U.S Futures green - Watch TIF, BBY, A, MDT

The S&P 500 Futures remain on the upside after they closed broadly higher yesterday. Once again, market sentiment was boosted by vaccine news. After market closed, Donald Trump authorized Joe Biden to access federal funding for the presidential transition.

Later today, the U.S., the Conference Board will release its Consumer Confidence Index for November (97.9 expected). The Federal Housing Finance Agency will post its house price index for September (+0.5% on month expected). SP Case Shiller will report its house price index for September (+0.6% on month expected).

European indices are strongly rebounding after late session consolidation move yesterday. The German Federal Statistical Office has posted final readings of 3Q GDP at +8.5% (vs +8.2% on quarter expected). Germany's IFO Business has released November Climate Index at 90.7 (vs 90.3 expected) and Expectations Index at 91.5 (vs 93.5 expected). France's INSEE has reported November indicators on business confidence at 79 (vs 84 expected) and manufacturing confidence at 92 (vs 91 expected).

Asian indices closed on the upside except the Chinese CSI.

WTI Crude Oil remains strongly bullish after an alleged Houthis attack on a Saudi Aramco facility.

U.S indices closed up on Monday, lifted by Energy (+7.09%), Automobiles & Components (+2.83%) and Banks (+2.5%) sectors.

Approximately 89% of stocks in the S&P 500 Index were trading above their 200-day moving average and 79% were trading above their 20-day moving average. The VIX Index dropped 1.01pt (-4.26%) to 22.69, while Gold fell $34.95 (-1.87%) to $1836.04, and WTI Crude Oil gained $0.45 (+1.06%) to $42.87 at the close.

On the U.S economic data front, Markit's US Manufacturing Purchasing Managers' Index rose to 56.7 on month in the November preliminary reading (53.0 expected), from 53.4 in the October final reading.

Gold slumps while riskier currencies gain on vaccine hopes and Joe Biden transition.

Gold fell 23.13 dollars (-1.26%) to 1814.74 dollars.

EUR/USD rose 31pips to 1.1872 and GBP/USD gained 25pips to 1.3346.

The dollar index declined 0.16pt to 92.342.

U.S. Equity Snapshot

Tiffany & Co (TIF), the jeweler, reported third quarter adjusted EPS up 73% to 1.11 dollar, above estimates. Net sales were down 0.6% to 1.01 billion dollars, beating expectations.

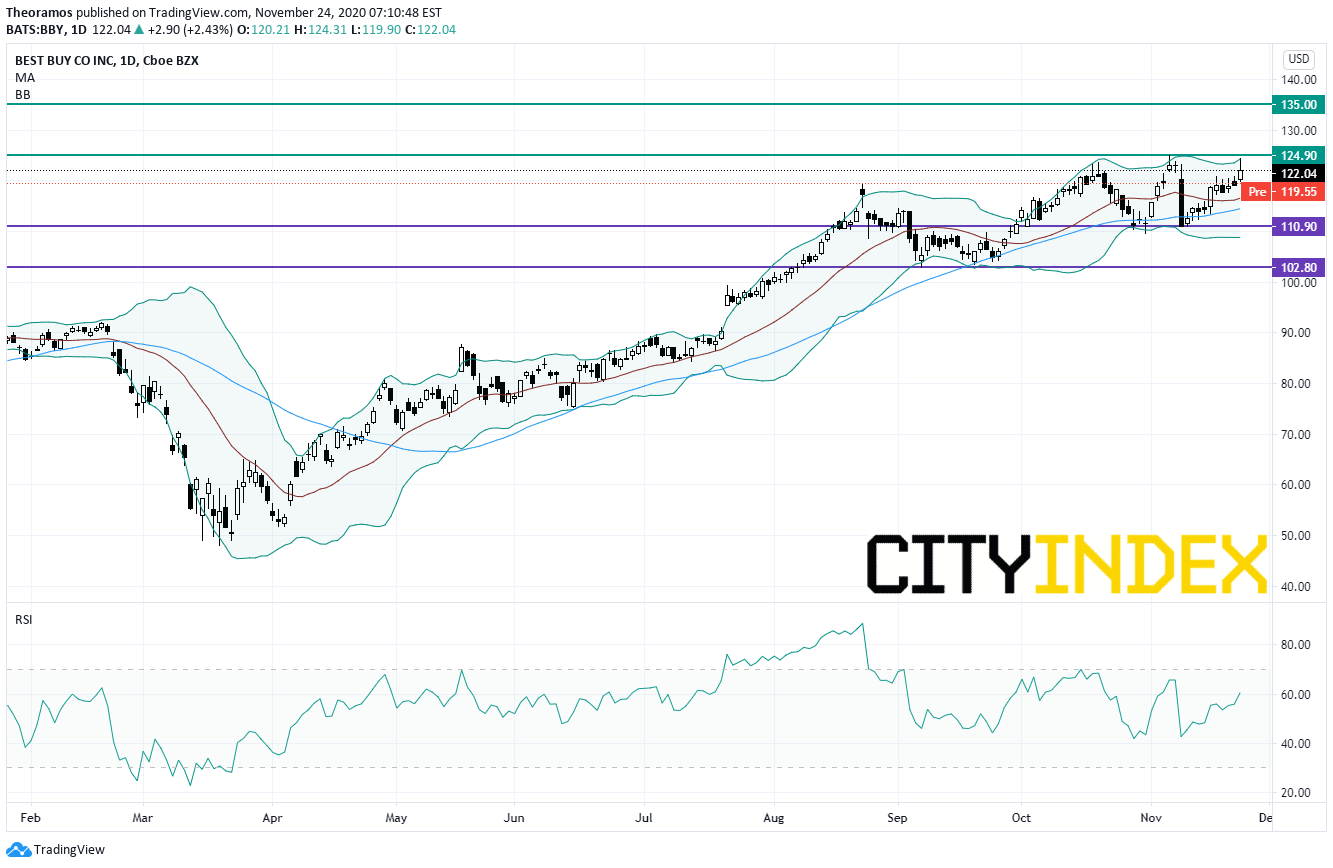

Best Buy (BBY), the consumer electronics retailer, released third quarter comparable sales up 23%, above estimates.

Source: TradingView, GAIN Capital

Agilent Technologies (A), an international life sciences and diagnostics company, lost ground postmarket after unveiling first quarter EPS forecast below estimates. Separately, the company posted fourth quarter earnings that beat expectations.

Medtronic (MDT), a developer and manufacturer of therapeutic medical devices, posted second quarter adjusted EPS down to 1.02 dollar from 1.31 dollar a year earlier, on sales down 0.8% to 7.65 billion dollars. Those figures beat estimates.

Later today, the U.S., the Conference Board will release its Consumer Confidence Index for November (97.9 expected). The Federal Housing Finance Agency will post its house price index for September (+0.5% on month expected). SP Case Shiller will report its house price index for September (+0.6% on month expected).

European indices are strongly rebounding after late session consolidation move yesterday. The German Federal Statistical Office has posted final readings of 3Q GDP at +8.5% (vs +8.2% on quarter expected). Germany's IFO Business has released November Climate Index at 90.7 (vs 90.3 expected) and Expectations Index at 91.5 (vs 93.5 expected). France's INSEE has reported November indicators on business confidence at 79 (vs 84 expected) and manufacturing confidence at 92 (vs 91 expected).

Asian indices closed on the upside except the Chinese CSI.

WTI Crude Oil remains strongly bullish after an alleged Houthis attack on a Saudi Aramco facility.

U.S indices closed up on Monday, lifted by Energy (+7.09%), Automobiles & Components (+2.83%) and Banks (+2.5%) sectors.

Approximately 89% of stocks in the S&P 500 Index were trading above their 200-day moving average and 79% were trading above their 20-day moving average. The VIX Index dropped 1.01pt (-4.26%) to 22.69, while Gold fell $34.95 (-1.87%) to $1836.04, and WTI Crude Oil gained $0.45 (+1.06%) to $42.87 at the close.

On the U.S economic data front, Markit's US Manufacturing Purchasing Managers' Index rose to 56.7 on month in the November preliminary reading (53.0 expected), from 53.4 in the October final reading.

Gold slumps while riskier currencies gain on vaccine hopes and Joe Biden transition.

Gold fell 23.13 dollars (-1.26%) to 1814.74 dollars.

EUR/USD rose 31pips to 1.1872 and GBP/USD gained 25pips to 1.3346.

The dollar index declined 0.16pt to 92.342.

U.S. Equity Snapshot

Tiffany & Co (TIF), the jeweler, reported third quarter adjusted EPS up 73% to 1.11 dollar, above estimates. Net sales were down 0.6% to 1.01 billion dollars, beating expectations.

Best Buy (BBY), the consumer electronics retailer, released third quarter comparable sales up 23%, above estimates.

Source: TradingView, GAIN Capital

Agilent Technologies (A), an international life sciences and diagnostics company, lost ground postmarket after unveiling first quarter EPS forecast below estimates. Separately, the company posted fourth quarter earnings that beat expectations.

Medtronic (MDT), a developer and manufacturer of therapeutic medical devices, posted second quarter adjusted EPS down to 1.02 dollar from 1.31 dollar a year earlier, on sales down 0.8% to 7.65 billion dollars. Those figures beat estimates.

Latest market news

Today 08:15 AM

Today 05:45 AM

Yesterday 11:09 PM

Yesterday 11:01 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM