EU indices on the upside | TA focus on Proximus

INDICES

Yesterday, European stocks closed mixed. The Stoxx Europe 600 Index rebounded 0.20%, Germany's DAX 30 rose 0.41% and the U.K.'s FTSE 100 was up 0.43%, while France's CAC 40 declined 0.40%.

EUROPE ADVANCE/DECLINE

55% of STOXX 600 constituents traded higher yesterday.

29% of the shares trade above their 20D MA vs 26% Monday (below the 20D moving average).

51% of the shares trade above their 200D MA vs 51% Monday (below the 20D moving average).

The Euro Stoxx 50 Volatility index eased 1.77pt to 28.11, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Pers. & House. Goods

3mths relative low: Insurance, Banks

Europe Best 3 sectors

energy, automobiles & parts, technology

Europe worst 3 sectors

insurance, travel & leisure, basic resources

INTEREST RATE

The 10yr Bund yield fell 5bps to -0.53% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -21bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Oct GfK Consumer Confidence, exp.: -1.8

FR 08:15: Sep Markit Composite PMI Flash, exp.: 51.6

FR 08:15: Sep Markit Services PMI Flash, exp.: 51.5

FR 08:15: Sep Markit Manufacturing PMI Flash, exp.: 49.8

GE 08:30: Sep Markit Composite PMI Flash, exp.: 54.4

GE 08:30: Sep Markit Services PMI Flash, exp.: 52.5

GE 08:30: Sep Markit Manufacturing PMI Flash, exp.: 52.2

EC 09:00: ECB Non-Monetary Policy Meeting

EC 09:00: Sep Markit Composite PMI Flash, exp.: 51.9

EC 09:00: Sep Markit Services PMI Flash, exp.: 50.5

EC 09:00: Sep Markit Manufacturing PMI Flash, exp.: 51.7

UK 09:30: Sep Markit/CIPS Manufacturing PMI Flash, exp.: 55.2

UK 09:30: Sep Markit/CIPS UK Services PMI Flash, exp.: 58.8

UK 09:30: Sep Markit/CIPS Composite PMI Flash, exp.: 59.1

MORNING TRADING

In Asian trading hours, the U.S. dollar strengthened further, as EUR/USD slid to 1.1680 and GBP/USD slipped to 1.2721. USD/JPY held gains at 105.12. NZD/USD fell further to 0.6620. This morning, the Reserve Bank of New Zealand kept its benchmark rate unchanged at 0.25% as expected. RBNZ said "further monetary stimulus may be needed", citing "a severe and prolonged economic downturn".

Spot gold was little changed at $1,901 an ounce.

#UK - IRELAND#

Halma, a manufacturer of hazard detection and life protection products, posted a trading update for the period from April 1 to date: "At the end of the first quarter we reported that revenue was 13% lower than last year on an organic constant currency basis. Since then, the Group's revenue trends have gradually improved, (...) Order intake was ahead of revenue albeit marginally down on the same period last year. (...) the Board continues to expect Adjusted profit before tax for FY2021 to be 5%-10% below FY2020 and more weighted to the second half than in previous years." Separately, the company announced that Paul Walker has indicated his intention to retire from his role as Chairman by July.

RELX, a provider of information-based analytics and decision tools, announced that Paul Walker, currently Chairman of Halma, will succeed Sir Anthony Habgood as Chairman.

#GERMANY#

Fresenius, a health care group, was upgraded to "overweight" from "equalweight" at Barclays.

Wacker Chemie, a chemical company, was upgraded to "buy" from "hold" at HSBC.

#FRANCE#

Veolia, a resource management company, is ready to engage in discussion with Engie regarding its proposal to acquire Engie's stake in Suez, according to news agency Agence France-Presse.

Sanofi and GlaxoSmithKline, the two pharmaceutical groups, said they have signed agreements with the Canadian government to supply up to 72 million doses of adjuvanted COVID-19 vaccine. Financial terms were not disclosed.

Orpea, a dependency care company, announced that 1H net income declined 36.3% on year to 73 million euros and EBITDA dropped 5.5% to 439 million euros on revenue of 1.90 billion euros, up 3.5%.

#BENELUX#

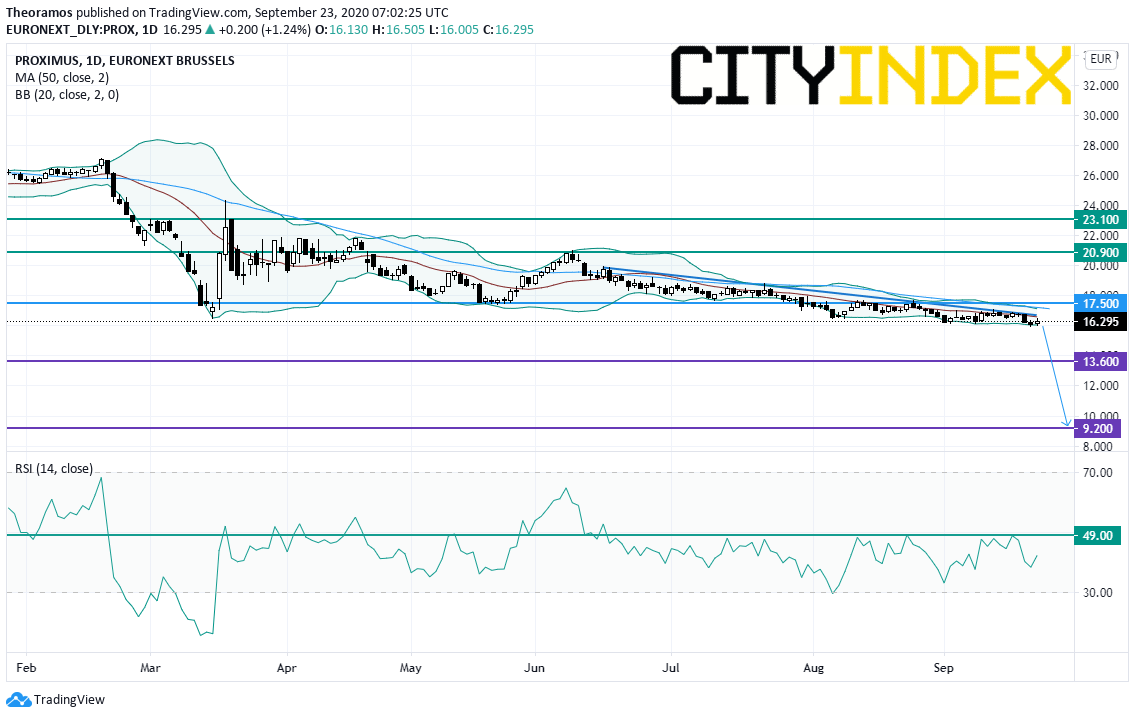

Proximus, a mobile telecommunications company, was downgraded to "neutral" from "buy" at Citigroup.

From a chartist point of view, the share is capped by a short term declining trend line since June. Furthermore, the 50 DMA is playing a resistance role, while a resistance at 49% maintains the RSI. Above the overlap at 17.5E look for 13.6E and 9.2E in extension.

#ITALY#

Snam, an energy infrastructure company, was upgraded to "buy" from "sell" at Goldman Sachs.

#DENMARK#

Coloplast, a medical devices manufacturer, was downgraded to "underweight" from "equalweight" at Barclays.

Yesterday, European stocks closed mixed. The Stoxx Europe 600 Index rebounded 0.20%, Germany's DAX 30 rose 0.41% and the U.K.'s FTSE 100 was up 0.43%, while France's CAC 40 declined 0.40%.

EUROPE ADVANCE/DECLINE

55% of STOXX 600 constituents traded higher yesterday.

29% of the shares trade above their 20D MA vs 26% Monday (below the 20D moving average).

51% of the shares trade above their 200D MA vs 51% Monday (below the 20D moving average).

The Euro Stoxx 50 Volatility index eased 1.77pt to 28.11, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Pers. & House. Goods

3mths relative low: Insurance, Banks

Europe Best 3 sectors

energy, automobiles & parts, technology

Europe worst 3 sectors

insurance, travel & leisure, basic resources

INTEREST RATE

The 10yr Bund yield fell 5bps to -0.53% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -21bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Oct GfK Consumer Confidence, exp.: -1.8

FR 08:15: Sep Markit Composite PMI Flash, exp.: 51.6

FR 08:15: Sep Markit Services PMI Flash, exp.: 51.5

FR 08:15: Sep Markit Manufacturing PMI Flash, exp.: 49.8

GE 08:30: Sep Markit Composite PMI Flash, exp.: 54.4

GE 08:30: Sep Markit Services PMI Flash, exp.: 52.5

GE 08:30: Sep Markit Manufacturing PMI Flash, exp.: 52.2

EC 09:00: ECB Non-Monetary Policy Meeting

EC 09:00: Sep Markit Composite PMI Flash, exp.: 51.9

EC 09:00: Sep Markit Services PMI Flash, exp.: 50.5

EC 09:00: Sep Markit Manufacturing PMI Flash, exp.: 51.7

UK 09:30: Sep Markit/CIPS Manufacturing PMI Flash, exp.: 55.2

UK 09:30: Sep Markit/CIPS UK Services PMI Flash, exp.: 58.8

UK 09:30: Sep Markit/CIPS Composite PMI Flash, exp.: 59.1

MORNING TRADING

In Asian trading hours, the U.S. dollar strengthened further, as EUR/USD slid to 1.1680 and GBP/USD slipped to 1.2721. USD/JPY held gains at 105.12. NZD/USD fell further to 0.6620. This morning, the Reserve Bank of New Zealand kept its benchmark rate unchanged at 0.25% as expected. RBNZ said "further monetary stimulus may be needed", citing "a severe and prolonged economic downturn".

Spot gold was little changed at $1,901 an ounce.

#UK - IRELAND#

Halma, a manufacturer of hazard detection and life protection products, posted a trading update for the period from April 1 to date: "At the end of the first quarter we reported that revenue was 13% lower than last year on an organic constant currency basis. Since then, the Group's revenue trends have gradually improved, (...) Order intake was ahead of revenue albeit marginally down on the same period last year. (...) the Board continues to expect Adjusted profit before tax for FY2021 to be 5%-10% below FY2020 and more weighted to the second half than in previous years." Separately, the company announced that Paul Walker has indicated his intention to retire from his role as Chairman by July.

RELX, a provider of information-based analytics and decision tools, announced that Paul Walker, currently Chairman of Halma, will succeed Sir Anthony Habgood as Chairman.

#GERMANY#

Fresenius, a health care group, was upgraded to "overweight" from "equalweight" at Barclays.

Wacker Chemie, a chemical company, was upgraded to "buy" from "hold" at HSBC.

#FRANCE#

Veolia, a resource management company, is ready to engage in discussion with Engie regarding its proposal to acquire Engie's stake in Suez, according to news agency Agence France-Presse.

Sanofi and GlaxoSmithKline, the two pharmaceutical groups, said they have signed agreements with the Canadian government to supply up to 72 million doses of adjuvanted COVID-19 vaccine. Financial terms were not disclosed.

Orpea, a dependency care company, announced that 1H net income declined 36.3% on year to 73 million euros and EBITDA dropped 5.5% to 439 million euros on revenue of 1.90 billion euros, up 3.5%.

#BENELUX#

Proximus, a mobile telecommunications company, was downgraded to "neutral" from "buy" at Citigroup.

From a chartist point of view, the share is capped by a short term declining trend line since June. Furthermore, the 50 DMA is playing a resistance role, while a resistance at 49% maintains the RSI. Above the overlap at 17.5E look for 13.6E and 9.2E in extension.

Source: TradingView, GAIN Capital

#ITALY#

Snam, an energy infrastructure company, was upgraded to "buy" from "sell" at Goldman Sachs.

#DENMARK#

Coloplast, a medical devices manufacturer, was downgraded to "underweight" from "equalweight" at Barclays.

Latest market news

Today 05:45 AM

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM