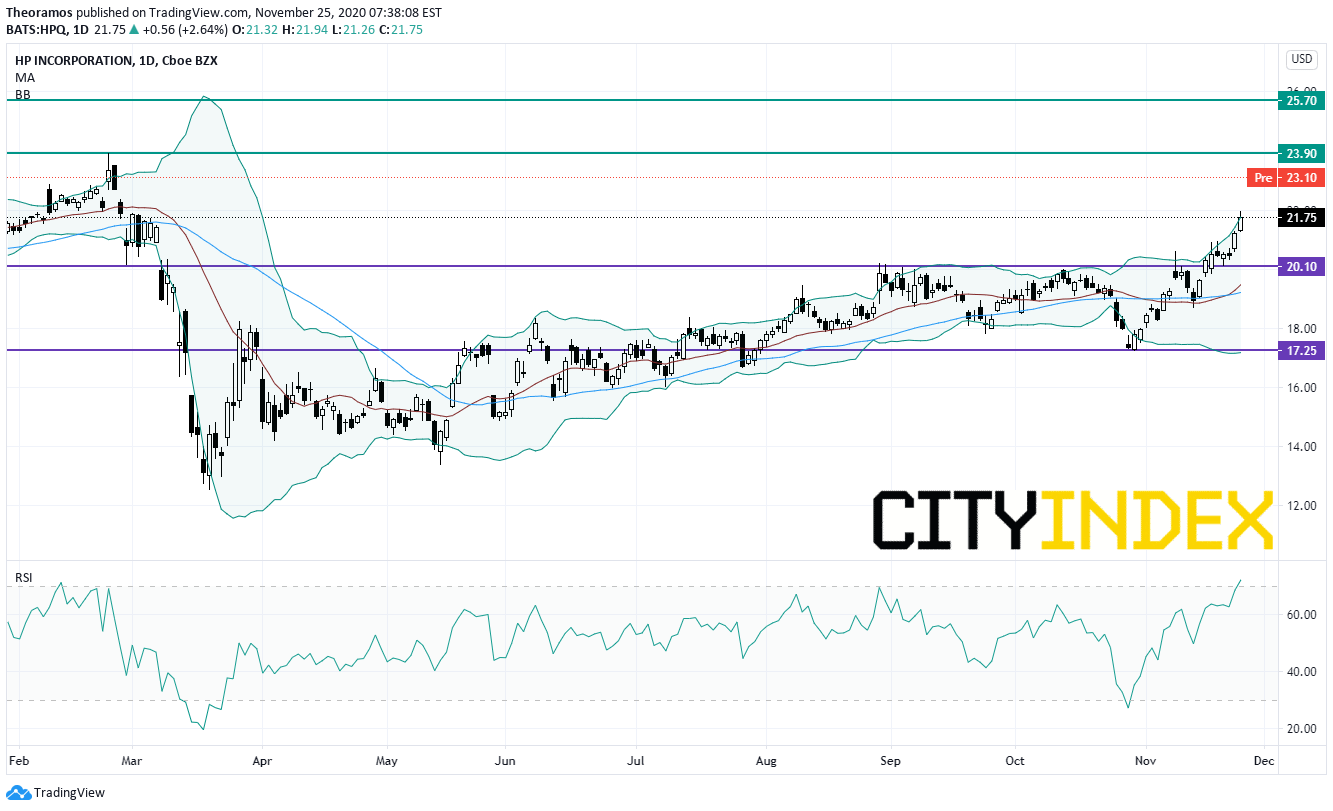

HP (HPQ), a provider of computers, printers and printer supplies, jumped after hours after disclosing fourth quarter adjusted EPS of 0.62 dollar, beating forecasts, up from 0.60 dollar a year ago on net revenue of 15.3 billion dollars, higher than anticipated, down from 15.4 billion dollars a year earlier. The company also issue current quarter earnings guidance that beat estimates.

Source: TradingView, GAIN Capital

IBM (IBM), an IT company, plans to cut about 10,000 jobs in Europe, according to Bloomberg.

Deere & Co (DE), a manufacturer of agricultural and construction equipment, reported fourth quarter sales down 0.5% to 8.66 billion dollars, beating estimates. EPS was up to 2.39 dollars from 2.27 dollars a year earlier. The company expects fiscal 2021 net income between 3.6 and 4 billion dollars, above forecasts.

Gap (GPS), a retailer of apparel, dived postmarket after announcing third quarter EPS of 0.25 dollar, missing estimates, down from 0.53 dollar a year ago.

Ford Motor (F), the automobile manufacturer, was donwgraded to "equalweight" from "overweight" at Morgan Stanley.

Nordstrom (JWN), the North American fashion retailer, gained ground postmarket after posting third quarter earnings that beat estimates.

Dollar Tree (DLTR), a discount store chain, was downgraded to "neutral" from "overweight" at JPMorgan.

Dell Technologies (DELL), a computer technology company, released third quarter adjusted EPS of 2.03 dollars, exceeding the consensus, up from 1.75 dollar a year ago on revenue of 23.5 billion dollars, above forecasts, up from 22.9 billion dollars a year earlier.

Autodesk (ADSK), a provider of computer-aided design software, reported third quarter adjusted EPS of 1.04 dollar, just ahead of estimates, up from 0.78 dollar a year ago on revenue of 952.0 million dollars, also above expectations, up from 842.7 million dollars a year earlier.

Later today, the U.S. Federal Reserve will release its latest FOMC meeting minutes. The U.S. Labor Department will post initial jobless claims in the week ending November 21 (0.73 million expected). The Commerce Department will post the second estimate of 3Q annualized GDP (+33.1% on quarter expected), October durable goods orders (+0.9% on month expected), wholesale inventories (+0.4% on month expected), personal spending (+0.4% on month expected), personal income (flat on month expected) and new home sales (0.98 million units expected). The University of Michigan will publish its final readings of Consumer Sentiment Index for November (77.0 expected).

European indices are posting a pull back after a positive open.

Asian indices closed on the upside except the Chinese CSI. NZD/USD hit 0.7000 for the first time since June 2018, as it was widely expected that New Zealand may not see further interest-rate cuts.

WTI Crude Oil is still bullish. The American Petroleum Institute (API) reported that U.S. crude-oil inventories rose 3.8M barrels in the week ending November 20 (+0.1 million barrels expected). Later today, the International Energy Agency (EIA) will release official crude oil inventories data for the same week (+0.2 million barrels expected).

U.S indices closed up on Tuesday, lifted by Banks (+5.52%), Energy (+5.16%) and Automobiles & Components (+4.66%) sectors.

Approximately 90% of stocks in the S&P 500 Index were trading above their 200-day moving average and 80% were trading above their 20-day moving average. The VIX Index fell 1.02pt (-4.5%) to 21.64 and WTI Crude Oil jumped $1.82 (+4.23%) to $44.88 at the close.

On the U.S economic data front, the Conference Board's Consumer Confidence Index fell to 96.1 on month in November (98.0 expected), from a revised 101.4 in October.

Gold edges higher on consolidating U.S dollar.

Gold rose 4.89 dollars (+0.27%) to 1812.49.

The dollar index was flat at 92.23.

U.S. Equity Snapshot

HP (HPQ), a provider of computers, printers and printer supplies, jumped after hours after disclosing fourth quarter adjusted EPS of 0.62 dollar, beating forecasts, up from 0.60 dollar a year ago on net revenue of 15.3 billion dollars, higher than anticipated, down from 15.4 billion dollars a year earlier. The company also issue current quarter earnings guidance that beat estimates.

Source: TradingView, GAIN Capital

IBM (IBM), an IT company, plans to cut about 10,000 jobs in Europe, according to Bloomberg.

Deere & Co (DE), a manufacturer of agricultural and construction equipment, reported fourth quarter sales down 0.5% to 8.66 billion dollars, beating estimates. EPS was up to 2.39 dollars from 2.27 dollars a year earlier. The company expects fiscal 2021 net income between 3.6 and 4 billion dollars, above forecasts.

Gap (GPS), a retailer of apparel, dived postmarket after announcing third quarter EPS of 0.25 dollar, missing estimates, down from 0.53 dollar a year ago.

Ford Motor (F), the automobile manufacturer, was donwgraded to "equalweight" from "overweight" at Morgan Stanley.

Nordstrom (JWN), the North American fashion retailer, gained ground postmarket after posting third quarter earnings that beat estimates.

Dollar Tree (DLTR), a discount store chain, was downgraded to "neutral" from "overweight" at JPMorgan.

Dell Technologies (DELL), a computer technology company, released third quarter adjusted EPS of 2.03 dollars, exceeding the consensus, up from 1.75 dollar a year ago on revenue of 23.5 billion dollars, above forecasts, up from 22.9 billion dollars a year earlier.

Autodesk (ADSK), a provider of computer-aided design software, reported third quarter adjusted EPS of 1.04 dollar, just ahead of estimates, up from 0.78 dollar a year ago on revenue of 952.0 million dollars, also above expectations, up from 842.7 million dollars a year earlier.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM