US Futures consolidating - Watch SNAP, BIIB, KO, COF, UAL, TXN, M

The S&P 500 Futures closed mixed yesterday, as the tech-heavy Nasdaq 100 Index (-119 points or -1.09% to 10833) took a breather following a series of record closes.

Later today, the National Association of Realtors will report June existing home sales (475 million units expected). The Federal Housing Finance Agency will post its house price index for May (+0.3% on month expected).

European indices are on the downside as President Trump said that Covid-19 crisis is likely to get worse before it gets better.

Asian indices ended in the red except the Chinese CSI. This morning, official data showed that Australia's preliminary retail sales grew 2.4% on month in June (+16.9% on month in May).

WTI Crude Oil futures are under pressure. The American Petroleum Institute (API) reported that U.S. crude stockpiles built 7.5M bbl for the week ended July 16. Later today, the Energy Information Administration (EIA) will release official crude oil inventories data for the same week (-1.95M bbl expected).

Gold remains firm close to a nine-year high on sliding US dollar and hopes of stimulus measures.

Gold rose 17.43 dollars (+0.95%) to 1859.34 dollars.

The euro rose to its highest since October 2018 on euro zone recovery fund plan.

EUR/USD rose 51pips to 1.1578 while GBP/USD fell 28pips to 1.2703.

U.S. Equity Snapshot

Later today, the National Association of Realtors will report June existing home sales (475 million units expected). The Federal Housing Finance Agency will post its house price index for May (+0.3% on month expected).

European indices are on the downside as President Trump said that Covid-19 crisis is likely to get worse before it gets better.

Asian indices ended in the red except the Chinese CSI. This morning, official data showed that Australia's preliminary retail sales grew 2.4% on month in June (+16.9% on month in May).

WTI Crude Oil futures are under pressure. The American Petroleum Institute (API) reported that U.S. crude stockpiles built 7.5M bbl for the week ended July 16. Later today, the Energy Information Administration (EIA) will release official crude oil inventories data for the same week (-1.95M bbl expected).

Gold remains firm close to a nine-year high on sliding US dollar and hopes of stimulus measures.

Gold rose 17.43 dollars (+0.95%) to 1859.34 dollars.

The euro rose to its highest since October 2018 on euro zone recovery fund plan.

EUR/USD rose 51pips to 1.1578 while GBP/USD fell 28pips to 1.2703.

U.S. Equity Snapshot

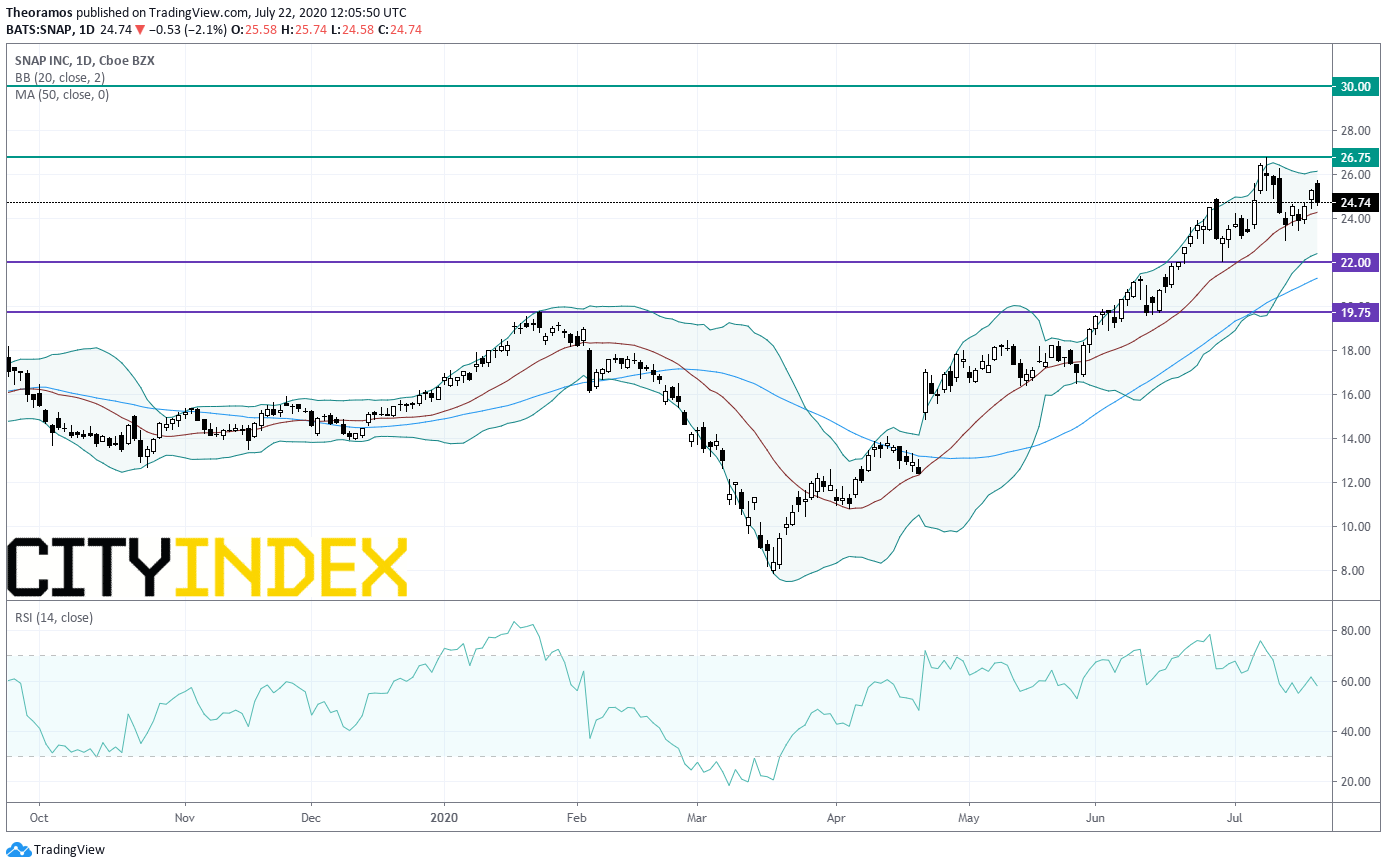

Snap (SNAP), a camera and social media company, reported second quarter adjusted LPS of 0.09 dollar, below expectations, vs a LPS of 0.06 dollar a year ago, on revenue up 17% to 454 million dollars. Also, daily active user rose 4% quarter on quarter to 238 million, below estimates. Following that release, the stock was downgraded to "neutral" from "buy" at Guggenheim.

Source: TradingView, Gain Capital

Biogen Idec (BIIB), a pharmaceutical company, expects full year adjusted EPS between 34 dollars and 36 dollars, above current consensus, vs a previous forecast of 31.50-33.50 dollars. Separately, the company posted quarterly figures that beat estimates.

Coca-Cola (KO), the soft drinks giant, was upgraded to "overweight" from "equal weight" at Morgan Stanley.

Capital One Financial (COF), a diversified banking services firm, disclosed second quarter adjusted LPS of 1.61 dollar, worse than expected, vs an EPS of 3.37 dollars a year ago.

United Airlines (UAL), the transportation company, released second quarter adjusted LPS of 9.31 dollars, worse than anticipated, down from an EPS of 4.21 dollars a year ago, on net revenue of 1.5 billion dollars, above the consensus, down from 11.4 billion dollars last year.

Texas Instruments (TXN), a designer of semiconductors, announced second quarter EPS of 1.48 dollar, beating forecasts, up from 1.36 dollar a year ago on revenue of 3.2 billion dollars, exceeding estimates, down from 3.7 billion dollars in the previous year.

Macy's (M), the department store chain, was downgraded to "sell" from "neutral" at UBS.

Interactive Brokers (IBKR), a global proprietary trading business, reported second quarter adjusted EPS flat at 0.46 dollar, on sales up 31% to 539 million dollars. Both figures beat estimates.

Thermo Fisher Scientific (TMO), the scientific instruments maker, posted second quarter adjusted EPS up to 3.89 dollars from 3.04 dollars a year earlier, on sales up 9.5% to 6.92 billion dollars. Both top and bottom lines beat estimates.

Intuitive Surgical (ISRG), a developer of robotic systems for the medical industry, unveiled second quarter adjusted EPS of 1.11 dollar, exceeding forecasts, down from 3.25 dollars a year ago, on revenue of 852.1 million dollars, better than expected, down from 1.1 billion dollars a year earlier.

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM