EU indices gaining some ground | TA on Sandvik

INDICES

Yesterday, European stocks also gained. The Stoxx Europe 600 rose 0.91%, Germany's DAX advanced 1.26%, France's CAC 40 increased 1.21%, and the U.K.'s FTSE 100 was up 1.55%.

EUROPE ADVANCE/DECLINE

56% of STOXX 600 constituents traded higher yesterday.

73% of the shares trade above their 20D MA vs 79% Monday (above the 20D moving average).

84% of the shares trade above their 200D MA vs 84% Monday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 1.12pt to 21.37, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Insurance, Autos, Banks, Travel & Leisure, Energy, Basic Resource

3mths relative low: Chemicals, Food & Beverage, Healthcare

Europe Best 3 sectors

energy, banks, basic resources

Europe worst 3 sectors

personal & household goods, health care, real estate

INTEREST RATE

The 10yr Bund yield was unchanged to -0.58% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -18bps (below its 20D MA).

ECONOMIC DATA

GE 08:40: Bundesbank Mauderer speech

EC 10:30: ECB Financial Stability Review

FR 12:00: Oct Jobseekers Total, exp.: 3606.3K

FR 12:00: Oct Unemployment Benefit Claims, exp.: -15.2K

GE 12:15: Bundesbank Wuermeling speech

UK 13:00: 2020 Spending Review

UK 13:00: OBR Economic and Fiscal Forecasts

MORNING TRADING

In Asian trading hours, EUR/USD rose further to 1.1904 and GBP/USD held gains at 1.3358. USD/JPY edged up to 104.51.

Spot gold was little changed at $1,806 an ounce.

#UK - IRELAND#

Melrose Industries, an investment group, posted a trading update for the four months to October 31: "Melrose is currently trading at the top end of the Board's expectations for 2020. (...) The performance of the Group in the Period reflected the faster than expected recovery in automotive markets, first seen over the summer, the continued strong performance in Nortek Air Management, and the more challenging, although currently stable, market conditions in Aerospace."

#GERMANY#

Thyssenkrupp, an industrial engineering group, was upgraded to "buy" from "hold" at Deutsche Bank.

#FRANCE#

Dassault Systemes, a software company, announced the acquisition of the remainder of cloud-native distributed SQL database company NuoDB equity, which it had a 16% ownership interest. Financial terms were not disclosed.

Air Liquide, an industrial gases supplier, was downgraded to "hold" from "buy" at HSBC.

#SPAIN#

CaixaBank and Bankia, the two Spanish banks, were downgraded to "hold" from "buy" at HSBC.

#BENELUX#

Unibail-Rodamco-Westfield, a commercial real estate company, was upgraded to "neutral" from "sell" at Goldman Sachs.

#SWEDEN#

Volvo, a vehicle manufacturer, was upgraded to "buy" from "hold" at HSBC.

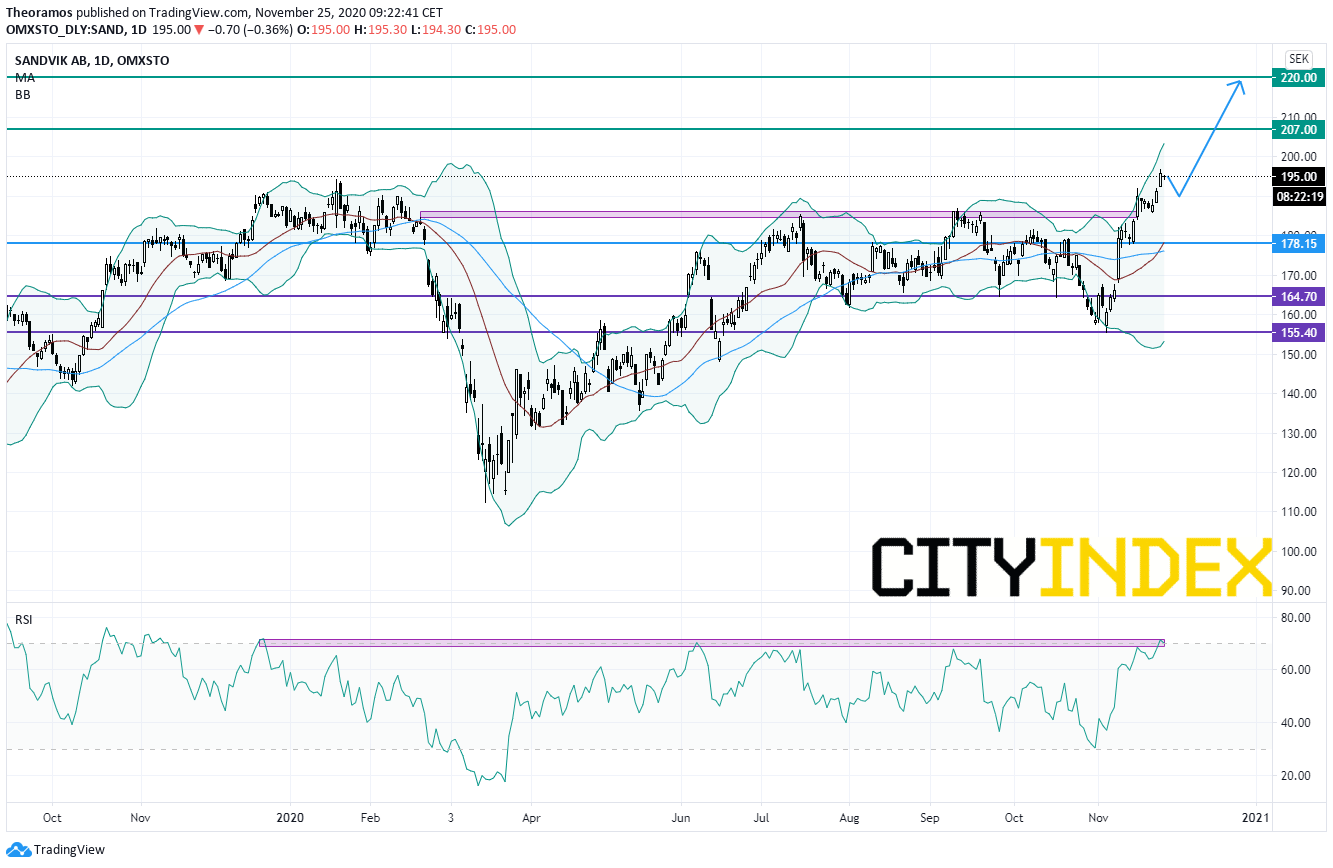

Sandvik, a Swedish engineering group, was downgraded to "hold" from "buy" at HSBC.

From a technical point of view, the share has broken above the key horizontal resistance around 185SEK, given us the signal of a new up leg and allowing the share price to reach a new all-time high. the RSI is now overbought and is calling for a slight pullback towards 190SEK. Above 178.15SEK, after the correction move, targets are set at 207SEK and 220SEK in extension.

EX-DIVIDEND

Assa Abloy: SEK1.85

Yesterday, European stocks also gained. The Stoxx Europe 600 rose 0.91%, Germany's DAX advanced 1.26%, France's CAC 40 increased 1.21%, and the U.K.'s FTSE 100 was up 1.55%.

EUROPE ADVANCE/DECLINE

56% of STOXX 600 constituents traded higher yesterday.

73% of the shares trade above their 20D MA vs 79% Monday (above the 20D moving average).

84% of the shares trade above their 200D MA vs 84% Monday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 1.12pt to 21.37, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Insurance, Autos, Banks, Travel & Leisure, Energy, Basic Resource

3mths relative low: Chemicals, Food & Beverage, Healthcare

Europe Best 3 sectors

energy, banks, basic resources

Europe worst 3 sectors

personal & household goods, health care, real estate

INTEREST RATE

The 10yr Bund yield was unchanged to -0.58% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -18bps (below its 20D MA).

ECONOMIC DATA

GE 08:40: Bundesbank Mauderer speech

EC 10:30: ECB Financial Stability Review

FR 12:00: Oct Jobseekers Total, exp.: 3606.3K

FR 12:00: Oct Unemployment Benefit Claims, exp.: -15.2K

GE 12:15: Bundesbank Wuermeling speech

UK 13:00: 2020 Spending Review

UK 13:00: OBR Economic and Fiscal Forecasts

MORNING TRADING

In Asian trading hours, EUR/USD rose further to 1.1904 and GBP/USD held gains at 1.3358. USD/JPY edged up to 104.51.

Spot gold was little changed at $1,806 an ounce.

#UK - IRELAND#

Melrose Industries, an investment group, posted a trading update for the four months to October 31: "Melrose is currently trading at the top end of the Board's expectations for 2020. (...) The performance of the Group in the Period reflected the faster than expected recovery in automotive markets, first seen over the summer, the continued strong performance in Nortek Air Management, and the more challenging, although currently stable, market conditions in Aerospace."

#GERMANY#

Thyssenkrupp, an industrial engineering group, was upgraded to "buy" from "hold" at Deutsche Bank.

#FRANCE#

Dassault Systemes, a software company, announced the acquisition of the remainder of cloud-native distributed SQL database company NuoDB equity, which it had a 16% ownership interest. Financial terms were not disclosed.

Air Liquide, an industrial gases supplier, was downgraded to "hold" from "buy" at HSBC.

#SPAIN#

CaixaBank and Bankia, the two Spanish banks, were downgraded to "hold" from "buy" at HSBC.

#BENELUX#

Unibail-Rodamco-Westfield, a commercial real estate company, was upgraded to "neutral" from "sell" at Goldman Sachs.

#SWEDEN#

Volvo, a vehicle manufacturer, was upgraded to "buy" from "hold" at HSBC.

Sandvik, a Swedish engineering group, was downgraded to "hold" from "buy" at HSBC.

From a technical point of view, the share has broken above the key horizontal resistance around 185SEK, given us the signal of a new up leg and allowing the share price to reach a new all-time high. the RSI is now overbought and is calling for a slight pullback towards 190SEK. Above 178.15SEK, after the correction move, targets are set at 207SEK and 220SEK in extension.

Source: TradingView, GAIN Capital

EX-DIVIDEND

Assa Abloy: SEK1.85

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM