US Futures consolidating, watch EXPE, MDT, TTWO, BBY, LB

The S&P 500 Futures are facing a consolidation after they rebounded over 1% yesterday on growing optimism toward a quicker-than-expected recovery of the global economy from the coronavirus pandemic.

Later today, U.S. Initial Jobless Claims

European indices are on posting a consolidation move. Research firm Markit has published preliminary readings of May Manufacturing PMI for the eurozone at 39.5 (vs 38.0 expected), for Germany at 36.8 (vs 39.4 expected), for France at 40.3 (vs 36.0 expected) and for the U.K. at 40.6 (vs 37.2 expected). Also, preliminary readings of May Services PMI were publish for the eurozone at 28.7 (vs 25.0 expected), for Germany at 31.4 (vs 26.0 expected), for France at 29.4 (vs 28.0 expected) and for the U.K. at 27.8 (vs 24.0 expected).

Asian indices closed in the red. This morning, official data showed that Japan recorded a trade deficit of 996 billion yen in April (503 billion yen deficit expected), where exports declined 21.9% on year (-22.2% expected) and imports slid 7.2% (-13.2% expected).

WTI Crude Oil Futures remain on the upside. The U.S. Energy Information Administration (EIA) released a weekly report for May 15, which stated that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 5.0M barrels from the previous week to 526.5M barrels. Meanwhile, U.S. crude oil production fell to 11.5M b/d last week from 11.6M b/d in the prior period.

Later today, U.S. Initial Jobless Claims

(a decline to 2.400 million expected), the Markit U.S. Manufacturing Purchasing Managers' Index (May preliminary reading, 39.5 expected), Existing Home Sales (an annualized rate of 4.22 million units for April expected) and the Conference Board Leading Index (-5.4% on month in April expected) will be reported. Markit May Manufacturing PMI is expected at 39.5 and the May Services PMI is expected at 32.3.

European indices are on posting a consolidation move. Research firm Markit has published preliminary readings of May Manufacturing PMI for the eurozone at 39.5 (vs 38.0 expected), for Germany at 36.8 (vs 39.4 expected), for France at 40.3 (vs 36.0 expected) and for the U.K. at 40.6 (vs 37.2 expected). Also, preliminary readings of May Services PMI were publish for the eurozone at 28.7 (vs 25.0 expected), for Germany at 31.4 (vs 26.0 expected), for France at 29.4 (vs 28.0 expected) and for the U.K. at 27.8 (vs 24.0 expected).

Asian indices closed in the red. This morning, official data showed that Japan recorded a trade deficit of 996 billion yen in April (503 billion yen deficit expected), where exports declined 21.9% on year (-22.2% expected) and imports slid 7.2% (-13.2% expected).

WTI Crude Oil Futures remain on the upside. The U.S. Energy Information Administration (EIA) released a weekly report for May 15, which stated that U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 5.0M barrels from the previous week to 526.5M barrels. Meanwhile, U.S. crude oil production fell to 11.5M b/d last week from 11.6M b/d in the prior period.

Gold fell 14.39$ (-0.82%) to 1733.8 as the US dollar strengthened. The dollar index rose 0.04pt to 99.16.

US Equity Snapshot

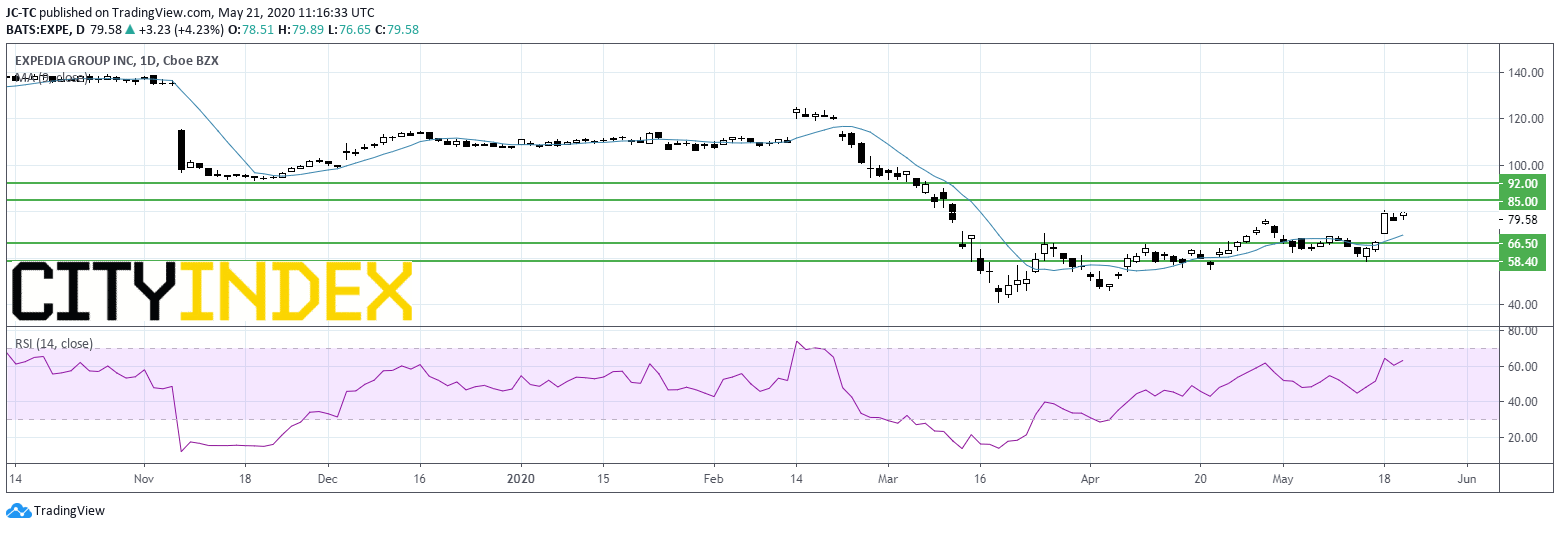

Expedia (EXPE), the online travel agency, disclosed first quarter adjusted LPS of 1.83 dollar, worse than expected, down from a LPS of 0.27 dollar a year ago, on sales of 2.2 billion dollars, just above the consensus, down from 2.6 billion dollars last year. The company said it «accelerated and expanded" its "ambition on improving long-term cost structure".

Medtronic (MDT), a developer and manufacturer of therapeutic medical devices, reported fourth quarter adjusted EPS down to 0.58 dollar, missing estimates, from 1.54 dollar a year earlier. Sales were down 26% to 6 billion dollars, also below forecasts.

Take-Two Interactive Software (TTWO), a leading global video game publisher, announced fourth quarter adjusted EPS of 1.50 dollar, beating estimates, up from 0.78 dollar a year ago, on sales of 729.4 million dollars, exceeding forecasts, up from 488.4 million dollars in the same prior year period. Yet, the stock lost ground in extended trading on profit taking as sales growth seen last quarter may fade after the end of lockdown.

Best Buy (BBY), the consumer electronics retailer, unveiled first quarter same-store sales down 5.3%, beating consensus. Adjusted EPS fell to 0.67 dollar from 1.02 dollar a year earlier, above forecasts.

L Brands (LB), a women's apparel and beauty products retailer, posted first quarter adjusted LPS of 0.99 dollar, below estimates, vs a LPS of 0.15 dollar a year ago, on sales of 1.7 billion dollars, also missing the forecast, down from 2.6 billion dollars in the same previous year period.

Source: TradingVIEW, Gain Capital

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Earnings articles

April 18, 2024 04:46 PM

April 16, 2024 08:00 PM

April 14, 2024 04:00 AM

February 20, 2024 02:53 PM